New UAE Tax Procedures 2026: What Businesses Need to Know In 2026, the UAE's tax compliance landscape looks fundamentally different from what businesses encountered when corporate tax first went live in June 2023, with t

New UAE Tax Procedures 2026: What Businesses Need to Know

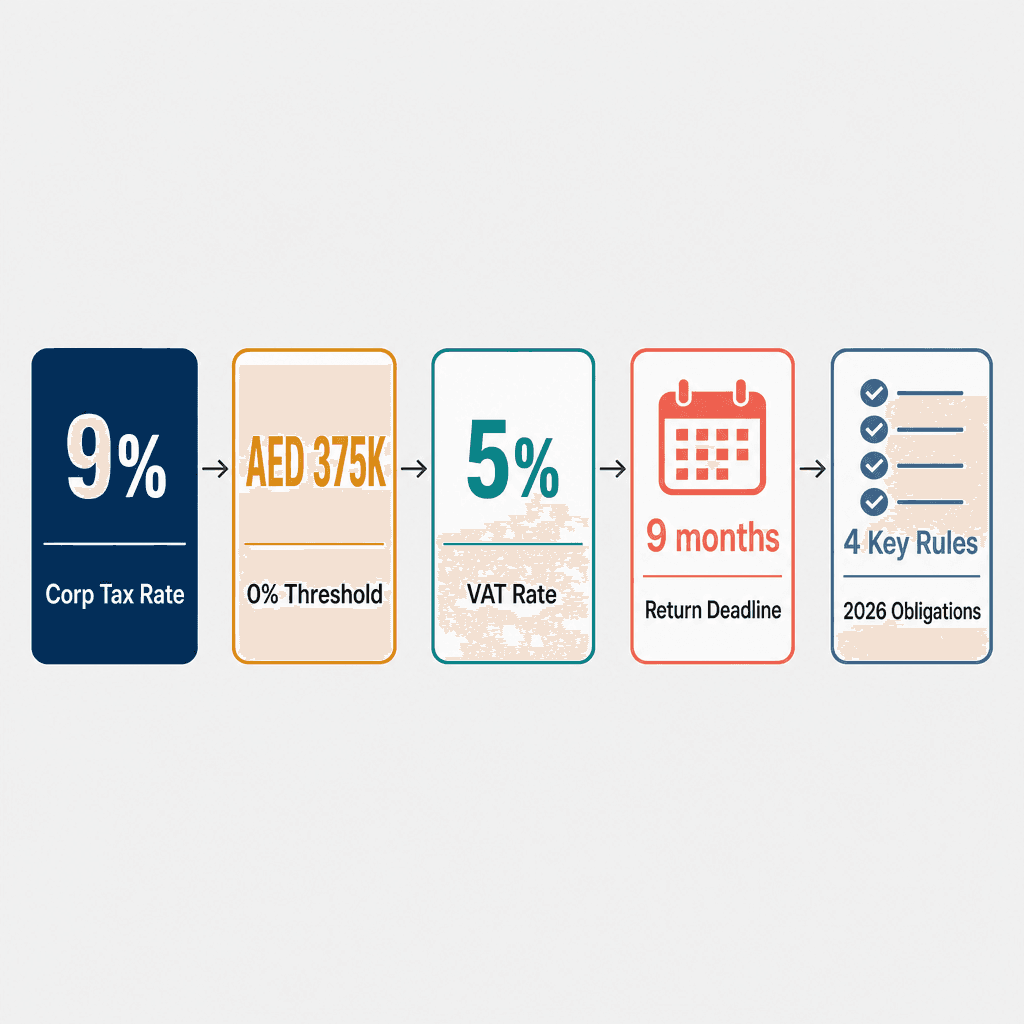

In 2026, the UAE's tax compliance landscape looks fundamentally different from what businesses encountered when corporate tax first went live in June 2023, with the 9% corporate tax rate applying to taxable income above AED 375,000 (Federal Decree-Law No. 47 of 2022), a 0% rate for income at or below that threshold, and VAT holding steady at 5% since Federal Decree-Law No. 8 of 2017. What's changed is the layer on top: transfer pricing documentation thresholds under Ministerial Decision No. 97 of 2023, Country-by-Country Reporting (CbCR) obligations for large multinationals, a phased e-invoicing mandate tied to the Peppol-based BTDT platform, and an FTA enforcement posture that has visibly shifted from education-first to active audit issuance. The new UAE tax procedures 2026 are not one change, they are a converging set of obligations landing in the same compliance window.

