Topic Summary

The free zone corporate tax regime in Dubai centres on qualifying income: free zone companies that meet the qualifying conditions can access the preferential rate, while non-qualifying income is taxed at the standard rate. This guide explains the legal basis, what a qualifying free zone person means in practice, and where the line falls.

By Editorial Team, Business setup and UAE tax compliance specialists with direct experience advising free zone companies on QFZP structuring. Full bio →

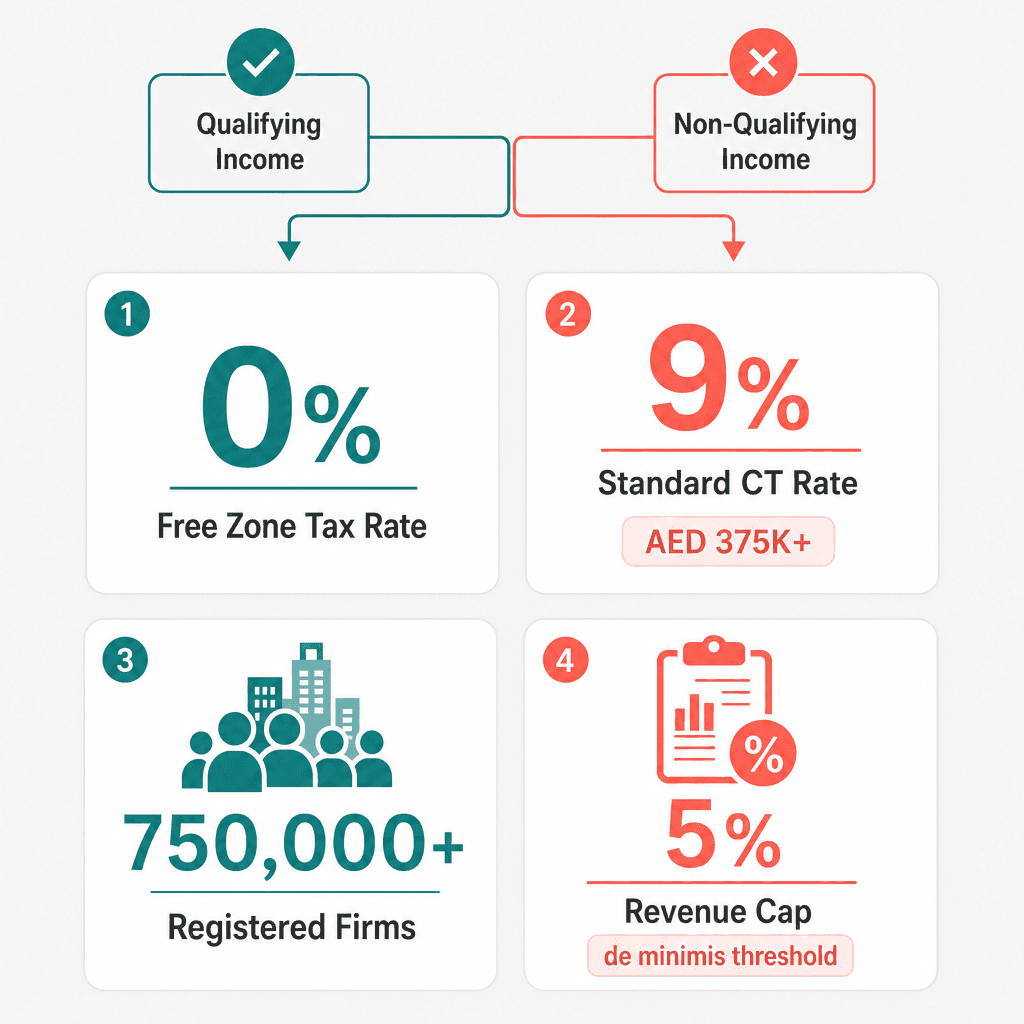

In 2026, over 45 UAE free zones are home to more than 750,000 registered businesses (UAE Ministry of Economy, 2025). The standard corporate tax rate is 9% on taxable income above AED 375,000 (Federal Decree-Law No. 47 of 2022). Free zone qualifying income is taxed at 0%, but only under specific conditions (Ministerial Decision No. 139 of 2023). The de minimis threshold sits at 5% of total revenue or AED 5 million, whichever is lower (MoF, 2023). Dubai South alone covers 145 sq km of purpose-built economic infrastructure (Dubai South, 2025). Yet a significant share of free zone businesses are unknowingly at risk of losing the 0% rate they assumed was automatic.

