IT Companies in Dubai vs Emerging Tech Startups: Trends and Opportunities

Topic Summary

Dubai's technology market splits between established IT companies, integrators, government suppliers and telco IT arms, and a fast-moving startup ecosystem reshaping the sector. This guide explains how the market is structured, where startup activity and funding concentrate, and where the real opportunity lies for new entrants.

By Editorial Team, Business setup specialists covering UAE free zones, technology sector formation, and GCC market entry since 2015. Full bio →

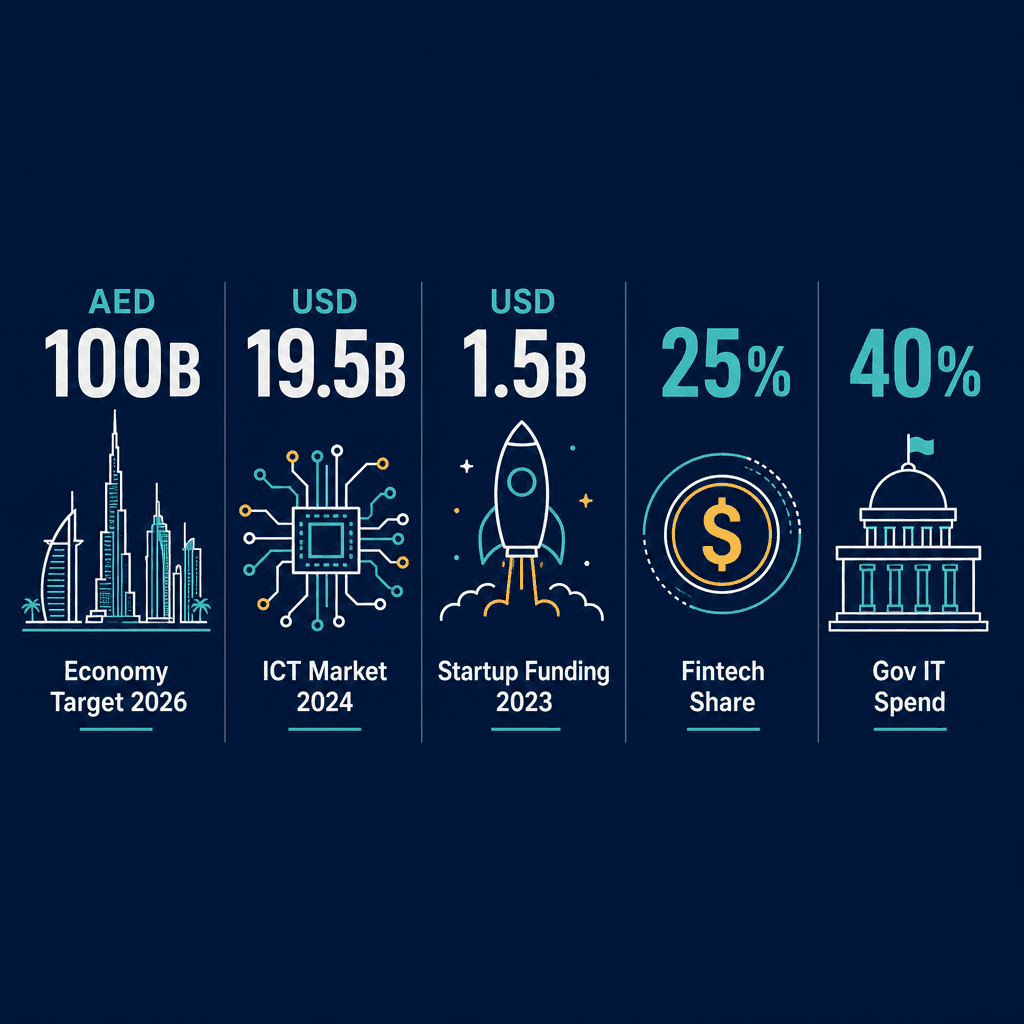

The UAE's technology sector is projected to contribute over AED 100 billion to the national economy by 2026 (UAE Ministry of Economy, 2023). Dubai accounts for the majority of that output. The UAE ICT market was estimated at USD 19.5 billion in 2024 (IDC, 2024). UAE startups raised over USD 1.5 billion in venture funding in 2023 (MAGNiTT, 2024). Fintech alone accounts for roughly 25% of all UAE startup funding rounds (MAGNiTT, 2024). Government IT spending is expected to reach USD 4.5 billion by 2026 (Gartner, 2024). And the UAE ranked first in MENA for startup ecosystem maturity in 2023 (Global Startup Ecosystem Report, 2023).

Dubai's technology market is bifurcating. On one side are established IT services companies, system integrators, managed service providers, and enterprise software resellers that have dominated contracts for decades. On the other are a new generation of tech startups building SaaS, fintech, healthtech, and AI-native products that are reshaping their own categories. This guide unpacks both sides, maps where IT companies Dubai trends are heading, and shows you exactly where the opportunity sits, whether you're a global IT firm eyeing the Gulf or a founder ready to build.

What Are IT Companies in Dubai and How the Market Is Structured Today

IT companies in Dubai range from large government IT suppliers and telco-owned technology arms to enterprise system integrators and managed service providers. These established players dominate long-cycle government contracts and direct enterprise sales, operating across banking, healthcare, logistics, and public administration under both UAE free zone and mainland structures. Understanding IT companies Dubai trends starts with understanding who already owns the market.

The Established Players: Government Suppliers, Integrators, and Telco IT Arms

Three categories define the IT industry UAE incumbents:

