Topic Summary

In the UAE, personal income remains tax-free while business profits above the qualifying threshold are subject to corporate tax. This practical guide explains what corporate tax means for UAE residents, how it affects employed residents, natural persons in business and company shareholders differently, and how dividends are treated.

By Editorial Team, Business setup and UAE tax compliance specialists with direct experience advising mainland and free zone companies across Dubai and Abu Dhabi. Full bio →

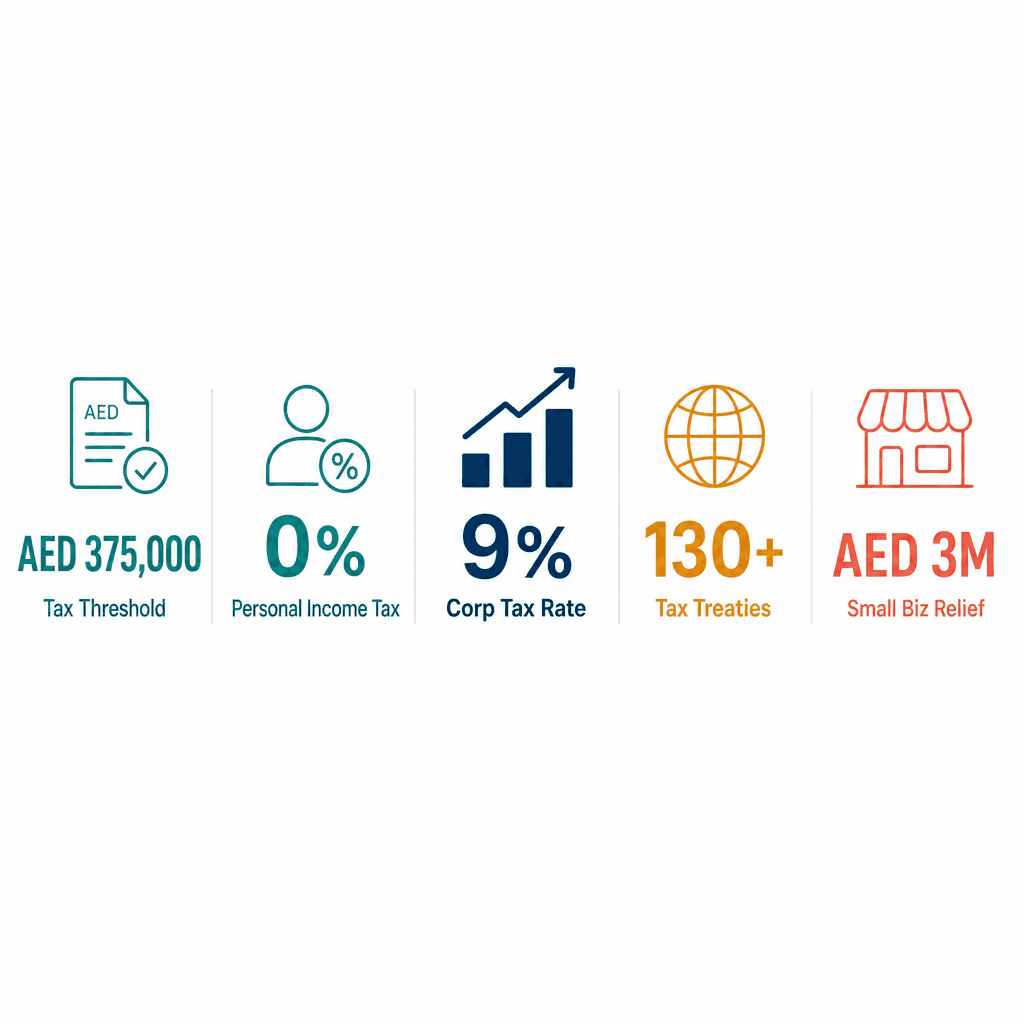

In 2026, the UAE's corporate tax rate sits at 9% on business profits above AED 375,000 (Federal Decree-Law No. 47 of 2022). The personal income tax rate remains 0% for all UAE residents (UAE Federal Tax Authority, 2023). Corporate tax took effect for most entities from 1 June 2023. The UAE has double tax treaties with over 130 countries (UAE Ministry of Finance, 2024). Small Business Relief covers businesses with revenue under AED 3 million through 31 December 2026 (FTA Ministerial Decision No. 73 of 2023). These five numbers define the landscape for anyone living and working in the UAE right now.