This guide walks you through every significant new UAE tax procedure and regulatory update relevant to businesses operating in the UAE in 2026, from corporate tax return deadlines and transfer pricing rules to e-invoicing timelines, free zone eligibility conditions, and penalty considerations. Where specific 2026 developments are based on announced timelines rather than confirmed legislation, we flag that clearly so you can verify with a registered tax agent.

What Are the New UAE Tax Procedures 2026 and Why They Matter for Your Business

The new UAE tax procedures 2026 refer to a cluster of regulatory updates, including corporate tax return filing deadlines, transfer pricing documentation, e-invoicing mandates, and updated free zone eligibility rules, that collectively raise the compliance bar for businesses operating in the UAE from 2024 financial years onward. These aren't isolated tweaks. They represent the maturation of a tax framework that launched in 2023 and is now entering its enforcement phase.

From Zero Tax to a Full Compliance Framework: The Journey Since 2023

The UAE introduced corporate tax at 9% for taxable income above AED 375,000, effective for financial years starting on or after 1 June 2023 (Federal Decree-Law No. 47 of 2022). The 0% rate for income at or below AED 375,000 remains in place, a genuine relief for smaller businesses and startups. But the 2023 launch was the foundation, not the finished building. The UAE corporate tax guide 2024 covers the base structure in detail; what 2025 and 2026 bring are layered obligations stacked on top of that base.

Consider a mainland trading company with a 31 December 2023 year-end. It filed its first corporate tax return in September 2024, a significant milestone. But in 2026, that same company now faces transfer pricing documentation requirements and potential FTA audit exposure as enforcement ramps up. Filing once was the easy part. Sustaining compliance year-on-year, with new obligations activating, is the real challenge.

Why 2026 Is the Defining Year for UAE Tax Compliance

The first full cohort of UAE businesses is now completing its second corporate tax return cycle. Lessons from year one, errors in income classification, missed elections, incomplete related-party disclosures, now feed directly into year two scrutiny. The uae tax changes 2026 aren't happening in isolation: transfer pricing documentation, CbCR notification, and e-invoicing phased mandates are all activating in the same window.

Corporate tax return filing for December 2025 year-ends: deadline 30 September 2026

Transfer pricing master file and local file: required on FTA request for entities above AED 40 million threshold

CbCR notification: due for UAE-headquartered MNE groups above AED 3.15 billion consolidated revenue

E-invoicing: phased BTDT platform integration, with large businesses already in scope

A multinational group with a UAE subsidiary generating over AED 200 million in revenue will simultaneously manage corporate tax filing, master file and local file preparation, and CbCR notification in the same 2026 compliance window. That's not a routine filing exercise, it requires a structured compliance calendar. See the company compliance calendar UAE for deadline tracking.

New UAE Tax Procedures 2026: Obligation Overview by Business Type

Obligation | SME / Mainland Entity | Free Zone / MNE Group |

|---|---|---|

Corporate Tax Return | ✅ Required, 9-month rule applies | ✅ Required, QFZP status affects rate |

Transfer Pricing Documentation | ❌ Below AED 40M threshold, not required | ✅ Required above AED 40M related-party transactions |

Country-by-Country Report | ❌ Not applicable | ✅ Required above AED 3.15B consolidated revenue |

E-Invoicing (BTDT Platform) | Phase 2+, timeline to be confirmed by FTA | Phase 1 if above revenue threshold |