Government IT suppliers: G42 (Abu Dhabi-headquartered, valued at over USD 1.5 billion) and DarkMatter, both holding AI and cybersecurity contracts at the federal level

Enterprise system integrators: Regional arms of Cognizant, Wipro, and IBM, each running delivery centers across Dubai's major business districts

Telco IT arms: e& Enterprise (formerly Etisalat Digital) and du, which bundle infrastructure, cloud, and managed services into multi-year government and semi-government contracts

e& Enterprise is a textbook example of how this model works. It holds infrastructure contracts spanning federal ministries, smart city deployments, and enterprise cloud migration, combining telco assets with IT services to lock in multi-year revenue. Government and semi-government contracts account for approximately 40% of IT spend in the UAE (IDC, 2024). Margins are thin, but contract volumes are substantial and renewal rates are high.

How Established IT Companies Go to Market in Dubai

The dominant go-to-market route is the government RFP/tender cycle, which typically runs 12 to 18 months from brief to contract award. Direct enterprise sales follow a relationship-driven model, account managers with 10-plus years of in-market relationships, often supported by local sponsor arrangements or partner entities under mainland DED licenses.

Channel partner programs are the other major route. SAP's UAE partner ecosystem includes over 40 certified resellers and integrators operating from Dubai free zones, handling ERP implementations for government entities and large enterprises. Microsoft, Oracle, and Cisco operate similar tiered partner models. Worth flagging: free zone-licensed IT companies need a mainland branch or agent to participate directly in federal government procurement, a structural constraint that shapes how established players set up their legal entities. If you're exploring this route, a professional business license in Dubai is often the starting point for IT services firms.

The Emerging Tech Startup Ecosystem Reshaping the Technology Sector Dubai

Dubai's emerging tech startup ecosystem is concentrated in fintech, healthtech, logistics tech, edtech, proptech, and AI. Key accelerators include DIFC FinTech Hive, Hub71 in Abu Dhabi, and in5 Tech. UAE startups raised over USD 1.5 billion in venture funding in 2023, with Dubai accounting for the majority of deals (MAGNiTT, 2024). Tech startups Dubai are no longer a sideshow, they're the primary growth engine of emerging tech Dubai.

