Topic Summary

By Editorial Team , UAE business setup and tax compliance specialists with direct experience advising free zone and mainland companies on FTA obligations. Full bio →

Last updated: June 2026

By Editorial Team, UAE business setup and tax compliance specialists with direct experience advising free zone and mainland companies on FTA obligations. Full bio →

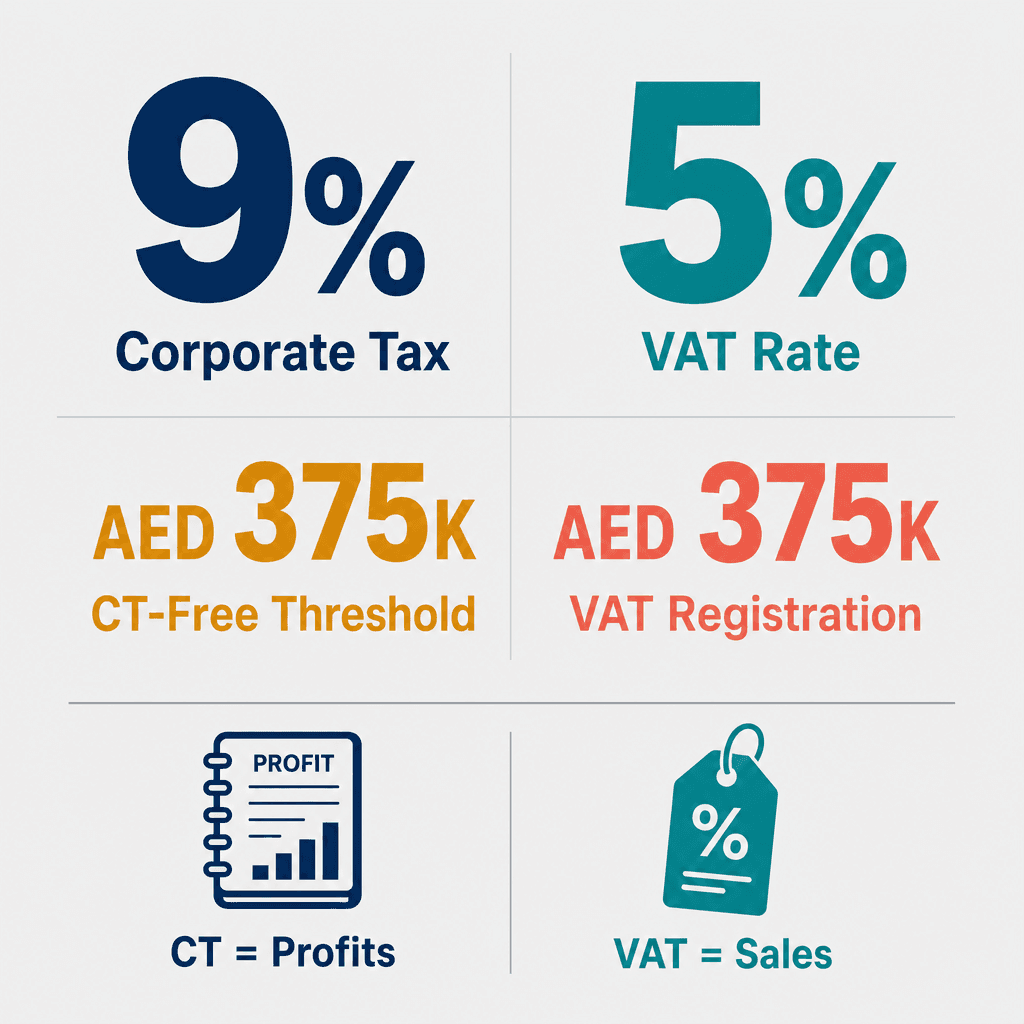

In 2026, the UAE Federal Tax Authority (FTA) administers two entirely separate taxes on businesses: a 9% corporate tax (CT) on net profits, introduced under Federal Decree-Law No. 47 of 2022 (FTA, 2023) [1], and a 5% VAT on taxable supplies, in force since 1 January 2018 under Federal Decree-Law No. 8 of 2017 (FTA, 2018) [2]. The mandatory VAT registration threshold sits at AED 375,000 in annual taxable supplies (FTA, 2018) [3]. The CT 0% band covers taxable income up to AED 375,000 (FTA, 2023) [4]. Both taxes are filed through the EmaraTax portal at tax.gov.ae (FTA, 2023) [5]. Yet hundreds of businesses still conflate the two, filing on the wrong schedule, treating VAT receipts as income, or assuming one registration covers the other. It doesn't.

