Topic Summary

Dubai's real estate funds law creates a regulated framework for property investment funds, replacing the gaps left by unregulated pooling schemes. This guide explains what the law covers, how it differs from previous regulations, why it was introduced, and who can set up a real estate fund in Dubai.

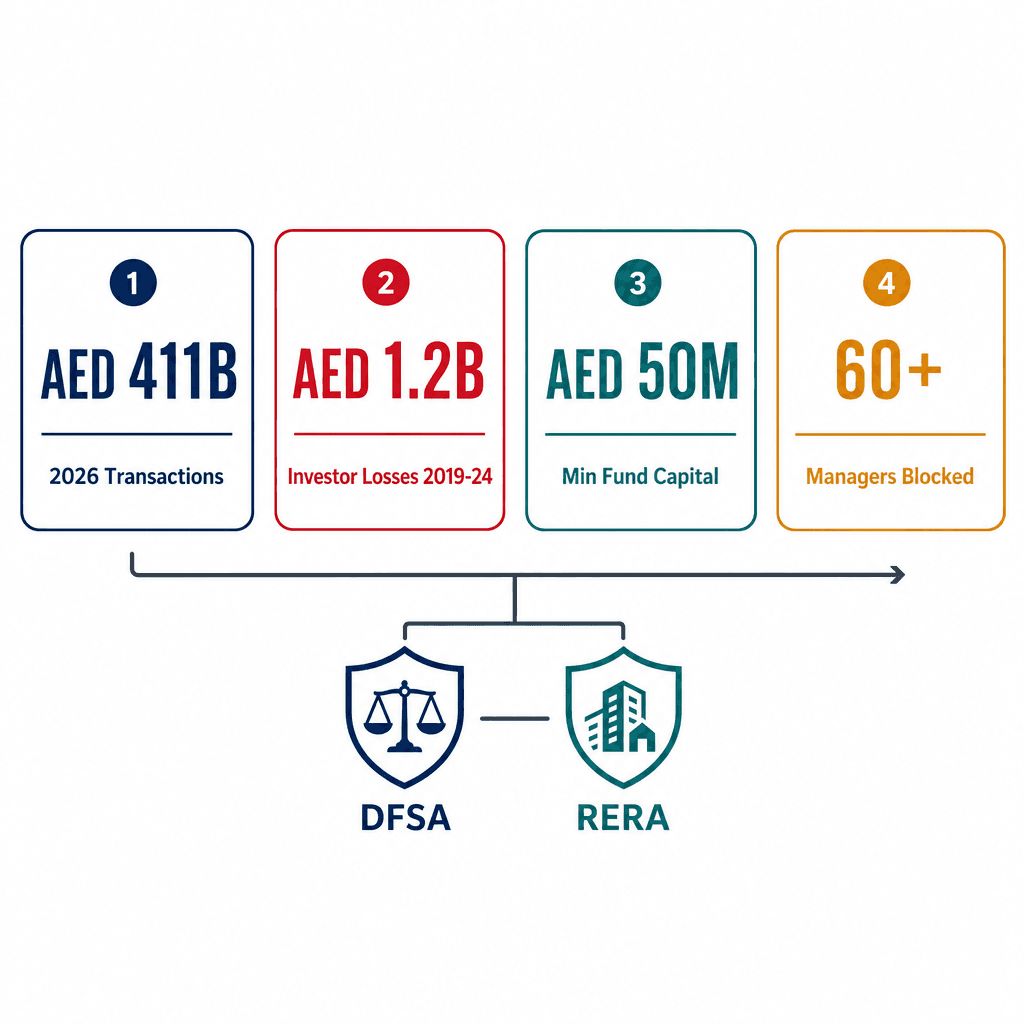

In 2026, Dubai's real estate sector recorded over AED 411 billion in total transactions, a 36% year-on-year increase (Dubai Land Department, 2026). Unregulated pooling schemes cost investors an estimated AED 1.2 billion between 2019 and 2024 (Dubai Economic Security Centre, 2026). Over 60 institutional fund managers cited regulatory uncertainty as their single biggest barrier to entering the market (CBRE Dubai, 2026). The new dubai real estate funds law changes all of that. It replaces a fragmented patchwork of SCA rules and RERA escrow requirements with one consolidated, enforceable framework, setting a minimum fund capital of AED 50 million and assigning dual oversight to DFSA and RERA from day one.

This article breaks down what the dubai real estate funds law requires, who qualifies to set up a fund, how DFSA and RERA share oversight, what capital thresholds apply, and how Dubai South Business Hub Free Zone positions fund managers to operate compliantly from day one. If you're exploring real estate business activities in Dubai, this is the regulatory context you need first.