Here's the thing: the UAE has no personal income tax. Your salary, your bonus, your end-of-service gratuity, all tax-free, full stop. But corporate tax for UAE residents is a real and growing compliance obligation if you own or operate a business here. The boundary between personal income (tax-free) and business income (potentially taxable at 9%) is the single most important line you need to understand in 2026.

This guide explains exactly how corporate tax for UAE residents works, who pays, who doesn't, how employed residents and company shareholders are each treated, when a Tax Residency Certificate becomes essential, and which misconceptions could cost you real money if left uncorrected.

What Is Corporate Tax for UAE Residents and Why the Distinction Matters

Corporate tax for UAE residents is a 9% federal tax on business profits above AED 375,000 earned by UAE-registered companies or qualifying natural persons. It does not apply to salaries or employment income. UAE residents pay 0% personal income tax, the corporate tax obligation only arises when you operate a business.

The Core Rule: Personal Income Is Tax-Free, Business Profits Are Not

UAE residents pay 0% on salaries, wages, bonuses, and investment returns received as individuals. This hasn't changed under the corporate tax regime and applies to every UAE resident regardless of nationality. What changed in June 2023 is the treatment of business profits.

Business profits earned through a UAE-registered company, or as a natural person conducting business, are subject to corporate tax at 9% above AED 375,000. That threshold is the small business relief floor, and it applies to all taxable persons. The governing legislation is Federal Decree-Law No. 47 of 2022, which you can read in full on the UAE Federal Tax Authority portal.

Consider this: an expat software engineer earning AED 30,000 per month in salary pays zero income tax. The same engineer running a UAE LLC on the side with AED 500,000 in annual profits owes corporate tax on AED 125,000 of those profits (the portion above AED 375,000), that's AED 11,250 in tax. The salary is untouched. The business profit is not. For a deeper look at the legislative framework, see our guide to UAE corporate tax explained.

Why This Matters More Than Ever for UAE Business Owners

Corporate tax took effect for financial years starting on or after 1 June 2023. Most UAE companies have now completed at least one full tax year under the regime. That means filing deadlines, due 9 months after financial year-end, are either passed or approaching fast.

Residents who previously operated businesses informally, or assumed "no tax in UAE" covered everything, now face real compliance obligations. The Federal Tax Authority (FTA) requires registration, annual filing, and payment. Non-compliance carries administrative penalties that accumulate quickly.

A UK expat who set up a trading company in Dubai in 2021 and never revisited the tax question may have been caught off guard when FY2024 filings became mandatory. Understanding your exposure now is considerably cheaper than correcting it under audit.

How Corporate Tax Affects Different Types of UAE Residents

Corporate tax affects UAE residents differently depending on how they earn income. Employees pay nothing extra, their salary is tax-free. Natural persons conducting business activity become taxable if turnover exceeds AED 1 million. Company shareholders are not personally taxed on dividends, the company itself pays corporate tax on its profits.

Employed Residents: Your Salary Stays Tax-Free

If your only income source is employment, salary, housing allowance, annual bonus, or end-of-service gratuity, you have zero corporate tax exposure as an individual. This applies to every UAE resident: Emirati nationals, GCC citizens, and expats from any country. Your employment income is simply outside the corporate tax net.

Passive investment income received personally, dividends from UAE companies, rental income from a personally held property, is also generally outside the CT scope for natural persons. The company distributing those dividends has already settled its CT liability before paying you.

Take a marketing director at a Dubai-based multinational earning AED 420,000 per year in salary and receiving AED 50,000 in dividends from a UAE company she invested in. She pays no personal income tax on either amount. The company paid its CT before declaring the dividend. She receives the net amount, tax-free in her hands.

Natural Persons in Business: The AED 1 Million Threshold You Need to Know

Natural persons conducting business activity in the UAE, including sole traders operating under a trade license, are subject to corporate tax only if their annual turnover exceeds AED 1,000,000. Below that, no registration and no filing are required.

