Topic Summary

By Editorial Team , Business setup and commercial insurance specialists covering UAE free zone regulations and risk management. Full bio →

Last updated: June 2026

By Editorial Team, Business setup and commercial insurance specialists covering UAE free zone regulations and risk management. Full bio →

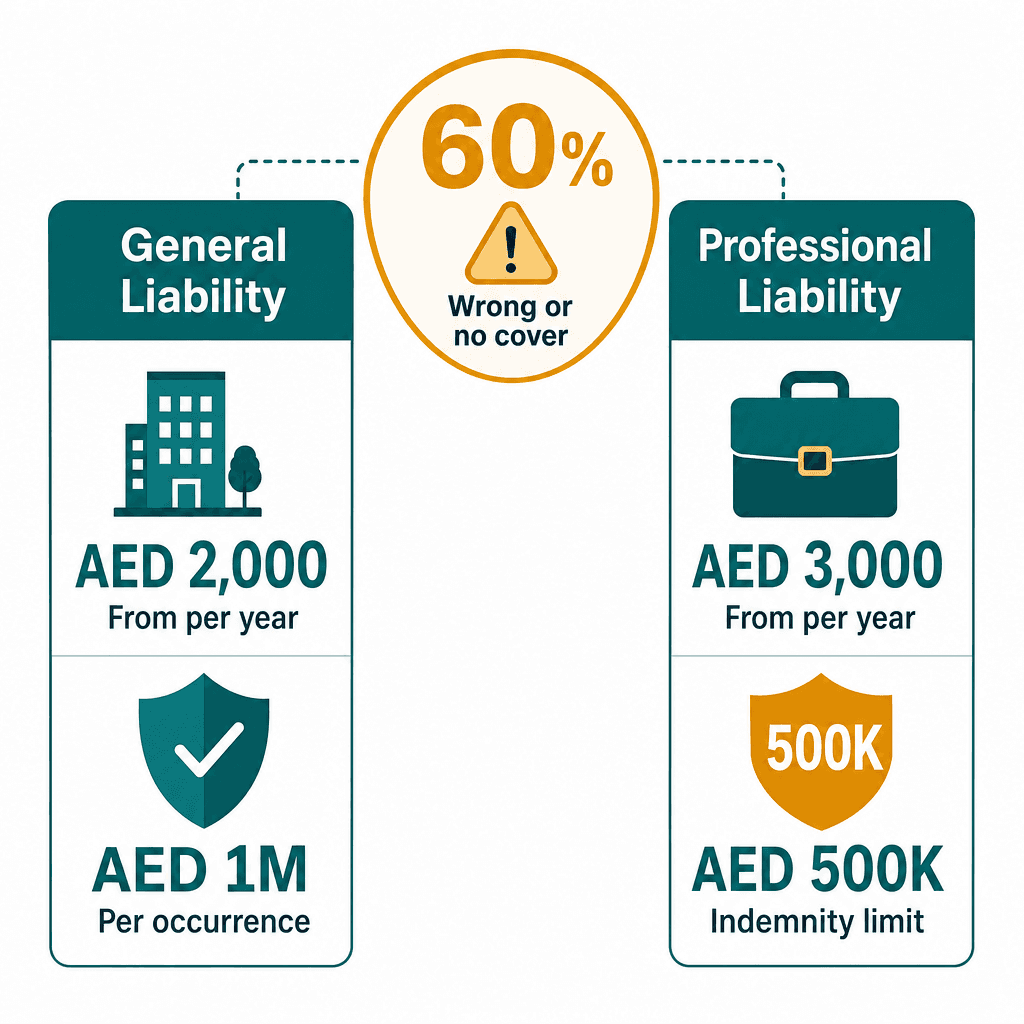

Insurance is one of the most overlooked line items in any UAE business setup budget, until something goes wrong. In 2026, an estimated 60% of small and mid-sized businesses operating in the UAE carry either the wrong commercial coverage or none at all, and most discover the gap only after a claim lands on their desk. General liability insurance UAE businesses rely on for physical and operational risks costs as little as AED 2,000 per year. Professional liability insurance Dubai professionals need for advice-based claims starts around AED 3,000 annually. Coverage limits for UAE SMEs typically begin at AED 1 million per occurrence for general liability and AED 500,000 for professional indemnity. Yet the two policies cover completely different risks, and buying one does not substitute for the other.

