Topic Summary

UAE corporate tax law defines specific categories of exempt persons, and exemption is distinct from the free zone qualifying rate. This guide explains the legal basis for exemptions, why the exempt-versus-qualifying distinction matters, and the categories of entities that qualify, from government bodies and natural resource extractors to pension funds.

By Editorial Team, Business setup and UAE tax compliance specialists with direct experience advising free zone and mainland entities on Federal Tax Authority registration. Full bio →

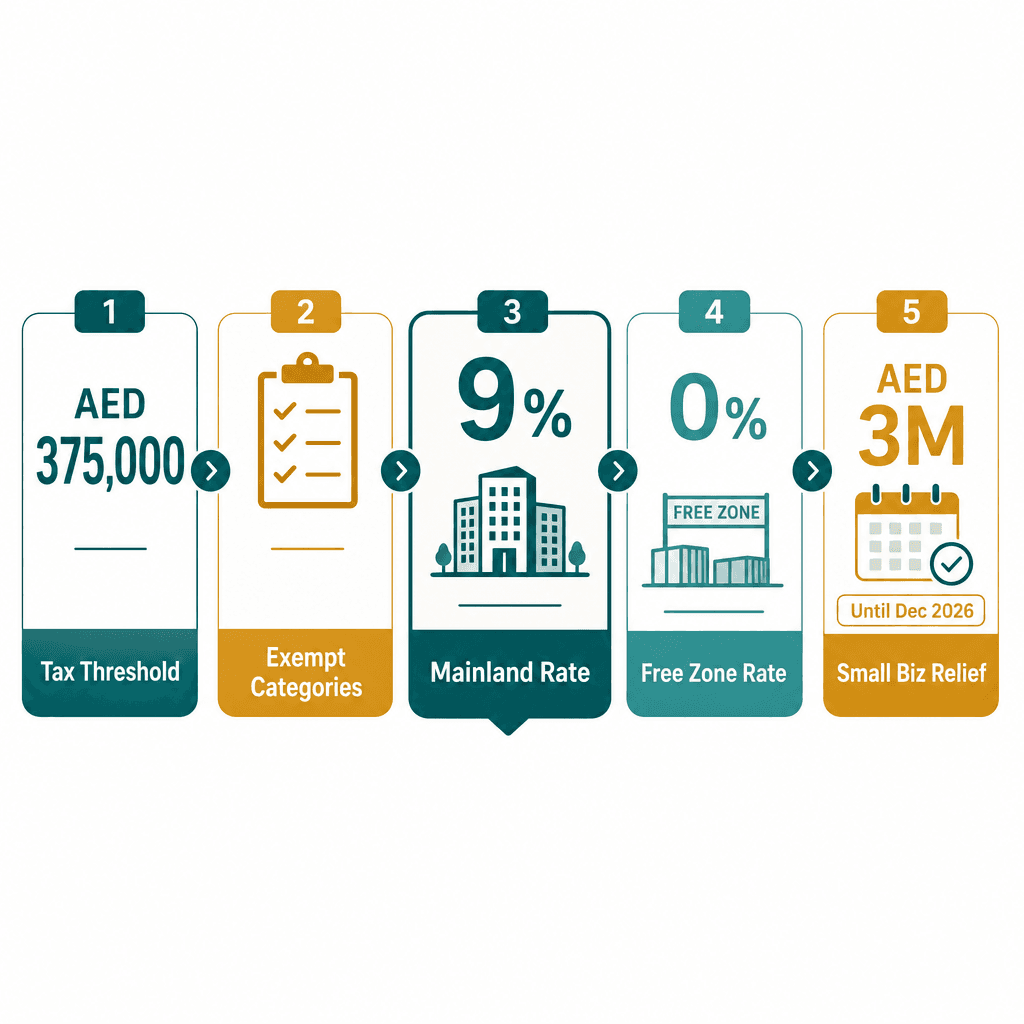

In 2026, the UAE's 9% corporate tax rate applies to the majority of mainland businesses, but Federal Decree-Law No. 47 of 2022 carves out seven defined categories of entities that either pay nothing or qualify for a 0% rate (Federal Decree-Law No. 47 of 2022). The standard rate kicks in on taxable income above AED 375,000 [1]. Small Business Relief covers entities with revenue under AED 3 million, temporarily through 31 December 2026 (Ministerial Decision No. 43 of 2023) [2]. Free zone persons earning qualifying income pay 0%, not exempt, but effectively zero (FTA guidance, 2023) [3]. Over 45 free zones operate across the UAE, each with businesses that must actively manage their tax position [4]. Cabinet Decision No. 37 of 2023 governs which government-controlled entities qualify for full exemption [5].