Above AED 1M, the natural person must register with the FTA via the EmaraTax portal, file annual returns, and pay 9% on taxable income above AED 375,000. This catches many high-earning consultants, creative professionals, and tech contractors by surprise, the assumption that "personal = always tax-free" doesn't hold once you cross that threshold.

Here's a worked example. An independent management consultant in Abu Dhabi with AED 1.4M in annual billings must register for corporate tax. After allowable deductions, her net taxable income is AED 500,000. She pays 9% on AED 125,000 (the amount above AED 375,000), that's AED 11,250 in tax. Not ruinous, but real. And worth planning for before the filing deadline, not after.

Company Shareholders: How Dividends Are Treated Under UAE Corporate Tax

When a UAE company pays corporate tax on its profits, individual shareholders receiving dividends do not pay a second layer of tax. There is no dividend withholding tax on distributions to UAE resident individuals. Tax is paid once, at the entity level, not again at shareholder level.

This structural advantage matters enormously for business owners deciding between salary and dividend as a remuneration strategy. Shareholders who receive dividends from foreign companies may also benefit from participation exemption rules under certain qualifying conditions (UAE FTA, 2023).

Three co-founders own equal shares in a Dubai mainland LLC earning AED 900,000 in profit. The company pays 9% CT on AED 525,000 (the amount above the threshold), totalling AED 47,250. The remaining AED 852,750 is distributed as dividends. None of the three founders pay additional personal tax on those dividends. For support on structuring this correctly, see accounting and tax compliance at Dubai South.

UAE Resident Type vs. Corporate Tax Treatment

Resident Type | CT Obligation? | Key Threshold | Tax Rate |

|---|---|---|---|

Employed resident (salary only) | ❌ None | N/A | 0% |

Sole trader / natural person in business | ✅ Above AED 1M turnover | AED 1,000,000 | 9% above AED 375K |

UAE company (mainland or free zone) | ✅ Mandatory registration | No revenue threshold | 9% above AED 375K |

Company shareholder (dividends) | ❌ No personal tax on dividends | Company pays CT | 0% at shareholder level |

Qualifying Free Zone Person (QFZP) | ✅ Must actively qualify | Substance + income conditions | 0% qualifying / 9% non-qualifying |

Small business (revenue under AED 3M) | ✅ Relief available to Dec 2026 | AED 3,000,000 | 0% under Small Business Relief |

UAE Corporate Tax for Expats: A Step-by-Step Breakdown of Your Obligations

UAE corporate tax for expats follows the same rules as for all UAE residents. Employment income is tax-free. If you own a UAE company, that entity files and pays corporate tax. If you operate a business as a natural person and exceed AED 1M in turnover, you register as an individual taxable person. Your home country's tax treaties with the UAE may also affect your overall position.

Step 1: Identify Whether You Have a Business Activity in the UAE

Ask yourself: do you earn income through a UAE-registered company or trade license? If yes, you have a business activity that falls within the CT framework. Employment income alone carries no CT obligation for you as an individual, regardless of the salary amount.

Investment income, interest, dividends, capital gains on personal investments, is generally outside the CT scope for natural persons (UAE FTA, 2023). A British expat in Dubai who holds a salaried role and is a 50% shareholder in a UAE LLC has a clean personal position. The LLC has CT obligations. The individual does not, their salary and dividend receipts are both outside personal CT.

Step 2: Determine If Your Business Must Register with the FTA

All UAE companies, mainland and free zone, that are juridical persons must register for corporate tax. There is no turnover threshold for companies; registration is mandatory from incorporation. Natural persons must register only if annual turnover exceeds AED 1M.

Registration is completed through the FTA's EmaraTax portal, with deadlines tied to the company's financial year-end. A free zone company incorporated at Dubai South Business Hub Free Zone with zero revenue still needs to register and file a nil return. Penalties for late registration apply and accumulate monthly. Register early.

Step 3: Confirm Your Tax Residency Status and Treaty Position

Even as a UAE tax resident, your home country may still assert taxing rights over your worldwide income. The UAE has double tax treaties with over 130 countries (UAE Ministry of Finance, 2024), these treaties are your primary defence against double taxation.