Sectors Attracting the Most UAE Tech Startup Activity

The most active verticals for tech startups Dubai right now:

Fintech: Payments, lending, Islamic fintech, and crypto, Sarwa, Beehive, and YAP are live examples of UAE-built products with regional scale

Healthtech: Post-pandemic acceleration in telemedicine, AI diagnostics, and insurance tech; MENA healthtech startups raised USD 200M+ in 2023 (MAGNiTT, 2023)

Logistics tech: Proximity to Jebel Ali port and Al Maktoum cargo hub creates natural demand for supply chain SaaS and freight visibility tools

Proptech: Huspy and Property Monitor are building digital infrastructure for one of the world's most active real estate markets

AI-native products: Generative AI tools built specifically for Arabic language and MENA market contexts, an underserved gap that global models haven't filled

Beehive is worth studying closely. The UAE's first regulated peer-to-peer lending platform launched from Dubai and has facilitated over AED 1 billion in business financing. That's a product doing what legacy banks couldn't move fast enough to build. If you're considering how to start a fintech company in Dubai, Beehive's trajectory is the clearest proof of market.

Accelerators, Incubators, and the Funding Landscape for Emerging Tech Dubai

The accelerator infrastructure supporting emerging tech Dubai is genuinely strong:

DIFC FinTech Hive: The region's largest fintech accelerator, backed by DIFC Authority, regulatory sandbox access and direct introductions to 44+ financial institutions; has supported 200+ startups since 2017

Hub71 (Abu Dhabi): Government-backed, offering equity-free incentive packages up to AED 500,000 for qualifying startups

in5 Tech (Dubai): Free zone-embedded incubator with low-cost desk space, mentorship, and fast-track licensing

Dubai South Business Hub: A free zone actively courting tech businesses with competitive license packages and world-class logistics infrastructure at the heart of the Al Maktoum International Airport corridor

DIFC FinTech Hive's 2023 cohort included 44 startups from 20 countries, connecting them directly to 17 financial institutions operating within DIFC. That's a go-to-market shortcut no standalone accelerator in the region can replicate. The UAE led MENA in startup deal count for the third consecutive year in 2023 (MAGNiTT, 2024), which tells you the capital is here, the question is which structure and free zone positions you best to access it.

Where the Real Opportunity Lies for New Entrants in the IT Industry UAE

The biggest opportunity in Dubai's IT market sits in the gap between what legacy IT companies deliver and what modern businesses actually need: cloud-native architecture, API-first integrations, mobile-first design, and AI-ready platforms. Government digital transformation under Smart Dubai and the UAE Digital Economy Strategy 2031 is creating a procurement window that newer vendors are well-positioned to win. This is the clearest near-term opportunity in the IT industry UAE.

Government Digital Transformation as a Client: The Smart Dubai Opportunity

Smart Dubai has digitized over 1,000 government services (Smart Dubai, 2023), and the initiative targets 100% digital government services across all touchpoints. The UAE Digital Economy Strategy 2031 aims to double the digital economy's contribution to GDP, a policy commitment that translates directly into sustained procurement budgets for cloud migration, UX redesign, and AI integration.

Dubai's Roads and Transport Authority (RTA) has issued multiple open innovation challenges for mobility tech startups, resulting in paid pilots. That's a procurement model that bypasses traditional 18-month RFP cycles entirely. New vendors can access these opportunities through GITEX-sourced introductions, government innovation challenges, and accelerator programs tied to specific ministries. The procurement gap is real: government entities increasingly want outcome-based contracts, not body-shop IT delivery, a structural shift that favors product companies over traditional integrators. To start your IT tech company in Dubai free zone, understanding this procurement shift is essential.

The Gap Between Legacy IT Delivery and What Modern Businesses Need

Here's the thing: legacy IT companies are strong on infrastructure and on-premise deployment, but slow to deliver cloud-native, API-first solutions. SMEs and scale-ups in Dubai increasingly want SaaS subscriptions, not CapEx-heavy custom builds. Consider a UAE logistics company choosing between a legacy ERP integration (12-month deployment, AED 500,000+) and a modern API-first TMS SaaS (live in 6 weeks, subscription pricing). The latter wins more often than incumbents want to admit.