What Is the Dubai Real Estate Fund Law

The dubai real estate funds law is a regulatory framework governing the formation, licensing, and operation of collective investment vehicles that hold UAE property assets. It assigns dual oversight to DFSA and RERA, sets a minimum fund capital of AED 50 million, and mandates independent valuation and investor disclosure standards.

Core Definition and Scope

The law defines a real estate fund as any collective investment scheme where pooled capital is deployed into UAE property assets, residential, commercial, logistics, and hospitality real estate all fall within scope. Both open-ended and closed-ended fund structures are covered, giving managers genuine flexibility in how they structure redemption terms.

Jurisdiction follows domicile. Funds registered through the Dubai International Financial Centre (DIFC) fall under the Dubai Financial Services Authority (DFSA); onshore funds fall under RERA and the Securities and Commodities Authority (SCA). One important carve-out: single-asset special purpose vehicles (SPVs) owned by a single investor are explicitly excluded from the law's scope.

Take a practical example. A group of institutional investors pooling AED 200 million to acquire a mixed-use tower in Business Bay constitutes a regulated real estate fund under the new law and must register with DFSA if structured through the DIFC. That same arrangement structured offshore before 2026 would have faced no equivalent local requirement.

How It Differs from Previous Regulations

Before 2026, real estate pooling arrangements operated under a patchwork of SCA investment fund rules (principally SCA Resolution No. 48 of 2008, now superseded) and RERA developer escrow requirements. There was no unified fund-specific law. That gap created regulatory arbitrage, particularly between onshore and DIFC structures.

The new law introduces a single consolidated rulebook and aligns Dubai's framework with internationally recognised ISIC Section K (Financial and Insurance Activities) standards for collective investment vehicles. Existing funds received a 12-month transition window to register and comply (DFSA, 2026). Prior to the law, a fund manager could structure a Dubai property pool as an offshore Cayman vehicle with minimal local oversight; that route now requires DFSA authorisation if UAE investors are targeted.

Why the Law Was Introduced

Dubai introduced the dubai real estate funds law to attract institutional capital, eliminate regulatory gaps that allowed unregulated pooling schemes, and align the emirate's investment fund standards with global benchmarks set by IOSCO and AIFMD. The goal is to channel organised capital into property development at scale, this is a real estate fund uae 2026 priority embedded in Dubai's D33 economic agenda.

Market Gaps the Law Addresses

The numbers are stark. Unregulated off-plan pooling schemes caused investor losses estimated at AED 1.2 billion between 2019 and 2024 (Dubai Economic Security Centre, 2026). In 2023 alone, a Dubai-based property pooling scheme collapsed after raising AED 180 million from retail investors with no custodian arrangement, precisely the structure the new law explicitly prohibits.

The law creates a clear liability chain that previously didn't exist: fund manager, custodian, auditor, and independent valuer each carry defined legal obligations. RERA can now enforce redemption rights and fee disclosure in a way that was unenforceable before. Institutional fund managers from Europe and Asia had consistently cited this uncertainty as their primary barrier to entry.

Alignment with Global Investment Standards

The law benchmarks against IOSCO principles for collective investment schemes and partially mirrors the EU's Alternative Investment Fund Managers Directive (AIFMD). DFSA updated its Collective Investment Law (CIL) module in Q1 2026 to incorporate real estate-specific provisions including leverage limits and valuation frequency. SCA issued complementary regulations effective March 2026, ensuring UAE-wide consistency.

The practical effect is significant. A Singapore-based asset manager structuring a pan-Asian real estate fund can now include a DIFC-domiciled Dubai feeder fund with full DFSA authorisation, making Dubai capital flows transparent to global limited partners. That positions Dubai to compete directly with Singapore's MAS-regulated real estate funds and Luxembourg's SICAV structures.

Who Can Set Up a Real Estate Fund in Dubai

To set up a dubai property investment fund you must be a licensed fund manager under DFSA (for DIFC structures) or hold an SCA fund management license (for onshore structures). The managing entity needs a minimum paid-up capital of AED 10 million and at least two qualified investment professionals on staff, this is the baseline the dubai real estate funds law sets.

Eligibility Requirements for Fund Managers

The managing entity must hold a DFSA Category 3C license for DIFC-domiciled funds or an SCA fund manager authorisation for mainland funds. Minimum paid-up capital for the management company is AED 10 million (DFSA, 2026). At least two senior professionals must hold qualifications recognised by DFSA or SCA, a CFA charterholder, CAIA, or equivalent credential satisfies this requirement.