A UAE Tax Residency Certificate (TRC), issued by the FTA, is your formal proof of UAE tax residence for treaty purposes. To qualify, you generally need 183+ days of physical presence in the UAE per year (or 90 days under certain conditions for UAE nationals and residents with a UAE establishment). An Indian national running a consultancy from Dubai who receives tax demands from Indian authorities can use a UAE TRC, combined with the UAE-India double tax treaty, to establish the UAE as his primary tax jurisdiction. For support with this process, explore DSBH banking and taxation services.

Is a UAE company always required to register for corporate tax even with no income?

Yes. All juridical persons, mainland and free zone companies, must register with the Federal Tax Authority via EmaraTax regardless of revenue level. The AED 1M threshold applies only to natural persons conducting business activity. A company with zero revenue must still register and file a nil return by the deadline tied to its financial year-end.

Qualifying Free Zone Income and the 0% Corporate Tax Rate

UAE free zone companies that meet qualifying conditions, including having substance in the free zone, deriving qualifying income, and complying with transfer pricing rules, can benefit from a 0% corporate tax rate on qualifying income. This does not mean all free zone profits are automatically tax-free; the conditions must be actively met.

What Counts as a Qualifying Free Zone Person

A Qualifying Free Zone Person (QFZP) is a free zone entity that satisfies four core conditions: adequate economic substance in the free zone, income that qualifies under the relevant ministerial decision, no election to be taxed under the standard CT regime, and compliance with transfer pricing documentation requirements (UAE FTA, 2023).

QFZPs pay 0% on qualifying income and 9% on non-qualifying income, for example, income from UAE mainland transactions above the de minimis threshold (the lower of AED 5 million or 5% of total revenue). A logistics company at Dubai South Business Hub Free Zone with genuine operational substance, staff on-site, management decisions made locally, transactions primarily with non-UAE counterparties, is well-positioned to qualify for the 0% rate on international trade income. For a full breakdown, see our guide to corporate tax benefits in Dubai free zones.

Common Mistakes UAE Residents Make About Free Zone Tax Status

Three mistakes come up repeatedly in practice:

Mistake 1: Assuming free zone incorporation automatically means 0% tax. It does not. You must actively qualify as a QFZP, meeting substance, income type, and compliance conditions every tax period.

Mistake 2: Conducting significant business with UAE mainland clients without accounting for the tax consequence. Income from mainland transactions above the de minimis threshold is taxed at 9%, not 0%.

Mistake 3: Neglecting economic substance requirements. The FTA expects real operations, staff, physical presence, genuine decision-making, not just a registered address.

A consultancy in a UAE free zone billing 80% of its revenue to Dubai mainland clients may find that most of its income does not qualify for the 0% rate. Discovering this at audit is far more painful than identifying it at the planning stage. Engaging accounting and tax compliance at Dubai South from day one keeps your QFZP status defensible.

The UAE Tax Residency Certificate: What It Is and When You Need One

A UAE Tax Residency Certificate (TRC) is an official document issued by the Federal Tax Authority confirming that an individual or company is a UAE tax resident. It is used to claim protection under double tax treaties, preventing your home country from taxing UAE-sourced income. It does not reduce your UAE corporate tax obligations.

Who Should Apply for a UAE Tax Residency Certificate

The TRC is most valuable for four groups:

Expats who retain tax obligations in their home country, Americans subject to US worldwide taxation, UK residents who have not formally severed UK tax ties

Business owners receiving income from foreign clients who want treaty protection against double taxation

Individuals who recently relocated to the UAE and need to formally establish their primary tax jurisdiction

UAE companies transacting with foreign counterparties where withholding tax reductions are available under a DTT

A German national who moved to Dubai in 2023 and still owns a rental property in Frankfurt is a clear example. German tax authorities may assert a claim on that rental income. A UAE TRC, combined with the UAE-Germany double tax treaty, is the instrument that blocks the double charge, it formally establishes the UAE as his primary tax jurisdiction. The TRC is issued by the UAE FTA and is valid for one year; renewal is required annually (UAE FTA, 2023).

Important Considerations for Expats Managing Dual Tax Exposure

Worth flagging: a TRC does not eliminate your home country filing obligations in all cases. US citizens, for example

References

Editorial sources available on request. Full citation list is being compiled.