Topic Summary

Opening a UAE business bank account starts with preparation: banks ask for a defined set of documents, and your business description can make or break the application. This guide covers what to prepare, compares traditional banks with digital-first options, and helps you choose the right bank for your business profile.

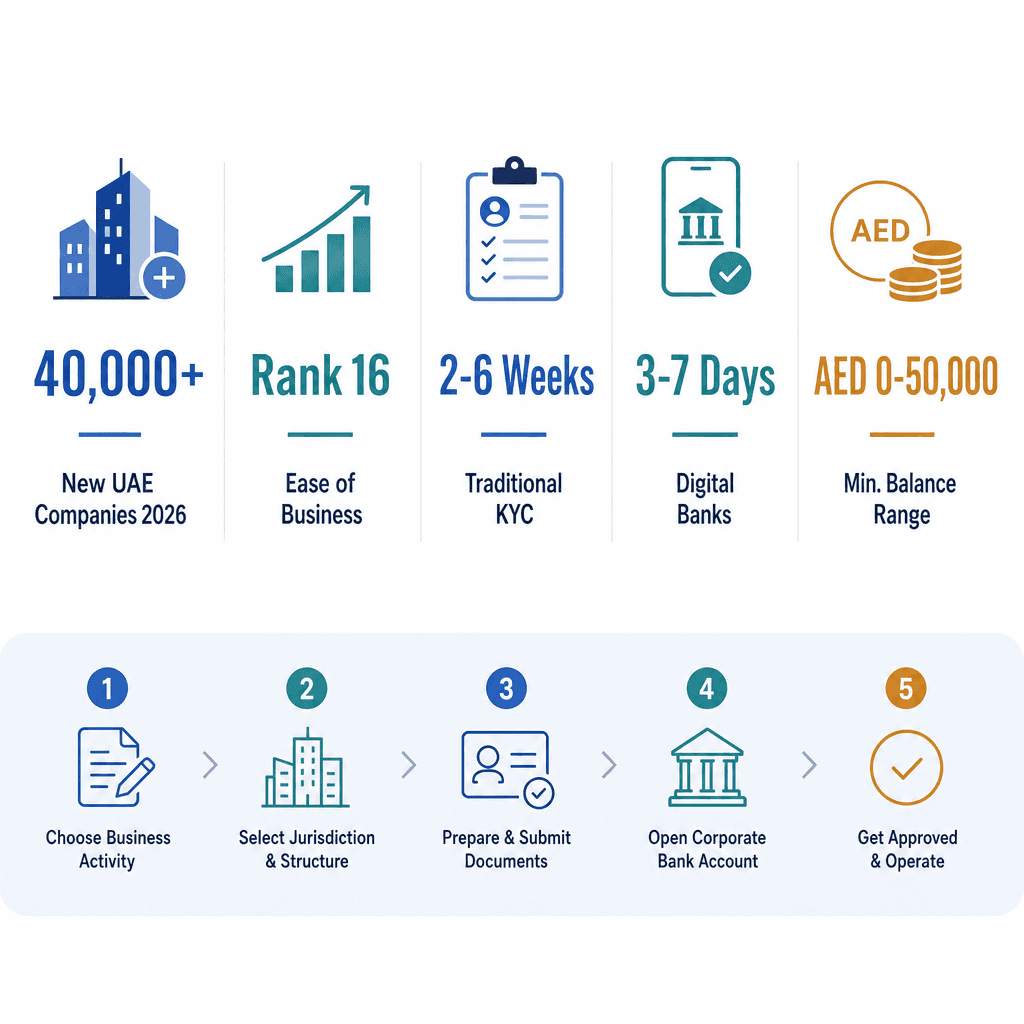

In 2026, over 40,000 new companies are expected to register in UAE free zones (Dubai Department of Economy and Tourism, 2026). The UAE ranks 16th globally for ease of doing business (World Bank, 2024). Traditional bank KYC reviews take 2-6 weeks on average. Digital banks like Wio Business can activate accounts in 3-7 business days. Minimum balances range from AED 0 to AED 50,000 depending on the bank. And incomplete document packs are the single leading cause of delays. Knowing how to open a bank account for your UAE business, correctly, the first time, is what separates founders who are operational in three weeks from those still waiting after three months.