This guide breaks down exactly what each policy covers, who needs it, what it costs, and how to build the right coverage stack for your UAE business, so you stop overpaying for the wrong protection and stop leaving yourself exposed where it matters most.

What Is General Liability Insurance UAE and What Does It Actually Cover

General liability insurance UAE covers third-party claims for bodily injury, property damage, and advertising injury caused by your business operations. It protects businesses with physical premises, contractors, and event companies when a client, visitor, or member of the public suffers a loss connected to your operations or location.

Third-Party Bodily Injury and Property Damage Coverage

This is the core of any general liability policy. If a client slips on a wet floor in your Dubai retail showroom, the policy covers their medical costs and your legal defence fees. If your staff accidentally damage a client's property during a site visit, the same policy responds.

Medical costs and legal fees for third-party injuries at your premises

Accidental damage your team causes to a client's property during service delivery

Legal defence costs even if the claim against you is ultimately dismissed

Many UAE free zone authorities and government tender processes require proof of general liability coverage before issuing trade licenses or awarding contracts

Consider a fit-out contractor working on a Jumeirah villa who accidentally damages a neighbouring property's boundary wall. Without general liability insurance UAE coverage in place, that contractor pays repair costs and legal fees directly, easily AED 50,000 or more. Annual premiums for comparable coverage typically run AED 2,000–10,000+, depending on business size and risk profile. For a fuller picture of where insurance fits in your operating budget, the cost of running a business in Dubai guide is worth reviewing before you finalise your numbers.

Advertising Injury and What It Means for UAE Businesses

Advertising injury covers libel, slander, copyright infringement, and misappropriation of a competitor's advertising idea

Increasingly relevant as UAE businesses scale digital marketing and social media activity

Usually bundled into standard general liability policies at no additional premium, confirm this with your broker before assuming it's included

Does NOT cover professional mistakes or financial losses from advice, that gap belongs to professional liability insurance

A Dubai-based events company uses stock imagery in a campaign without proper licensing. The image owner files a copyright infringement claim. The advertising injury clause in their general liability policy covers the legal defence costs, a real-world scenario that plays out more often than most business owners expect as GCC digital ad spend continues to grow year on year.

What Is Professional Liability Insurance Dubai and Who Needs It

Professional liability insurance Dubai, also called Errors and Omissions (E&O) or Professional Indemnity insurance, covers claims arising from professional advice, errors, omissions, or negligence in delivering a service. Consultants, lawyers, architects, accountants, IT professionals, and healthcare providers are the primary buyers of this coverage in the UAE.

General Liability vs Professional Liability Insurance in the UAE: Side-by-Side Comparison

Feature | General Liability Insurance | Professional Liability Insurance |

|---|---|---|

What Triggers a Claim | Physical event: a visitor is injured, property is damaged, or advertising causes harm | Client alleges your advice, design, or deliverable caused them a financial loss |

What It Pays For | Medical costs, property repair bills, and legal defence for third-party physical claims | Legal defence costs and settlements for negligence, errors, or omissions in professional services |

Who Typically Needs It | Retailers, contractors, events companies, any business where clients or the public visit your location | Consultants, architects, accountants, lawyers, IT professionals, engineers, healthcare providers |

What It Does NOT Cover | Professional mistakes, financial losses from advice, intentional acts, or employee disputes | Physical accidents at your premises, intentional fraud, contractual penalties, or bodily injury claims |

Typical UAE Annual Premium | AED 2,000–10,000+ depending on premises size, footfall, and industry | AED 3,000–20,000+ depending on profession, revenue, and coverage limit selected |