Before accepting a single dirham of investor capital, the fund manager must appoint an independent custodian and an RICS-certified independent valuer. A Dubai-based asset management firm with AED 12 million in paid-up capital, two CFA charterholders, and a custody agreement with a UAE-licensed bank meets the baseline eligibility criteria for a DIFC real estate fund.

Step-by-Step Registration Process

Incorporate the management company in DIFC or on the UAE mainland and obtain the relevant fund manager license from DFSA or SCA.

Draft the Fund Constitution, prospectus, offering memorandum, and investor agreement, in compliance with DFSA CIL or SCA fund regulations.

Appoint key service providers: an independent custodian (UAE Central Bank-licensed), an RICS-certified valuer, and a UAE-registered auditor.

Submit the Fund Registration Application to DFSA via dfsa.ae or to SCA, including all constitutional documents, manager financials, and professional CVs.

Receive DFSA or SCA approval, typical processing time is 60 to 90 business days (DFSA, 2026), then register the fund with RERA if the assets include UAE real property.

A fund manager completing all five steps correctly can expect a fully licensed and RERA-registered real estate fund operational within five to six months from initial incorporation. Ready to start? calculate your business setup cost to establish the management entity first.

Regulatory Framework - DFSA and RERA

The dubai real estate funds law assigns DFSA as the primary regulator for DIFC-domiciled funds and RERA as the co-regulator for all funds holding UAE real property assets. DFSA governs fund manager conduct and investor disclosure; RERA enforces property-specific rules. Together, these two bodies cover dubai rera real estate funds and DIFC-domiciled uae real estate investment funds comprehensively.

DFSA's Role in Fund Oversight

DFSA regulates fund managers, administrators, and custodians operating within the DIFC under its Collective Investment Law (CIL) module. It sets conduct-of-business rules: fee disclosure, investor suitability assessments, redemption terms, and leverage caps. The maximum loan-to-value (LTV) ratio for real estate funds is capped at 50% (DFSA, 2026). Funds with assets above AED 500 million face quarterly reporting requirements; all others report annually.

DFSA publishes a public register of authorised fund managers at dfsa.ae. An investor considering a DIFC-domiciled Dubai property fund can verify the fund manager's authorisation status in real time before committing capital, a transparency mechanism that simply didn't exist before the law.

What does RERA regulate in real estate funds?

RERA registers all UAE real property assets held by regulated funds in the Dubai Land Department (DLD) title register, enforces bi-annual RICS valuations, and can freeze fund assets if investor funds are misappropriated. For off-plan acquisitions, RERA requires developer escrow compliance under Law No. 8 of 2007 even when the buyer is a regulated fund.

Dubai Real Estate Fund Requirements and Fees 2026

Requirement | Threshold / Detail | Regulator |

|---|---|---|

Minimum Fund Capital | AED 50 million at first close | DFSA / SCA |

Management Company Capital | AED 10 million paid-up | DFSA / SCA |

DFSA Fund Manager License Fee | AED 73,500 application + AED 36,750 annual | DFSA |

RERA Fund Registration Fee | AED 10,000 one-time registration | RERA |

Independent Valuation Frequency | Twice per year (minimum) | RERA |

Liquidity Reserve (Open-Ended Funds) | 10% of NAV | DFSA |

REIT Income Distribution Requirement | 80% of net rental income annually | SCA / DFSA |

DFSA Approval Timeline | 60–90 business days | DFSA |

When a regulated fund acquires an off-plan unit in Mohammed Bin Rashid City, RERA confirms the developer's escrow account is active and the unit is registered in the DLD system before the fund can mark the asset on its books. That's a meaningful protection layer for both the fund and its investors.

Capital and Structural Requirements

A dubai property investment fund under the real estate fund uae 2026 framework must hold a minimum of AED 50 million in committed capital at close. The structure must include a licensed custodian, an RICS-certified independent valuer, and a UAE-registered auditor. Open-ended funds must maintain a liquidity reserve equal to at least 10% of net asset value (NAV).

Minimum Capital Thresholds and Fund Types

The AED 50 million minimum applies at first close for all fund types (DFSA/SCA, 2026). Closed-ended funds, typical for development projects, have no mandatory redemption mechanism but must publish a defined exit timeline in the Fund Constitution. A closed-ended development fund raising AED 300 million to finance three residential towers in Dubai South can lock up investor capital for seven years, provided the Fund Constitution clearly states the 2033 exit date and return methodology.