This guide breaks down the corporate tax vs VAT UAE distinction in plain terms: what each tax is, who pays it, how it's calculated, when it's filed, and how the two interact so you can manage both without costly errors.

What Corporate Tax and VAT in the UAE Actually Are: Definitions That Clear the Confusion

Corporate tax in the UAE is a 9% tax on a business's net profits, introduced under Federal Decree-Law No. 47 of 2022. VAT is a 5% consumption tax charged on the sale of goods and services, collected from customers and remitted to the FTA. When you look at the difference between corporate tax and VAT Dubai businesses face, the starting point is simple: one taxes what you earn, the other taxes what you sell.

What Is UAE Corporate Tax and What Does It Tax?

Corporate tax (CT) is levied on taxable income, net profit after allowable deductions, not on revenue or sales. It was introduced by Federal Decree-Law No. 47 of 2022, effective for financial years starting on or after 1 June 2023 (FTA, 2023). The standard rate is 9% on taxable income above AED 375,000, with a 0% rate on income up to that threshold. It applies to juridical persons (companies) and, in certain cases, resident natural persons conducting business in the UAE. Read the full breakdown in our UAE corporate tax explained guide.

Here's a concrete example. A Dubai mainland LLC with AED 1.2 million net profit pays 9% only on the AED 825,000 above the threshold, roughly AED 74,250 in CT for that year. The first AED 375,000 is taxed at zero.

What Is UAE VAT and What Does It Tax?

VAT is a consumption tax, introduced on 1 January 2018 under Federal Decree-Law No. 8 of 2017 at a flat 5% rate. Businesses act as collection agents: they charge VAT on sales (output tax), reclaim VAT paid on purchases (input tax), and remit the net difference to the FTA. VAT applies to taxable supplies of goods and services, not to profit. The mandatory registration threshold is AED 375,000 in taxable supplies per year (FTA, 2018). For the registration process, see our UAE VAT registration guide.

A Dubai-based marketing agency invoicing a client AED 100,000 adds AED 5,000 VAT (5%). That AED 5,000 is collected on behalf of the FTA, it is never the agency's income.

Corporate Tax vs VAT in the UAE: Head-to-Head Comparison

The corporate tax and VAT comparison UAE businesses need comes down to this: CT applies to business profits at 9%; VAT applies to sales at 5%. CT is filed annually; VAT is filed monthly or quarterly. Both are administered through EmaraTax, but they are separate registrations, separate returns, and separate payment obligations. Confusing the two is one of the most common compliance errors the FTA sees.

Side-by-Side: How the Two Taxes Differ Across Every Key Dimension

Corporate Tax vs VAT in the UAE: Complete Comparison

Feature | Corporate Tax (CT) | VAT |

|---|---|---|

Tax Type | Direct tax on profits | Indirect consumption tax on sales |

Rate | 9% (0% up to AED 375,000) | 5% flat rate |

What Is Taxed | Net profit (after deductions) | Value of taxable goods and services supplied |

Registration Threshold | All UAE juridical persons must register | AED 375,000 taxable supplies/year (mandatory) |

Calculation Method | Taxable income × 9% | Output tax minus input tax = VAT payable |

Filing Frequency | Annually (within 9 months of year-end) | Monthly or quarterly (28 days after period-end) |

Filing Portal | EmaraTax (tax.gov.ae), separate CT account | EmaraTax (tax.gov.ae), separate VAT TRN |

Who Bears the Cost | The business (paid from profits) | The end consumer (collected by business) |

Consider a wholesale trading company in Dubai South with AED 5 million revenue, AED 4 million costs, and AED 1 million net profit. It collects and remits VAT on its AED 5 million in sales. Separately, it pays CT on its AED 625,000 taxable income (AED 1M net profit minus the AED 375,000 threshold), that's AED 56,250 in CT. Two completely separate calculations, two separate payments.