Common Policy Requirement | Free zone trade licenses, government tenders, construction NOCs from Dubai Municipality | DIFC and ADGM licensing conditions, corporate client contracts, professional body registrations |

Errors, Omissions, and Negligence: What Triggers a Claim

A client alleges your advice, report, or design caused them a financial loss, this is the core trigger

Covers legal defence costs even when the claim is unfounded, defending a baseless claim in the UAE can still cost AED 30,000–100,000+ in legal fees

Most professional indemnity policies in the UAE operate on a claims-made basis: the policy active when the claim is filed responds, not necessarily the policy active when the work was done, retroactive cover matters significantly

DIFC and ADGM-licensed firms are typically required by their regulators to carry minimum professional indemnity limits as a condition of their financial services license

Take a management consultant in Dubai who advises a client to restructure their supply chain. The client implements the advice, loses AED 2 million in disrupted contracts, and files a negligence claim. Professional liability insurance covers the legal defence and any settlement up to the policy limit, which for UAE professional indemnity policies commonly ranges from AED 500,000 to AED 5 million. Annual premiums run AED 3,000–20,000+ depending on profession and limit.

What Professional Liability Does NOT Cover

Intentional acts or deliberate fraud, no insurer covers knowingly wrongful conduct

Physical accidents at your premises, that's general liability territory, not professional indemnity

Contractual penalties or liquidated damages written into a client agreement, these are typically excluded

Bodily injury claims from clients visiting your office, this is the most common coverage gap for UAE service firms

Here's a real scenario: an accounting firm's client visits their office, trips on a loose cable, and breaks a wrist. The firm's professional indemnity policy will not respond. Their general liability policy will. That gap, missing one policy while holding the other, is the leading reason UAE SMEs end up underinsured. If you're also thinking about best health insurance for business owners in UAE, it's worth noting that employee health cover is a separate obligation entirely from commercial liability insurance.

The Core Difference Between General and Professional Liability Insurance

General liability insurance UAE covers physical and operational risks, injury, property damage, and advertising harm. Professional liability insurance covers financial losses from your professional advice or service errors. Most UAE businesses with both a physical presence and a service offering need both policies to avoid a dangerous coverage gap.

Which UAE Businesses Need Both Policies

Any business that has a physical location AND provides professional services or advice should carry both policies. One does not substitute for the other.

IT consultancies with a Dubai office: general liability for client visits, professional indemnity for system recommendations

Legal firms with client meeting rooms: general liability for the space, professional indemnity for legal advice

Engineering companies with site operations: general liability for site accidents, professional indemnity for design specifications

Free zone businesses bidding on government or corporate contracts are increasingly required to produce certificates of both general and professional liability coverage as part of the RFP process

A cybersecurity consultancy at Dubai South Free Zone hosts client briefings onsite and delivers security audits remotely. They need general liability insurance UAE coverage for the physical space and professional liability for the audit recommendations. An architecture firm in Abu Dhabi faces the same split: general liability for client site visits to their studio, professional indemnity for design errors in their drawings. One policy alone leaves them half-exposed. Some UAE insurers bundle both into a Business Owner Policy (BOP) at a combined premium, which can reduce total cost by 10–20% versus buying separately. For businesses considering ISO certification in UAE, note that ISO 9001 compliance audits often prompt a simultaneous insurance review, the two processes complement each other well.

How to Choose the Right Business Insurance UAE Policy for Your Company

To choose the right business insurance UAE policy, first identify whether your risk is physical, injuries, property damage, or advice-based, errors, omissions. Then assess your contractual obligations, client-facing activities, and UAE regulatory requirements. Most service businesses need both general and professional liability coverage to be fully protected.

Step 1: Map Your Risk Profile Before Talking to a Broker

List every way your business interacts with the public, clients, or third parties: physical visits, remote advice, events, deliverables

Identify contractual insurance obligations in your client agreements or free zone license conditions

Assess the financial consequence of a worst-case claim in each risk category, this determines the coverage limits you need

Check whether your UAE free zone authority, such as Dubai South, specifies minimum insurance requirements as part of your license conditions

A Dubai-based HR consultancy running through this exercise identifies three distinct risk layers: clients visit the office (general liability insurance UAE coverage needed), the firm provides recruitment advice (professional liability needed), and it processes employee data (cyber liability worth considering). Coverage limits for UAE SMEs typically start at AED 1 million per occurrence for general liability and AED 500,000 for professional indemnity, both are reasonable starting points before you assess your specific exposure.