This guide walks you through exactly how to open a bank account for your UAE business: the six documents you need, the banks worth approaching, the five-step process, the real rejection reasons, and how Dubai South Business Hub's banking and taxation services can cut your timeline materially.

What You Need Before You Apply to Open a Bank Account for Your UAE Business

To open a bank account for your UAE business, you need a valid trade license, company Memorandum of Association, passport copies of all shareholders, Emirates ID if you are a UAE resident, proof of business address, and a one-page business description outlining your activity, customers, and expected monthly turnover. Have every item ready before you approach a single bank. Partial applications don't just slow things down, they reset the clock.

The Six Documents Every UAE Bank Will Ask For

Valid UAE trade license, must be current with at least 60 days of validity remaining at the time of application

Company Memorandum of Association (MoA), a notarised copy is required by most banks; free zone companies use their free zone-issued MoA rather than a mainland DED document

Passport copies of all shareholders, directors, and Ultimate Beneficial Owners (UBOs), clear, colour scans only; phone photos are routinely rejected

Emirates ID, required for any UAE-resident shareholder or signatory

Proof of registered business address, a free zone tenancy contract or flexi-desk agreement satisfies this requirement

One-page business description, your activity, customer profile, expected monthly AED turnover, and primary transaction geographies

One Dubai South Business Hub-licensed e-commerce company submitted all six documents upfront, including a precise business overview, and received RAKBank account approval in 18 days. A comparable company that submitted an incomplete pack took 11 weeks after two rounds of back-and-forth with the compliance team. The difference wasn't the bank, it was the preparation.

Why Your Business Description Can Make or Break Your Application

Banks use your business description to assess anti-money laundering (AML) and compliance risk under the UAE Central Bank's KYC framework. A vague description doesn't just delay your application, it flags it. Compliance officers are not reading essays, so keep it to one page.

Your description should specify: the exact licensed activity (for example, "B2B SaaS software licensing to GCC-based SMEs"), your customer profile, expected monthly inflows and outflows in AED, and the primary countries involved in your transactions. Critically, align the description word-for-word with the activity codes on your trade license. Any mismatch triggers additional KYC queries.

A Dubai South-based logistics consultancy initially described its activity as "trading and consulting", a phrase that tells a compliance officer almost nothing. After rewriting to "freight forwarding advisory services to UAE-registered logistics operators, expected monthly turnover AED 80,000," the application cleared KYC in 14 days. Specificity is not optional; it's the mechanism.

Choosing the Right Bank for Your UAE Business

For new UAE free zone companies, RAKBank, Mashreq, and Emirates NBD Business are the most commonly recommended banks when you want to open a business bank account in UAE. Wio Business is the leading digital-first option with zero minimum balance and faster onboarding. E-commerce businesses should prioritise banks with native payment gateway integration, Mashreq and RAKBank both qualify.

Traditional Banks: RAKBank, Mashreq, and Emirates NBD Compared

RAKBank is consistently the top recommendation for SME and free zone startups. It has a formal banking partnership with Dubai South Business Hub, meaning Dubai South Business Hub companies are introduced as pre-verified applicants rather than cold walk-ins. That distinction matters more than most founders realise. Read more about RAKBank business banking at Dubai South.

Mashreq is the strongest choice for e-commerce and cross-border businesses. Its Neo Business digital platform supports multi-currency account management, a Dubai South Business Hub-registered media production company chose Mashreq over Emirates NBD specifically to invoice international clients in USD and EUR without branch visits. Dubai South Business Hub also has an established corporate banking relationship with Mashreq. Details at Mashreq corporate banking at Dubai South.

Emirates NBD Business suits companies planning rapid growth and needing trade finance, foreign exchange facilities, and corporate credit lines. Expect higher minimum balance requirements and a more intensive KYC process in exchange for that product depth.