The Key Interaction: Why VAT Is Never Taxable Income for Corporate Tax

VAT collected from customers is held in trust for the FTA. It passes straight through the business and is never the business's income. When calculating corporate taxable income, VAT on sales is excluded from revenue, and input VAT on purchases is also excluded because it's either reclaimed or treated as a cost separately.

Warning: If a retailer shows AED 1.05 million in bank receipts (AED 1M sales plus AED 50,000 VAT collected), only AED 1 million counts as revenue for CT purposes. Treating the full AED 1.05 million as income overstates taxable profit by AED 50,000, and overstates your CT bill by AED 4,500. This is a common bookkeeping error that also triggers FTA audit queries. For help keeping the two clean, see accounting and tax compliance at Dubai South.

Who Must Register for Each Tax, and When

Virtually all UAE-based juridical persons must register for corporate tax, regardless of profit level. VAT registration is mandatory only when taxable supplies or imports exceed AED 375,000 per year. So if you're asking "do I need to pay both corporate tax and VAT UAE?", for most active businesses, the answer is yes. Two separate registrations, two separate compliance tracks running simultaneously.

Corporate Tax Registration: Who Is Covered and Who Is Exempt

All UAE-incorporated companies and foreign companies managed and controlled from the UAE must register for CT, even with zero revenue. Exempt entities include UAE government bodies, qualifying public benefit entities, qualifying investment funds, and natural resource extraction businesses subject to emirate-level taxation. Free zone companies can qualify for a 0% CT rate on qualifying income but must still register and file. Penalties for late CT registration can reach AED 10,000 (FTA penalty schedule). Check our guide on non-compliance risks and fines in UAE for the full penalty table.

A newly incorporated free zone company in Dubai South with zero revenue in its first year still must register for corporate tax. The registration obligation is not contingent on generating profit.

VAT Registration: Mandatory vs Voluntary Thresholds

Mandatory registration: taxable supplies or imports exceed AED 375,000 in the previous 12 months, or are expected to in the next 30 days (FTA, 2018).

Voluntary registration: available when taxable supplies or expenses exceed AED 187,500, useful for reclaiming input VAT before hitting the mandatory threshold (FTA, 2018).

Zero-rated supplies (exports, international transport, certain food items) and exempt supplies (bare land, residential property) affect whether registration is needed.

B2B exporters may not need to charge VAT but can still benefit from voluntary registration to reclaim input tax on UAE purchases.

A UAE startup with AED 200,000 in annual B2B consultancy fees sits below the mandatory threshold. But it voluntarily registers for VAT so it can reclaim input VAT on its AED 80,000 in software and office expenses, a net cash benefit that many small businesses miss. See the full process in our UAE VAT registration guide.

Is there a way to be exempt from both corporate tax and VAT in the UAE?

Rarely. Certain government entities and qualifying public benefit organisations are exempt from CT. VAT exemption applies only to specific supply categories, not entire businesses. Most commercial enterprises will carry at least the CT registration obligation, and most with revenues above AED 375,000 will carry both. Assuming otherwise is one of the costlier compliance mistakes you can make.

5 Steps to Calculate and File Both Taxes Without Mixing Them Up

Keeping corporate tax and VAT separate in the UAE requires clean bookkeeping from day one. Record VAT collected as a liability, not revenue. Calculate CT on net profit excluding VAT. File VAT returns quarterly or monthly via EmaraTax. File your CT return annually within 9 months of your financial year-end. Pay each through separate FTA payment channels. Here's how that works in practice, with UAE CT vs VAT explained step by step.

Step 1 to Step 3: Setting Up Clean Books and Filing VAT

Configure your accounting software to post VAT collected as a current liability account, not revenue, from the very first invoice you issue.

Reconcile your VAT return each period: output tax (VAT on sales) minus input tax (VAT on purchases) equals VAT payable or refundable. Submit via EmaraTax on the quarterly or monthly schedule assigned by the FTA. The deadline is 28 days after the end of each tax period (FTA).