Small Business Relief Election | ✅ Available below AED 3M taxable revenue | ❌ QFZP entities not eligible |

FTA Audit Risk Level | Medium, trading and retail sectors flagged | Higher, related-party transactions under scrutiny |

Corporate Tax Return Filing in 2026: Deadlines, First-Year Filers, and Common Pitfalls

Businesses with a 31 December 2023 financial year-end filed their first UAE corporate tax return by 30 September 2024. Those with a 31 December 2024 year-end faced a 30 September 2025 deadline. Now, businesses with a 31 December 2025 year-end are heading toward a 30 September 2026 deadline, the active window for the uae corporate tax updates 2026 cycle. Missing these deadlines triggers administrative penalties under the latest UAE tax rules for businesses, so precision on your specific deadline matters enormously.

Key Deadlines Every Business Must Track in 2025 and 2026

The nine-month rule is the foundation: your corporate tax return and payment are due nine months after the end of your relevant tax period. Here's how that maps to real dates:

31 December 2023 year-end: deadline was 30 September 2024 (first cohort, now past)

31 December 2024 year-end: deadline was 30 September 2025

31 December 2025 year-end: deadline is 30 September 2026, the primary active window

Non-calendar year-ends: staggered deadlines apply, a 31 March or 30 June year-end produces a different nine-month calculation

Here's a scenario worth flagging: a free zone company incorporated in Dubai South with a 31 March 2025 year-end has a corporate tax return deadline of 31 December 2025, not September 2026. Missing this because of an assumed calendar-year rule is one of the most common first-year filing errors. Don't assume your deadline matches your neighbour's. Administrative penalties for late filing run at AED 500 per month for the first 12 months, rising to AED 1,000 per month thereafter (verify current schedule with the FTA).

What First-Year Filers Got Wrong, and How to Avoid Repeating It

The most consistent errors from first-year corporate tax filings in the UAE centred on three areas:

Incorrect classification of exempt vs. taxable income, particularly free zone qualifying income mixed with mainland revenue

Failure to elect small business relief where eligible (taxable revenue below AED 3 million, per Ministerial Decision No. 73 of 2023, verify if updated for 2026)

Incomplete or inaccurate related-party transaction disclosure schedules, which now feed directly into transfer pricing scrutiny

Several mainland SMEs with mixed trading and consulting revenue incorrectly classified all revenue as qualifying income in their first return. If repeated in 2026, that error is likely to attract FTA attention given increased audit activity in the trading sector. Get professional support early, accounting and tax compliance at Dubai South covers exactly these scenarios.

A process timeline showing the nine-month filing rule applied across three consecutive December year-end cohorts from 2024 to 2026. UAE Corporate Tax Return Deadlines: 9-Month Rule 1 Dec 2023 Filed Sep 2024 2 Dec 2024 Filed Sep 2025 3 Dec 2025 Filed Sep 2026 ! Non-Dec YE Staggered deadline

UAE corporate tax return deadlines follow a nine-month rule from financial year-end. Source: Federal Decree-Law No. 47 of 2022; FTA guidance, 2023–2026.

How to Navigate Transfer Pricing and Country-by-Country Reporting in 2026: A Step-by-Step Overview

UAE businesses with related-party transactions above AED 40 million (or specific category thresholds) must maintain a master file and local file under the new UAE transfer pricing rules. Multinational groups with consolidated revenue above AED 3.15 billion must file a Country-by-Country Report. Both obligations are active components of the new UAE tax procedures 2026, and both are based on announced timelines, so verify current thresholds with a registered tax agent before your next filing window.