One rule applies across all three: avoid approaching banks with no existing relationship to your free zone. Relationship-less applications face longer KYC timelines and higher rejection rates.

Wio Business: The Digital-First Option for Lean Startups

Wio Business is a UAE Central Bank (CBUAE)-licensed digital bank built specifically for SMEs. Its headline advantage is AED 0 minimum balance, compared to AED 25,000-50,000 at traditional banks. Onboarding is entirely digital, with account activation possible in as few as 3-7 business days.

A solo-founder Dubai South Business Hub-licensed consulting company used Wio Business to get operational within a week of receiving its trade license. No minimum balance to fund, no branch appointment to schedule. That said, Wio is best suited to companies with straightforward activity profiles and lower initial transaction volumes. Complex multi-shareholder structures, high-value cross-border flows, or trade finance needs still point toward a traditional bank.

UAE Business Bank Account Comparison: RAKBank vs Mashreq vs Wio Business

Feature | RAKBank Business | Mashreq Neo Business | Wio Business |

|---|---|---|---|

Minimum Balance | AED 25,000 | AED 25,000-50,000 | ‚úÖ AED 0 |

KYC Timeline | 2-4 weeks | 2-4 weeks (digital) | ‚úÖ 3-7 business days |

Digital Application | ‚ùå In-person required | ‚úÖ Fully digital | ‚úÖ Fully digital |

Dubai South Business Hub Partnership | ‚úÖ Formal partnership | ‚úÖ Corporate relationship | ‚ùå No formal tie |

Multi-Currency Support | ‚úÖ Yes | ‚úÖ Yes (USD, EUR, more) | Limited |

Best For | SMEs, free zone startups | E-commerce, cross-border | Solo founders, lean startups |

How to Open a Bank Account for Your UAE Business: Five Steps

To open a UAE business bank account: prepare your full document pack, write a one-page business overview, submit your application in-person or digitally, await KYC review (typically two to six weeks for traditional banks), then activate your account and configure online banking and payment gateways. Here's how each step works in practice.

A process timeline showing five steps: Assemble Documents, Write Business Overview, Submit Application, KYC Review, Account Activation. How to Open a Bank Account for Your UAE Business 1 Assemble Documents 2 Write Business Overview 3 Submit Application 4 KYC Review 2-6 Weeks 5 Account Activated

Five-step process to open a UAE business bank account, from document assembly to account activation. Timelines based on 2026-2026 bank processing averages.

Step 1: Assemble Your Complete Document Pack

Gather all six core documents before approaching any bank. Do not apply with a partial pack.

Confirm your trade license has at least 60 days of validity remaining at the point of submission.

Scan all passport copies in colour at high resolution, phone photos are not acceptable.

If any shareholder holds a passport from a FATF grey-listed or black-listed jurisdiction, prepare notarised source-of-funds documentation now. FATF currently lists 23 jurisdictions under increased monitoring as of 2024 (FATF, 2024). This isn't a disqualifier, but walking in without the paperwork is.

A UK-based founder setting up a Dubai South Business Hub-licensed technology consultancy prepared source-of-funds declarations for a co-founder with a Pakistani passport before submitting. The application cleared KYC in 19 days. A comparable company that waited until the bank requested the documents added six weeks to the process.

Step 2: Write Your Business Overview and Step 3: Submit Your Application

Your business overview should be one page, written in plain English. Include: your specific licensed activity, who your customers are, your expected monthly turnover in AED, and the primary countries involved in your transactions. Keep it aligned exactly with your trade license activity codes.

For submission, RAKBank and Emirates NBD currently require an in-person branch appointment for most business account types. Mashreq Neo Business and Wio Business accept fully digital applications. Book a relationship manager appointment wherever possible, walk-in applications at major branches can add one to two weeks. Digital applications through Mashreq Neo or Wio typically receive a first response within 48-72 hours.