Dubai free zone companies can still pay 0% corporate tax in the UAE, but only if they meet specific conditions. This is not automatic and it is not guaranteed. Understanding exactly what the conditions are, and whether your business qualifies, is now one of the most important strategic decisions a free zone company owner can make. This guide breaks down exactly what the corporate tax benefits in Dubai free zones mean under Federal Decree-Law No. 47 of 2022, which conditions your company must meet to qualify for the 0% rate, what income types are taxed at 9%, and how to structure your operations to stay fully compliant and tax-efficient.

Qualifying Income vs Non-Qualifying Income Under UAE Free Zone Corporate Tax

Feature | Qualifying Income (0% Tax Rate) | Non-Qualifying Income (9% Tax Rate) |

|---|---|---|

Customer location | ✅ Foreign customers outside the UAE | ❌ UAE mainland customers (individuals or businesses) |

Transaction counterparty | ✅ Other UAE or foreign free zone persons | ❌ UAE mainland-registered companies or individuals |

IP income treatment | ✅ 0% on IP income linked to in-house R&D (nexus test passed) | ❌ 9% on IP income from acquired or outsourced IP (nexus test failed) |

Dividend and capital gain income | ✅ Dividends and capital gains from qualifying foreign shareholdings | ❌ Income from excluded activities under Cabinet Decision No. 55 of 2023 |

Impact on QFZP status | ✅ Preserves QFZP status; all income taxed at 0% | ❌ If over de minimis, triggers 9% on ALL income for the full tax period |

De minimis allowance | ✅ No cap, qualifying income can be 100% of revenue | ❌ Capped at lower of 5% of total revenue or AED 5 million |

What Is the Free Zone 0% Corporate Tax UAE Rate and Who It Actually Applies To

The free zone 0% corporate tax UAE rate applies to Qualifying Free Zone Persons (QFZPs) under Federal Decree-Law No. 47 of 2022. It is not automatic, companies must meet substance requirements, earn qualifying income, and pass a de minimis revenue test to retain the 0% rate.

The Legal Basis: Federal Decree-Law No. 47 of 2022

The UAE introduced a federal corporate tax effective for financial years starting on or after 1 June 2023 (UAE Ministry of Finance, 2022). The standard rate is 9% on taxable income above AED 375,000. Below that threshold, the rate is 0% for all businesses, mainland and free zone alike.

Free zone companies are carved out under a specific regime. They can qualify for a 0% rate on qualifying income, but this is a conditional exemption, not a blanket one. Ministerial Decision No. 139 of 2023 sets out the detailed conditions a Qualifying Free Zone Person must satisfy (still accurate as of 2026).

Take a trading company registered in a UAE free zone earning revenue exclusively from non-UAE clients. It qualifies for 0% on that income, but only if it also meets the substance and de minimis tests. Miss either, and 9% applies to everything.

What 'Qualifying Free Zone Person' Means in Practice

A QFZP is a legal entity or branch incorporated or registered in a UAE free zone that meets all four statutory conditions simultaneously. The four conditions are:

Adequate substance in the free zone (real staff, assets, and operations)

Qualifying income only, or non-qualifying income within the de minimis limits

No election to be taxed at the standard 9% rate

Compliance with UAE transfer pricing rules for related-party transactions

Failing any single condition disqualifies the entire entity. All income becomes taxable at 9% for that period, not just the problematic revenue stream. This is the critical point most business owners miss.

A Dubai South-based logistics company with real staff, a physical office, and contracts with overseas buyers is a textbook QFZP. The same company with no employees and all revenue from a Dubai mainland client is not. The QFZP regime applies across all 45+ UAE free zones including DIFC and Dubai South; the conditions are federal and identical regardless of which zone you operate in. For a deeper breakdown, see our guide on understanding qualifying income for UAE corporate tax.

Qualifying Income vs Non-Qualifying Income: The Line That Determines Your Tax Rate

Qualifying income includes revenue from transactions with other free zone persons and foreign customers outside the UAE. Non-qualifying income, primarily revenue from UAE mainland customers, is taxed at the standard 9% corporate tax rate. The distinction is the single most important factor in your free zone tax strategy and the primary driver of corporate tax benefits in Dubai free zones.

What Counts as Qualifying Income

Under the free zone tax exemption UAE framework, qualifying income includes:

Income from transactions with other free zone persons (UAE or foreign free zone entities)

Income from foreign customers, individuals or businesses located outside the UAE

Income from IP ownership or exploitation, subject to the nexus test

Dividends and capital gains from qualifying shareholdings in foreign entities

The key principle: qualifying income is income that does not originate from the UAE domestic (mainland) economy. A free zone-registered software company licensing its platform to clients in the UK, Germany, and Singapore earns qualifying income on all three contracts, all taxed at 0% under Federal Decree-Law No. 47 of 2022, Article 18.