Step 1: Determine Whether Transfer Pricing Documentation Applies to You

The threshold triggers under Ministerial Decision No. 97 of 2023 are:

Aggregate related-party transactions exceeding AED 40 million in a tax period: full master file and local file required

Specific transaction category exceeding AED 4 million: category-level documentation required

Arm's length principle applies to all related-party transactions, regardless of whether you cross the documentation threshold

A UAE subsidiary of a European manufacturing group with AED 55 million in intercompany service fee payments to its parent company crosses the AED 40 million threshold and must maintain both a master file and a local file for its 2024 tax period. The master file covers group-level information; the local file covers entity-specific related-party transactions. Both must be available on FTA request, not necessarily filed proactively, but produced within a defined timeframe. UAE transfer pricing rules are aligned with OECD BEPS Action 13, so if your group already prepares BEPS-compliant documentation for other jurisdictions, the UAE requirements should slot in without a complete rebuild.

Step 2: Understand Country-by-Country Reporting Obligations

CbCR applies to UAE-headquartered multinational enterprise (MNE) groups with consolidated group revenue of AED 3.15 billion or more in the preceding year (Cabinet Decision No. 44 of 2020, verify if superseded). The filing deadline is 12 months after the end of the reporting fiscal year. Worth flagging: even if the UAE entity is not the ultimate parent, it may still need to notify the FTA of which entity will file the CbCR, the notification obligation and the filing obligation are separate.

A UAE-based holding company that is the ultimate parent of a group with operations in six countries and consolidated revenue of AED 4 billion must file its first CbCR with the FTA within 12 months of its financial year-end. Based on announced timelines, 2026 is the first active filing year for many such groups. CbCR data feeds into the OECD's automatic exchange of information framework, which means the data you submit to the FTA may be shared with tax authorities in every jurisdiction where your group operates.

Step 3: Build Your Transfer Pricing Compliance Calendar

The single most effective thing you can do for transfer pricing compliance is map all related-party transactions at the start of each financial year. Reconstructing transaction data at year-end is slower, more error-prone, and produces documentation that looks retrospective to an auditor. Benchmark studies (comparability analyses) must be current, stale benchmarks from 2022 or 2023 won't hold up under FTA scrutiny in a 2026 audit. Align TP documentation preparation with your corporate tax return filing timeline, since both are due within nine months of year-end.

A logistics company at Dubai South with intragroup management fees, intercompany loans, and shared service cost allocations should maintain three separate transaction analyses within its local file, each requiring its own benchmarking methodology. Penalties for failure to maintain TP documentation can reach AED 100,000 (verify current schedule with the FTA). For specialist support, DSBH banking and taxation services provides transfer pricing documentation assistance tailored to free zone and mainland entities.

UAE Tax Obligations 2026: Key Thresholds at a Glance

A visual summary of the numerical thresholds triggering major UAE tax compliance obligations in 2026, designed to help businesses quickly assess their exposure.

AED 375,000: corporate tax 0% threshold (income at or below this level)

AED 3 million: small business relief eligibility ceiling (taxable revenue)

AED 4 million: per-category transfer pricing documentation trigger

AED 40 million: aggregate related-party transaction threshold for full TP documentation

AED 5 million / 5% of revenue: QFZP de minimis non-qualifying income cap (lower of the two)

AED 3.15 billion: consolidated group revenue threshold for CbCR filing

Suggested alt text: A horizontal threshold chart showing six AED value thresholds that trigger escalating UAE tax compliance obligations in 2026, from AED 375,000 at the base to AED 3.15 billion at the top.

E-Invoicing Rollout and VAT Compliance Updates: What the Phased Timeline Means for You

The UAE is implementing a mandatory e-invoicing system in phases, starting with large businesses and progressively covering all VAT-registered entities. E-invoices must comply with the Peppol-based BTDT standard and integrate with the FTA's digital platform. Based on announced timelines, mandatory adoption for most businesses is expected to complete by 2026, but verify the current FTA phasing schedule with a registered tax agent, as specific go-live dates for each phase are subject to update.