Not every UAE entity pays corporate tax. The law includes a defined list of corporate tax exemptions in the UAE, but qualifying for them is not automatic, and the conditions are specific. This article covers every exemption category in plain terms: what qualifies, what the exact conditions are, and what you need to do to actually claim the relief.

What Are Corporate Tax Exemptions in the UAE and How the Law Defines Them

Corporate tax exemptions in the UAE are defined under Federal Decree-Law No. 47 of 2022 and cover seven categories of entities, including government bodies, natural resource extractors, qualifying charities, investment funds, pension funds, qualifying free zone persons, and small businesses, that are either fully exempt or taxed at 0%.

The Legal Basis: Federal Decree-Law No. 47 of 2022

The UAE introduced corporate tax for financial years starting on or after 1 June 2023 under Federal Decree-Law No. 47 of 2022. The standard rate is 9% on taxable income above AED 375,000, and the exemptions are explicitly carved out within the same legislation. For foundational context on how the regime works, see our UAE corporate tax explained guide.

Here's the critical point most businesses miss: exemptions are not self-executing. Most require registration with the Federal Tax Authority (FTA) or a formal Cabinet or ministerial decision. A UAE government-owned infrastructure company that has always filed under emirate-level rules, for example, does not automatically receive federal corporate tax exemption, it must apply for Exempt Person status with the FTA directly.

Exempt vs. 0% Rate: Why the Distinction Matters

Exempt means the entity sits entirely outside the corporate tax regime. No registration. No filing. No return. A federal government ministry qualifies here, it simply does not interact with the federal corporate tax system at all.

The 0% rate is a completely different category. A free zone person earning qualifying income is registered for corporate tax, files a return, and pays zero. It's subject to the regime, just at a nil rate on qualifying income. A Dubai South free zone company earning qualifying income files a corporate tax return and pays 0%. That is not the same as being exempt.

Misclassifying your status has real compliance consequences. An entity that should be registered but isn't faces FTA penalties. If you're in a free zone and you've been treating yourself as exempt rather than as a 0%-rate registered person, that's a problem worth fixing now.

Exempt Person vs. 0% Rate Free Zone Person: Key Differences

Feature | Exempt Person | 0% Rate Free Zone Person |

|---|---|---|

Subject to Corporate Tax Regime | ❌ Outside the regime entirely | ✅ Inside the regime at 0% |

FTA Registration Required | ✅ Must notify FTA | ✅ Must register for CT |

Annual Tax Return Required | ❌ No return filed | ✅ Return filed annually |

Rate on Qualifying Income | N/A (not taxable) | 0% |

Rate on Non-Qualifying Income | N/A | 9% |

Substance Requirements | ❌ Not applicable | ✅ Mandatory |

De Minimis Rule Applies | ❌ Not applicable | ✅ 5% or AED 5M cap |

7 Categories of Corporate Tax Exemptions in the UAE: The Complete List

The UAE corporate tax law recognises seven exemption or 0%-rate categories: UAE government entities, natural resource extraction businesses taxed at emirate level, qualifying public benefit entities, qualifying investment funds, public and private pension funds, qualifying free zone persons earning qualifying income, and small businesses with revenue under AED 3 million claiming Small Business Relief.

The Full UAE CT Exemptions List at a Glance

Here's the complete UAE CT exemptions list under Federal Decree-Law No. 47 of 2022. This list is exhaustive, if your entity isn't on it, it's taxable at the standard 9% rate.

UAE Government Entities, Federal and emirate bodies are fully exempt; requires FTA notification.

Government-Controlled Entities, Entities meeting Cabinet Decision No. 37 of 2023 criteria; Cabinet listing required.

Natural Resource Extraction Businesses, Subject to emirate-level taxation; excluded from the federal regime automatically.

Qualifying Public Benefit Entities, Charities, foundations, and similar bodies; Cabinet or ministerial decision required.

Qualifying Investment Funds, Regulated, widely held funds meeting FTA conditions; formal application required.

Public and Private Pension Funds, UAE-regulated pension and end-of-service funds; FTA exempt status application required.

Qualifying Free Zone Persons, 0% rate on qualifying income only; full CT registration and annual return required.

Small Business Relief is a separate mechanism, technically a relief rather than an exemption, available to UAE resident businesses with revenue under AED 3 million, temporarily through tax periods ending before 31 December 2026 (Ministerial Decision No. 43 of 2023).

A private charity established in Abu Dhabi, a government-linked sovereign wealth vehicle, and a family pension trust are all on this list, but each follows a completely different approval path. Don't assume that being "government-related" or "non-profit" is enough. The specific conditions for each category are what matter.