What Counts as Non-Qualifying Income

Non-qualifying income covers:

Revenue from UAE mainland customers, whether individuals or mainland-registered businesses

Income from "excluded activities" under Cabinet Decision No. 55 of 2023, including most financial services, insurance, and certain IP activities that fail the nexus test

Any income that, when combined, pushes non-qualifying revenue above the de minimis threshold

Warning: A free zone trading company that starts supplying goods to a Dubai mainland retailer is now generating non-qualifying income. If that revenue exceeds 5% of total revenue or AED 5 million (whichever is lower), the entire company loses QFZP status for that tax period, not just the mainland revenue portion (Ministerial Decision No. 139 of 2023). The de minimis cliff is real, and it catches growing businesses off guard. For more detail, see our guide on understanding qualifying income for UAE corporate tax.

Is there a way to serve mainland UAE customers and still keep the 0% rate?

Yes, but only if your non-qualifying revenue stays below both 5% of total revenue and AED 5 million in the same tax period. Exceeding either figure removes QFZP status for that entire year. A dual-entity structure (free zone company plus a mainland LLC) is the most common compliant solution for businesses that need to serve both markets.

Substance Requirements: What the Free Zone Tax Exemption UAE Actually Demands

To retain the free zone tax exemption UAE, a company must maintain adequate substance in its free zone: real employees, physical assets, and operational expenditure proportionate to its activities. A shell company or a registered address with no genuine presence does not qualify and will be taxed at 9%.

The Three Pillars of Adequate Substance

The Federal Tax Authority (FTA) assesses substance against three pillars, per Ministerial Decision No. 139 of 2023:

Pillar 1, People: Sufficient qualified full-time employees (or contracted staff) physically based in the free zone. The FTA looks at headcount relative to business volume, not a fixed number.

Pillar 2, Assets: Adequate operating assets in the free zone, office space, equipment, or infrastructure proportionate to the business scale. A virtual mailbox address alone will not pass.

Pillar 3, Expenditure: Core income-generating activities must be conducted in the free zone. Income cannot flow through a letterbox entity with all real work happening elsewhere.

A Dubai South free zone company with two full-time finance professionals, a licensed office, and documented deal-flow records from overseas clients easily passes the substance test. A company with no staff, no office lease, and all activity managed from a mainland parent does not. Worth flagging: substance requirements under UAE corporate tax law are separate from the earlier Economic Substance Regulations (ESR) introduced in 2019. ESR compliance helps, but it does not automatically satisfy the corporate tax substance test. See our overview of economic substance regulations UAE for the broader regulatory context.

The Nexus Test for Intellectual Property Income

IP income receives 0% treatment only if the free zone company itself conducted the research and development that created the IP. This is the nexus test, aligned with OECD BEPS Action 5 standards (OECD, 2015, still the applicable framework as of 2026).

The nexus fraction works like this: qualifying R&D expenditure ÷ total R&D expenditure × total IP income = qualifying IP income at 0%. The remainder is taxed at 9%.

A free zone tech company that built its own SaaS platform in-house can apply 0% to all licensing revenue. A company that purchased the IP from its Cayman Islands parent and merely licenses it onward faces partial or full 9% exposure. This rule specifically targets "patent box" structures where companies park IP in low-tax jurisdictions without doing any actual innovation work.

5 stepsh2>

To confirm your free zone company qualifies for the 0% corporate tax rate, you must: (1) verify QFZP eligibility, (2) map all income streams as qualifying or non-qualifying, (3) confirm substance in the free zone, (4) apply the de minimis test, and (5) register with the Federal Tax Authority. These steps are how to pay zero tax in Dubai, legally and sustainably.

Step 1 to Step 3: Eligibility, Income Mapping, and Substance Check

Confirm QFZP eligibility: Verify your entity is incorporated in a recognised UAE free zone and is not conducting excluded activities under Cabinet Decision No. 55 of 2023. Check your license activities against the excluded activities list, some financial services and insurance activities disqualify you regardless of customer location.

Map your income: Categorise every revenue stream as qualifying (foreign or free zone customers) or non-qualifying (mainland UAE customers). Use contract-level analysis, not just invoices. The registered address of your counterparty, not the payment origin, determines the classification.

Substance audit: Document your headcount, office lease, asset register, and evidence that core activities are conducted in the free zone. This documentation is your first line of defence in an FTA audit.