Step 4: KYC Review and Step 5: Account Activation

KYC review takes 2-6 weeks at traditional banks and 3-7 business days at digital banks. The most important thing you can do during this period: respond to any bank query within 24 hours. Delayed responses reset the KYC clock at most institutions. Treat every query as urgent.

Once approved, configure online banking immediately and set minimum balance alerts to avoid monthly non-maintenance fees. If your business needs a payment gateway, e-commerce, SaaS, marketplace, activate it through the bank's merchant services team at the same time. Don't treat it as a separate process you'll get to later.

Dubai South Business Hub companies using the free zone's pre-established relationships with RAKBank and Mashreq typically complete Steps 3-5 faster than independent applicants, because the relationship manager already knows Dubai South Business Hub's licensing structure and documentation standards. See Dubai South Business Hub banking and taxation services for current timelines.

Common Reasons UAE Business Bank Accounts Get Rejected, and How to Fix Them

UAE business bank accounts are most commonly rejected due to a virtual office address, a vague or mismatched business description, high-risk ISIC activity codes, or shareholders from FATF-flagged jurisdictions. Each issue is fixable before reapplication. Addressing them proactively cuts rejection risk significantly, and saves you weeks. For a full breakdown, read why your UAE business bank account was rejected.

Virtual Office Address and Unclear Business Description

Problem: Virtual office addresses trigger compliance flags at most UAE banks. Banks want evidence of genuine business presence, a physical or flexi-desk address backed by a tenancy document.

Fix: Use your free zone's registered address supported by your tenancy agreement or flexi-desk contract. Dubai South Business Hub companies have a physical registered address within the free zone, which eliminates this risk entirely.

Problem: Vague descriptions like "general trading" or "consulting" are red flags. Compliance teams treat ambiguity as a risk signal, not a neutral data point.

Fix: Specify exact activity, named customer segments, and realistic AED turnover figures.

One Dubai South Business Hub client initially listed "general trading", a description that appears on a large share of UAE trade licenses. After narrowing to "wholesale distribution of personal care products to UAE-registered pharmacies and supermarkets," the resubmission was approved within three weeks.

High-Risk Activity Codes and Shareholders from Flagged Jurisdictions

Problem: Certain ISIC (International Standard Industrial Classification) activity codes are treated as inherently higher-risk by UAE bank compliance teams, including crypto, money services, arms-adjacent sectors, and specific commodity categories. ISIC Rev.4 classifies all economic activities into 21 sections, and banks use these codes to build their initial risk profile (UN Statistical Commission, 2008).

Fix: If your licensed activity falls into a higher-risk category, engage a relationship manager before submitting and prepare a detailed compliance pack including source-of-funds documentation upfront.

Problem: Shareholders from FATF grey-listed or black-listed jurisdictions require additional due diligence. FATF currently lists 23 jurisdictions under increased monitoring (FATF, 2024).

Fix: Prepare notarised source-of-funds declarations, tax residency certificates, and prior banking references for any flagged-jurisdiction shareholders before you submit. This is not a disqualifier, it's a documentation requirement.

Minimum Balance Requirements for a UAE Business Bank Account

UAE business bank account minimum balances range from AED 0 at Wio Business to AED 25,000-50,000 at Emirates NBD, RAKBank, and Mashreq. Falling below the minimum triggers monthly non-maintenance fees, typically AED 250-500 per month. Factor this into your startup cash flow before you choose a bank.

Bank-by-Bank Minimum Balance Breakdown

References

Editorial sources available on request. Full citation list is being compiled.

Bank | Minimum Balance | Non-Maintenance Fee | Best For |

|---|---|---|---|

Emirates NBD Business | AED 25,000-50,000 | AED 250-500/month | Growth-stage companies |

RAKBank Business | AED 25,000 | AED 250-500/month | SMEs and free zone startups |

Mashreq Business | AED 25,000-50,000 | AED 250-500/month | E-commerce, cross-border |

Wio Business | ‚úÖ AED 0 | ‚úÖ None Useful Resources

|