Mobile-first and Arabic-language UX is deeply underserved, most global SaaS products aren't built for the MENA market context. And AI integration is still treated as an add-on in most enterprise IT contracts, not a core architecture decision. Startups building AI-native from day one have a structural edge that's hard for legacy integrators to replicate without rebuilding their delivery model from scratch. The API economy in MENA is projected at USD 3.2 billion by 2027 (IDC, 2024), that's the market these startups are building into.

Established IT Companies vs Tech Startups in Dubai: Head-to-Head Comparison

Feature | Established IT Companies | Tech Startups Dubai |

|---|---|---|

Revenue Model | Project-based or managed service retainer; high volume, thin margins | SaaS subscriptions or transaction fees; lower volume, higher margin potential |

Typical Sales Cycle | 12–18 months via government RFP/tender | 2–8 weeks via direct product trial or accelerator introductions |

Primary Client Type | Federal/emirate government, semi-government entities, large enterprises | SMEs, scale-ups, and digital-native enterprise buyers |

Product vs Services | Custom services delivery; limited IP ownership | Proprietary software product; scalable without linear headcount growth |

Funding Source | Contract revenue; bank credit facilities | Venture capital, angel rounds, government grants (Hub71, in5) |

Free Zone vs Mainland | Often mainland DED license for direct government contract eligibility | Free zone setup at Dubai South Business Hub for cost, speed, and regulatory access |

Talent Strategy | Large teams; sourced via offshore delivery centers in India, Pakistan | Lean core team; ESOP/equity to attract senior engineers; hybrid and remote-friendly |

Established IT Companies vs Tech Startups in Dubai: A Direct Comparison

Established IT companies in Dubai compete on relationships, compliance track records, and large-scale delivery capacity. Tech startups compete on speed, unit economics, and product innovation. The two models are increasingly converging as corporates acquire startups and startups land enterprise contracts, but the go-to-market strategies and cost structures remain fundamentally different.

Established IT Firms vs Dubai Tech Startups: Key Differences at a Glance

Neither model is inherently superior, market position and growth stage determine which approach is right. What's worth watching is the convergence happening at the edges. Corporate venture arms of telcos like e& Ventures are actively acquiring or partnering with startups. In 2022, e& acquired a majority stake in Careem's fintech and super-app infrastructure business, a local example of the same pattern Microsoft demonstrated globally with LinkedIn and Nuance.

This convergence means the boundary between "established IT company" and "tech startup" in Dubai is blurring faster than most observers expected. Incumbents are buying product capability. Startups are landing enterprise contracts. The IT companies Dubai trends point toward a hybrid middle ground where the winners combine startup-speed product development with enterprise-grade compliance and local relationships.

Key considerations before choosing your model:

If you're targeting government contracts, a mainland DED license or a free zone entity with a mainland branch is non-negotiable for direct federal procurement

If you're building a SaaS product for SMEs or regional scale-ups, a free zone structure gives you speed, cost efficiency, and 100% ownership

If you're a UK or US-based IT services firm entering Dubai, the relationship-driven sales model means you'll need at least 12 months of local presence before winning meaningful contracts

Corporate venture activity from e& and du signals that startups with proven product-market fit in fintech, logistics tech, or AI should consider strategic partnership conversations early

How to Choose the Right Free Zone for Your Tech Company in Dubai: Five Key Factors

Choosing the right free zone for a tech company in Dubai depends on five factors: the type of technology activity, proximity to clients, license cost, visa quota, and regulatory access. Dubai South Business Hub serves a broad range of tech business profiles, from logistics-tech startups to regulated fintech operators, combining competitive pricing with strategic infrastructure. This is one of the most consequential decisions in the technology sector Dubai setup process.