Step 2: Understand D&O and Cyber Liability as Additional Layers

Directors and Officers (D&O) insurance covers company directors against claims of wrongful acts, mismanagement, or breach of fiduciary duty, relevant for UAE companies with boards or investor relationships. D&O premiums typically start at AED 5,000/year for SMEs

Cyber liability insurance covers data breach response costs, regulatory fines, and third-party claims following a cybersecurity incident, increasingly required for UAE businesses handling personal data under the Federal Decree-Law No. 45 of 2021 (UAE Personal Data Protection Law, PDPL)

Neither D&O nor cyber liability substitutes for general or professional liability, they address completely distinct risk categories

A fintech startup at a UAE free zone carries general liability for its office, professional indemnity for its financial advice, and cyber liability for its customer data platform. Three distinct policies. Three distinct risk categories. None of them overlaps. Worth flagging: UAE cybercrime-related losses have grown substantially in recent years, making cyber liability one of the fastest-growing commercial insurance lines in the region.

Step 3: Get Comparable Quotes and Check Policy Exclusions

Compare at least three quotes from UAE-licensed insurers, premium differences of 30–40% for identical coverage are common in the UAE commercial insurance market

Read the exclusions section before you focus on price, a cheap policy with broad exclusions is not cheaper when a claim arrives

Confirm retroactive dates on professional liability policies, gaps in continuous coverage can void claims for work done before the current policy period

Two UAE insurers quote AED 4,000 and AED 6,500 for the same professional indemnity limit. The cheaper policy excludes contractual liability claims, a common source of disputes in UAE service contracts. The AED 6,500 policy is the better value. DSBH business support services can connect you with vetted insurance advisers who already understand free zone license requirements, which saves significant time at this stage.

Is general liability insurance mandatory for UAE businesses?

There is no single federal law requiring general liability insurance for all UAE businesses. However, specific sectors, construction, healthcare, events, face regulatory mandates, and many free zones require proof of coverage before issuing or renewing a trade license. Dubai Municipality, for example, requires contractors to carry valid public liability insurance before issuing a No Objection Certificate (NOC) on permitted projects. Practically speaking, operating without coverage is a significant financial risk regardless of whether it is legally mandated in your specific case.

Typical Costs of General Liability Insurance UAE and Professional Liability in 2026

General liability insurance UAE typically costs AED 2,000–10,000+ per year for SMEs, depending on premises size, footfall, and industry. Professional liability insurance Dubai ranges from AED 3,000–20,000+ annually based on profession, revenue, and coverage limit. Bundling both policies with one insurer often reduces total premiums by 10–20%.

What Drives Premium Costs Up or Down in the UAE

Business size and annual revenue: insurers use turnover as a proxy for exposure, higher revenue typically means higher premiums

Industry risk profile: construction and events carry higher general liability premiums than office-based businesses

Professional risk category: medical professionals and lawyers pay more for professional indemnity than marketing consultants

Claims history: a clean record over three or more years can reduce UAE commercial insurance premiums by 15–25%

Coverage limit selected: doubling the limit does not double the premium, the marginal cost of higher limits decreases as you go up

Here's a practical illustration. A small marketing consultancy with AED 500,000 annual revenue might pay AED 2,500/year for general liability and AED 4,000/year for professional indemnity. A mid-size engineering firm with AED 5 million revenue and active site operations could pay AED 8,000 and AED 15,000 respectively. The difference isn't arbitrary, it reflects the insurer's assessment of how often and how severely claims occur in each category. For broader financial planning, the cost of running a business in Dubai guide puts these insurance figures in context alongside licensing, staffing, and office costs.