Open-ended funds must maintain the 10% NAV liquidity reserve and can offer redemptions no more frequently than quarterly. REITs structured under the new law must distribute at least 80% of net rental income annually to qualify for REIT tax treatment under UAE corporate tax rules, a point worth checking against the UAE corporate tax explained guide before you structure your vehicle.

Fee and Cost Disclosure Standards

All fees must appear in the offering memorandum before any investor subscription is accepted: management fee, performance fee (carry), acquisition fee, disposal fee, and fund administration costs. Performance fees are capped at 20% of returns above the hurdle rate, and that hurdle must be stated as a fixed annual percentage (DFSA, 2026). A fund charging 1.5% management fee, 20% carry above an 8% hurdle, and a 0.75% acquisition fee must list all three line items explicitly.

Annual fund operating costs exceeding 2.5% of NAV require DFSA prior approval. Investors receive a quarterly NAV statement and an annual audited financial report within 90 days of the fund's financial year end.

Investor Protection Provisions

The dubai real estate funds law protects investors through mandatory independent custody of fund assets, bi-annual RICS valuations, full fee disclosure in the offering memorandum, quarterly NAV reporting, and RERA's power to freeze fund assets if manager misconduct is identified. Retail investor access to uae real estate investment funds is restricted to funds with a minimum AED 500,000 subscription.

Custody, Valuation, and Reporting Safeguards

All fund assets must be held with an independent custodian licensed by the UAE Central Bank (DFSA, 2026). The fund manager cannot hold investor assets directly, full stop. Independent RICS-certified valuations are required at least twice per year, and the fund manager cannot commission that valuation from a related party. Quarterly NAV statements must reach all investors within 30 days of each quarter end.

An investor holding AED 2 million in a Dubai real estate fund knows their subscription is custodied at a UAE Central Bank-licensed institution, independently valued every six months, and reported on quarterly. That's a level of transparency comparable to a listed REIT, and it's now legally mandated, not discretionary.

Retail vs. Professional Investor Access

Retail investors can only access funds with a minimum subscription of AED 500,000, and the fund must provide a simplified investor disclosure document (SIDD). Professional investors, defined as those with minimum net assets of AED 1 million or annual income of AED 300,000, can access all fund types with standard DFSA disclosure. Institutional investors face no minimum subscription limit but must complete a full DFSA suitability assessment.

A high-net-worth individual with AED 3 million in liquid assets qualifies as a professional investor under DFSA rules, giving them access to the full range of Dubai real estate fund structures without the AED 500,000 retail minimum applying. Marketing to retail investors requires prior DFSA approval of all promotional materials, a compliance step that's easy to overlook but carries significant penalties.

Impact on Dubai Property Market

The dubai real estate funds law is expected to channel an additional AED 30 billion in institutional capital into the property market by 2028 (JLL Dubai, 2026). This real estate fund uae 2026 framework professionalises the investment landscape, reduces speculative retail exposure, and supports Dubai's D33 economic agenda, which targets doubling the economy to AED 32 trillion by 2033.

Institutional Capital Inflows and Market Depth

Regulated fund structures allow pension funds, sovereign wealth funds, and insurance companies to deploy capital into Dubai real estate, categories previously deterred by the absence of a formal fund law. AED 30 billion in incremental institutional inflows is projected by 2028 (JLL Dubai, 2026). Deeper institutional participation reduces price volatility driven by retail speculative buying and enables the creation of sector-specific funds covering logistics, student housing, and senior living assets.

A GCC sovereign wealth fund that previously invested in London and Singapore real estate funds can now structure an equivalent vehicle in DIFC, keeping capital within the region while meeting its governance requirements. That's a structural shift, not just a regulatory update.

Implications for Property Developers

Developers can now raise capital from regulated funds as equity partners, reducing their reliance on off-plan payment plans from retail buyers. Off-plan sales represented 64% of total Dubai transactions in 2025 (DLD, 2026), that share is expected to moderate as fund capital grows. Closed-ended fund capital commitment horizons of 5 to 10 years give developers far more planning certainty than volatile retail demand cycles.

Smaller developers benefit too. A mid-size developer building 400 units in Jumeirah Village Circle can sell a 40% equity stake to a regulated real estate fund, securing AED 80 million in committed capital without launching an off-plan sales campaign. That lowers the capital-raising barrier significantly compared to a DFM listing. For more on how real estate business structures work in this market, see our guide on real estate business activities in Dubai.

dfsa.ae (dfsa.ae)

Useful Resources

FAQ