Retain all tax invoices for a minimum of 5 years, the FTA can audit up to 5 years back (FTA guidance). Most UAE businesses are assigned quarterly VAT filing; high-volume businesses may be placed on monthly cycles.

A Dubai trading company files VAT quarterly. In Q1, it charged AED 25,000 output VAT and paid AED 10,000 input VAT on stock purchases, it remits AED 15,000 to the FTA by the 28th day after quarter-end. Clean, straightforward, and entirely separate from its CT calculation.

Step 4 to Step 5: Calculating Taxable Income and Filing Corporate Tax

Prepare financial statements under IFRS or another FTA-accepted accounting standard. Strip out all VAT amounts from revenue and expense lines before calculating net profit. VAT figures have no place in your CT base.

Apply the CT calculation: net profit minus allowable deductions minus the AED 375,000 small business threshold equals taxable income, multiplied by 9%. File the CT return via EmaraTax within 9 months of your financial year-end. CT payment is due at the same time as filing, there's no separate payment deadline. Tax losses can be carried forward to offset future taxable income, subject to conditions (FTA guidance).

A company with a financial year ending 31 December 2024 must file its CT return and pay any CT due by 30 September 2025. Miss that date and FTA penalties apply immediately. For structured support on both filings, accounting and tax compliance at Dubai South offers on-site advisory.

Can You Be Subject to Both Corporate Tax and VAT in the UAE at the Same Time?

Yes. Most active UAE businesses face both corporate tax and VAT simultaneously. CT applies because the business generates profit; VAT applies because it makes taxable supplies above the registration threshold. Being registered for one does not cover the other. The question "do I need to pay both corporate tax and VAT UAE?" has a straightforward answer for the majority of businesses: yes, and each requires its own registration, return, and payment. This is the heart of the corporate tax and VAT comparison UAE businesses need to understand.

How the Two Taxes Coexist for Most UAE Businesses

A business can simultaneously owe VAT on its quarterly sales and CT on its annual profit. These are independent liabilities calculated on entirely different bases. Paying your quarterly VAT on time does not reduce your CT liability. There is one useful interaction worth knowing: VAT expenses that are not recoverable as input tax (for example, VAT on entertainment or staff meals, which are blocked items under FTA rules) can be deducted as a business expense when calculating taxable income for CT purposes (FTA guidance).

A Dubai South logistics company pays AED 37,500 in VAT for Q3 and separately calculates AED 56,250 in CT for the full financial year. Different bases, different periods, different forms, the two figures are completely unrelated.

Scenarios Where a Business Might Face Only One Tax

Scenario A: A small consultancy with AED 200,000 annual revenue sits below the VAT mandatory threshold. No VAT obligation, but CT registration and filing are still required.

Scenario B: A UAE branch of a foreign bank making only exempt financial services supplies has no VAT on outputs. It is fully subject to CT on profits.

Scenario C: A qualifying free zone person with qualifying income taxed at 0% CT is still subject to VAT on any standard-rated supplies made to UAE mainland customers.

A freelance designer earning AED 180,000 per year sits below the mandatory VAT threshold and below the CT taxable income threshold, but still must register for CT and file a nil or low-liability return. The registration obligation doesn't disappear just because the tax bill is zero. See our UAE corporate tax explained guide for the full scope of who must register.

How Each Tax Is Filed: Portals, Deadlines, and Frequency

Both corporate tax and VAT are filed through the FTA's EmaraTax portal at tax.gov.ae. VAT returns are due 28 days after each tax period ends, monthly or quarterly depending on your assigned cycle. Corporate tax returns are filed annually, due within 9 months of your financial year-end. That's the core of UAE CT vs VAT explained from a filing standpoint, same portal, completely separate workflows.

EmaraTax: One Portal, Two Separate Tax Accounts

EmaraTax is the single portal for all FTA registrations, returns, and payments. Despite using the same platform,

References

[1] Source pending — please add URL and publisher.

[2] Source pending — please add URL and publisher.

[3] Source pending — please add URL and publisher.

[4] Source pending — please add URL and publisher.

[5] Source pending — please add URL and publisher.