Government Entities, Natural Resource Extractors, and Pension Funds: Automatic and Emirate-Level Exemptions

UAE government entities and government-controlled entities are automatically exempt from federal corporate tax. Businesses extracting UAE natural resources remain subject to emirate-level taxation and are excluded from the federal regime. Public and private pension or social security funds are also exempt, provided they are regulated under UAE law.

UAE Government Entities and Government-Controlled Entities

Federal and emirate government bodies, ministries, departments, and authorities established by law, are fully exempt from UAE corporate tax. That covers a wide range of entities, but it doesn't cover every organisation with government involvement.

Government-controlled entities can also qualify, but the bar is specific. Under Cabinet Decision No. 37 of 2023, the government must hold a direct or indirect ownership interest meeting defined criteria, and the entity's purpose must align with the conditions set out in that decision. Partial government ownership alone isn't sufficient.

Consider this: a government-owned port authority operating under a federal mandate is fully exempt. A partially government-owned commercial hotel chain is not automatically exempt, it must meet the specific control and purpose criteria under Cabinet Decision No. 37 of 2023 before the FTA will accept an exemption application.

Confirm your entity appears on or meets the Cabinet-issued criteria.

Apply for Exempt Person status via the EmaraTax portal.

Exempt persons must still notify the FTA, registration requirements apply (FTA guidance, 2023).

Natural Resource Extraction Businesses: Emirate-Level Tax Applies

Businesses engaged in extracting UAE natural resources, oil, gas, and minerals, are subject to emirate-level taxation, not the federal 9% rate. This exclusion preserves the long-standing fiscal arrangements between the federal government and individual emirates, particularly Abu Dhabi.

An Abu Dhabi-based oil extraction company operating under an emirate concession agreement pays emirate-level royalties and taxes. Its extraction profits sit entirely outside the federal corporate tax regime.

Worth flagging: this exemption from UAE corporate tax applies only to the extraction activity itself. If the same entity runs commercial operations, retail fuel sales, logistics services, or property leasing, those activities may fall under the federal 9% rate. Mixed-activity entities need to clearly delineate income streams and confirm emirate-level treatment with a qualified tax advisor.

Public and Private Pension and Social Security Funds

Both government-run pension funds and private pension or end-of-service benefit funds qualify for exemption, provided they are established and regulated under UAE law. Offshore schemes or unregulated arrangements do not qualify.

Investment returns generated within a qualifying pension fund are protected under the exemption, so the fund's growth isn't eroded by corporate tax (FTA guidance, 2023). A UAE-regulated end-of-service gratuity fund set up by a large private employer to manage staff entitlements can qualify, provided it meets the regulatory criteria. The action step: confirm regulatory standing under UAE law, then apply for exempt status through EmaraTax.

Qualifying Public Benefit Entities and Investment Funds: Cabinet-Approved Exemptions

Qualifying public benefit entities, charities, foundations, and similar organisations, are exempt from UAE corporate tax, but only after receiving Cabinet approval and being listed by ministerial decision. Qualifying investment funds are also exempt, subject to specific conditions around investor concentration, distribution of income, and regulatory status.

Qualifying Public Benefit Entities: What Charities and Foundations Must Prove

The entity must be established for a public benefit purpose: religious, charitable, scientific, educational, cultural, athletic, or broader community benefit. That's the starting point, but it's not enough on its own.

Under Federal Decree-Law No. 47 of 2022, Article 9, public benefit entities must be listed by Cabinet Decision or ministerial decision. There is no self-certification. A UAE-registered foundation that funds school-building projects in underserved communities can apply for public benefit entity status, but it must secure Cabinet approval and cannot distribute profits to founders or directors.

Income must be used exclusively for the stated public benefit purpose.

Commercial activity income generated by the entity may still be taxable.

Apply to the Ministry of Finance for inclusion on the qualifying list.

Maintain records showing all income is applied to the public benefit purpose.

For support with compliance documentation, see our guide on accounting and tax compliance at Dubai South.

Qualifying Investment Funds: Conditions That Must Be Met

Investment funds qualify if they are regulated, widely held, and primarily engaged in investment activity, not active business operations. The FTA has set specific thresholds that must all be satisfied simultaneously.

No single investor or connected group holds more than 30% of the fund (FTA Corporate Tax guidance).

The fund is not used to circumvent corporate tax obligations.

Income is distributed to investors within a reasonable period.

The fund maintains appropriate regulatory status in the UAE or a recognised jurisdiction.