How the UAE E-Invoicing Phased Rollout Works

UAE e-invoicing follows a Continuous Transaction Controls (CTC) model: invoices are transmitted to the FTA platform in near real-time, rather than submitted in batch at period-end. Phase 1 targets large VAT-registered businesses above a revenue threshold; Phase 2 and beyond progressively captures mid-market and smaller entities. The UAE joins the Peppol network, a global interoperability framework already used across Europe, Singapore, and Australia, which means businesses with international operations may already have relevant infrastructure in place.

A wholesale distribution company in Dubai South with annual VAT-taxable turnover above AED 150 million is likely in Phase 1 of the e-invoicing rollout. That means it needs ERP system integration with the FTA's BTDT platform before its mandatory activation date, not after. Integration typically takes three to six months end-to-end, so if you haven't started assessing your system readiness, the clock is already running.

E-Invoicing's Interaction with Your VAT Compliance Process

E-invoicing does not replace VAT return filing. It operates alongside the quarterly VAT return submission process, and data consistency between the two is non-negotiable. Invoice data transmitted to the FTA platform must reconcile with your VAT return figures; discrepancies will trigger automated flags. Credit notes, debit notes, and self-billed invoices all fall within the e-invoicing scope, not just standard tax invoices.

A professional services firm currently issuing PDF invoices via email needs to either upgrade its accounting software to an FTA-integrated solution or engage a certified e-invoicing service provider. The VAT standard rate remains 5% (Federal Decree-Law No. 8 of 2017), but the mechanism for reporting it is changing. Businesses using manual or semi-manual invoicing processes should treat the e-invoicing mandate as an urgent systems project, not a future compliance consideration. The accounting and tax compliance at Dubai South team can advise on FTA-compatible software options.

Is your business in Phase 1 of the UAE e-invoicing rollout?

If your annual VAT-taxable turnover exceeds AED 150 million, you are likely in scope for Phase 1 of the UAE's BTDT e-invoicing mandate. You'll need ERP integration with the FTA's Peppol-based platform before your activation date, a process that typically takes three to six months. Check the FTA's current phasing schedule and confirm your go-live date with a registered tax agent.

FTA Enforcement and Audit Activity in 2026: Who Is Under the Microscope

The FTA has significantly increased audit activity in 2025 and 2026, with particular focus on the real estate, hospitality, retail, and professional services sectors. Businesses with high volumes of related-party transactions, inconsistent VAT return histories, or recently registered corporate tax entities are seeing elevated scrutiny. The uae tax changes 2026 aren't just about new obligations, they're about the FTA actively checking whether existing obligations are being met correctly.

Which Sectors Are Seeing Increased FTA Scrutiny

Real estate: VAT treatment of commercial vs. residential supply continues to generate errors, particularly in mixed-use developments where input VAT apportionment methodology is disputed

Hospitality and F&B: VAT on service charges, staff discounts, and complimentary items remains a high-error area

Professional services: related-party service fee arrangements and transfer pricing compliance are now firmly on the FTA's radar

Retail and e-commerce: cross-border VAT obligations and place of supply rules are under active review

A UAE-based real estate developer selling a mixed-use tower with residential apartments (VAT-exempt supply) and retail units (standard-rated supply) must apportion input VAT using an agreed methodology. The FTA has flagged this calculation as frequently miscalculated in recent audit cycles. Getting it wrong doesn't just produce a VAT liability, it signals to the FTA that your broader compliance processes need scrutiny. See non-compliance risks and fines in UAE for a full breakdown of penalty exposure.

How to Prepare Your Business for an FTA Audit

Audit readiness isn't something you build in response to a notice. It's a standing operational state. Here's what a solid audit file looks like:

VAT returns for all periods, with supporting invoices and customs declarations

Intercompany agreements, signed and dated contemporaneously

Frequently Asked Questions

What are the new UAE tax procedures 2026?

The new UAE tax procedures 2026 are updated regulatory frameworks governing corporate tax compliance, filing requirements, and reporting obligations for businesses operating in mainland and free zones. These changes align the UAE with global tax transparency standards. Businesses should review their current compliance setup with a qualified UAE tax advisor immediately.