A Dubai South logistics company conducting a pre-filing substance audit discovered that three of its client contracts, assumed to be free zone transactions, were technically with mainland-registered buyers. Reclassifying those contracts as non-qualifying income brought them within the de minimis limit and preserved QFZP status. Contract-level income mapping, not aggregate revenue review, is what the FTA expects (FTA corporate tax guidance, 2023). For operational guidance on documentation, see accounting and tax compliance at Dubai South.

Step 4 to Step 5: De Minimis Test and FTA Registration

Apply the de minimis rule: Calculate whether your non-qualifying revenue is below both 5% of total revenue and AED 5 million. If it exceeds either threshold, you lose QFZP status for the entire tax period, not just on the excess amount. This cliff-edge effect is the most common compliance trap for growing free zone companies.

Register with the FTA and file correctly: All UAE companies with annual revenue above AED 1 million must register for corporate tax (Federal Tax Authority, tax.gov.ae). QFZPs must file a tax return even if their liability is AED 0, non-filing is a compliance breach regardless of tax owed.

Here's a concrete illustration of the de minimis cliff: a free zone consultancy with AED 8 million in total revenue and AED 350,000 from a mainland client (4.375% of revenue) passes the test and retains QFZP status. If that mainland revenue grew to AED 420,000 (5.25%), it would fail, and all AED 8 million becomes taxable at 9%. That's a potential AED 363,375 tax bill triggered by AED 70,000 of additional mainland revenue. Maintain annual documentation covering substance evidence, income classification records, and transfer pricing files if you transact with related parties.

What Happens If Your Free Zone Company Fails the Qualifying Conditions

If a free zone company fails any qualifying condition under Federal Decree-Law No. 47 of 2022, it loses Qualifying Free Zone Person status and all its income, not just the non-qualifying portion, becomes taxable at 9% for that entire tax period. The disqualification cannot be applied selectively, and this is one of the sharpest edges in the corporate tax free zone companies framework.

The All-or-Nothing Nature of QFZP Disqualification

Disqualification is binary. There is no partial QFZP status. Fail one condition and 9% applies to all taxable income for the full tax period (Federal Decree-Law No. 47 of 2022).

The most common disqualification triggers are: (1) non-qualifying revenue exceeds the de minimis threshold, (2) substance falls below the adequate level mid-year due to staff departures or office downsizing, and (3) the company begins conducting excluded activities without realising they're excluded.

Disqualification applies for the tax period in which the breach occurs, it does not carry back to prior periods. A company can requalify in a subsequent tax period if it remedies the breach, but it must maintain qualifying status continuously to benefit each year.

A free zone holding company that starts providing intra-group services to its UAE mainland subsidiary, without a formal intercompany agreement or arm's-length pricing, risks both disqualification from QFZP status and a transfer pricing challenge from the FTA simultaneously. Two problems from one oversight.

Transfer Pricing Obligations That Can Trigger Disqualification

QFZPs that transact with related parties must comply with UAE transfer pricing rules under the arm's-length principle. Key obligations include:

Maintaining a master file and local file for related-party transactions above AED 3.75 million per year (FTA transfer pricing guidance, 2023)

Pricing all intercompany transactions at arm's length, not just documenting that you have done so

Treating related-party transactions with UAE mainland group entities as particularly high-risk: they may generate non-qualifying income and attract FTA scrutiny

A free zone parent company charging a management fee to its mainland subsidiary must document the fee at arm's length. If the FTA recharacterises the fee as inflated, it can reclassify the income and challenge QFZP status retroactively. Failure to maintain transfer pricing documentation is itself a disqualification trigger, independent of whether the underlying pricing is actually correct. Our DSBH banking and taxation services team can help you structure intercompany agreements that hold up to FTA review.

How to Structure Your Business to Maximise Corporate Tax Benefits in Dubai Free Zones

To maximise corporate tax benefits in Dubai free zones, structure your operations so that revenue flows from foreign clients and other free zone entities, maintain genuine substance in the free zone, keep mainland UAE revenue below the de minimis threshold, and review your income classification at every financial year-end.

Revenue Routing and Customer Segmentation Strategies

Practical strategies for protecting the free zone 0% corporate tax UAE rate include:

Route international and free zone client contracts through your free zone entity, these generate qualifying income at 0%

If you serve mainland UAE customers, assess whether a separate mainland LLC is more tax-efficient than risking the de minimis breach through your free zone company

Use dual-entity structures, one free zone company for international and free zone business, one mainland entity for

References

Editorial sources available on request. Full citation list is being compiled.