A UAE-regulated real estate investment trust (REIT) listed on the Dubai Financial Market that distributes 80% of income annually to a diversified investor base is a strong candidate for qualifying investment fund status. If you're uncertain whether your fund meets the concentration threshold, get a formal FTA ruling before filing, retroactive corrections are harder to manage than proactive ones.

Free Zone Persons and the 0% Rate: How Qualifying Income Works

Free zone persons in the UAE are not exempt from corporate tax, they are subject to it at a 0% rate on qualifying income and 9% on non-qualifying income. To maintain the 0% rate, the entity must meet substance requirements, earn qualifying income as defined by the law, and not elect out of the free zone regime.

What Counts as Qualifying Income for Free Zone Businesses

Qualifying income includes income from transactions with other free zone persons, income from qualifying activities defined by Ministerial Decision No. 139 of 2023 (trading goods, manufacturing, logistics, fund management, and others), and income earned from overseas customers. For a full breakdown, see our guide on understanding qualifying income for UAE corporate tax.

Income from mainland UAE customers generally does not qualify and is taxed at 9%. Here's a concrete example: a Dubai South logistics company that invoices a fellow free zone entity for warehousing services earns qualifying income at 0%. The same company invoicing a mainland Dubai retailer for identical services earns non-qualifying income at 9%. Same activity, different customer, different tax rate.

Substance Requirements and the De Minimis Rule

Maintaining the 0% rate requires more than just earning the right type of income. You need adequate substance: real operations, employees, and decision-making physically located in the free zone. A shell entity with no staff and no genuine activity in the zone won't satisfy the FTA's substance test.

The de minimis rule is where many free zone businesses trip up. Non-qualifying revenue must not exceed the lower of 5% of total revenue or AED 5 million (Ministerial Decision No. 139 of 2023). Breach that threshold and the entire entity's income, not just the non-qualifying portion, becomes taxable at 9%.

A free zone manufacturing company earning AED 10 million total revenue cannot have more than AED 500,000 from non-qualifying mainland sources without triggering full 9% taxation on everything. That's a significant exposure. Electing out of the free zone regime is also possible, but it's a five-year lock-in, so think carefully before doing it. For detailed guidance on protecting the 0% rate, see our article on corporate tax benefits in Dubai free zones.

Is a free zone company in the UAE exempt from corporate tax?

No. A free zone company is a registered taxable person subject to UAE corporate tax. It qualifies for a 0% rate on qualifying income only, not full exemption. It must register with the FTA, file annual returns, and maintain substance and de minimis compliance to protect the 0% rate.

Small Business Relief: The Temporary Exemption for Revenue Under AED 3 Million

Small Business Relief allows UAE businesses with revenue under AED 3 million in a tax period to be treated as having zero taxable income, effectively paying no corporate tax. This relief is temporary, it applies to tax periods ending on or before 31 December 2026, and must be actively elected on the corporate tax return.

Who Qualifies and What the Revenue Threshold Covers

Revenue must be AED 3 million or less in the relevant tax period and in all previous tax periods from 1 June 2023 onward (Ministerial Decision No. 73 of 2023). It's measured on gross revenue, the same basis as your financial statements, not net profit. Revenue is cumulative: if you exceeded AED 3 million in a prior period, you can't claim the relief now.

A UAE-based consultancy that generated AED 2.4 million in its first tax year can elect Small Business Relief, treating taxable income as zero, saving up to AED 182,700 in corporate tax at the 9% rate on income above AED 375,000. That's a meaningful saving for an early-stage business.

Two groups are excluded: qualifying free zone persons (who are generally better served by the 0% free zone regime) and businesses that are part of a multinational group with consolidated revenues exceeding AED 3.15 billion, which falls under the Pillar Two threshold.

How to Elect Small Business Relief and What Happens After 2026

Small Business Relief is not automatic. You must elect it on the corporate tax return for each qualifying period. And here's the trade-off: electing the relief means forfeiting other tax benefits for that period, including tax loss carry-forwards and group relief transfers.

The relief expires for tax periods ending after 31 December 2026 (Ministerial Decision No. 43 of 2023). A startup qualifying for the relief in 2024 and 2025 should already be modelling its 2027 tax position. Once revenue crosses AED 3 million or the relief period ends, the standard 9% rate applies, with no phase-in. Start planning now, not in late 2026.

How to Claim Your Corporate Tax Exemption in the UAE: Conditions and Registration

Claiming a corporate tax exemption in the

References

[1] Source pending — please add URL and publisher.

[2] Source pending — please add URL and publisher.

[3] Source pending — please add URL and publisher.

[4] Source pending — please add URL and publisher.

[5] Source pending — please add URL and publisher.