Step 1: Match Your Tech Activity to the Right Free Zone Profile

Each free zone in the emerging tech Dubai ecosystem has a distinct profile:

Dubai Internet City (DIC): Brand-prestige hub; Microsoft, Oracle, and Cisco are all based here, best for IT services companies wanting enterprise credibility and proximity to large corporate buyers

DIFC: Mandatory for regulated fintech, access to the DFSA regulatory sandbox and direct introductions to 44+ global financial institutions operating within the zone

DAFZA: Logistics-adjacent, strong for logistics tech, supply chain SaaS, and e-commerce technology companies; supports over 1,600 companies across aviation, logistics, and tech sectors

Dubai South Business Hub: Cost-competitive, connected to Al Maktoum International Airport and Jebel Ali, ideal for startups and scale-ups in logistics tech, AI, and IT services that need low overheads without sacrificing infrastructure access

A cybersecurity startup serving logistics clients would find Dubai South Business Hub a more cost-effective base than DIC, with direct proximity to the clients it needs to serve. That's the practical logic of matching free zone to business model. If you're exploring how to start a cyber security business in Dubai, the free zone decision shapes everything from your license type to your client access.

Step 2: Evaluate License Costs, Visa Allocations, and Activity Permits

Free zone IT licenses in Dubai range from AED 12,000 to AED 50,000+ depending on the zone and activity type. The license category matters: an IT professional license, a technology trading license, and a software development license are distinct permit types with different activity scopes. Getting this wrong at setup creates compliance headaches later.

Visa quota is a practical constraint that founders underestimate. Early-stage startups typically need 2 to 4 visas; scaling teams need 10 or more. A 3-person SaaS startup licensing at Dubai South Business Hub can secure a professional license, 3 visas, and a flexi-desk for significantly less than comparable setups at higher-cost free zones — meaningful at pre-revenue stage. One more thing to consider: if government contract eligibility matters to your growth plan, you'll need a mainland branch in addition to your free zone entity. Launch your tech company at Dubai South Business Hub Free Zone to explore the specific packages available.

Hiring Tech Talent in the UAE: What IT Companies and Startups Are Competing For

Tech talent in the UAE is concentrated across Dubai's established business and technology districts. The market is competitive: UAE-based tech roles compete directly with remote-first global companies offering dollar or euro salaries. Specialist skills in AI, cloud architecture, cybersecurity, and full-stack development command significant premiums in 2026. This is a core challenge for anyone building in the technology sector Dubai.

Where to Source Tech Talent in Dubai and the UAE

The UAE tech sector employs over 250,000 professionals (MOHRE, 2023), drawing from India, Pakistan, Egypt, Lebanon, Eastern Europe, and increasingly the Philippines and Nigeria. In practice, talent lives across the city and commutes or works hybrid, regardless of where a company is licensed. Average software engineer salaries in Dubai run AED 15,000 to AED 30,000 per month depending on specialization (Hays UAE Salary Guide, 2024).

Mohamed Bin Zayed University of AI (MBZUAI) in Abu Dhabi, launched in 2019 with zero tuition fees, graduated its first cohort of 100+ AI specialists in 2022. Dubai-based AI startups are actively recruiting from that pipeline. Heriot-Watt Dubai and Middlesex University Dubai supply solid software engineering graduates. The UAE's remote work visa also allows companies to engage global professionals legally — a useful mechanism for early-stage teams that can't yet justify full-time headcount.

Is it hard to compete with global remote roles for UAE tech talent?

Yes, and it's the most underestimated hiring challenge in the UAE. Remote roles paying USD salaries from US and European employers are the real competition, not local IT firms. UAE companies counter with tax-free income, family visa sponsorship, and lifestyle. ESOP frameworks recognized in DIFC and ADGM give startups a credible equity story. Careem attracted 1,000+ engineers before its Uber acquisition by combining competitive equity, a regional mission, and the Dubai lifestyle package, a template worth studying for any founder building a tech team here.

IT Companies in Dubai vs Emerging Tech Startups: What You Should

References

Editorial sources available on request. Full citation list is being compiled.