Topic Summary

UAE corporate tax operates on a two-tier structure, with a standard rate applying above the qualifying threshold and defined exemptions for certain entities. This complete guide explains the rates and scope, who is exempt, and the conditions free zone businesses must meet to access the qualifying regime.

By Editorial Team, Business setup and tax compliance specialists covering UAE free zones, mainland regulations, and federal tax obligations since 2017. Full bio →

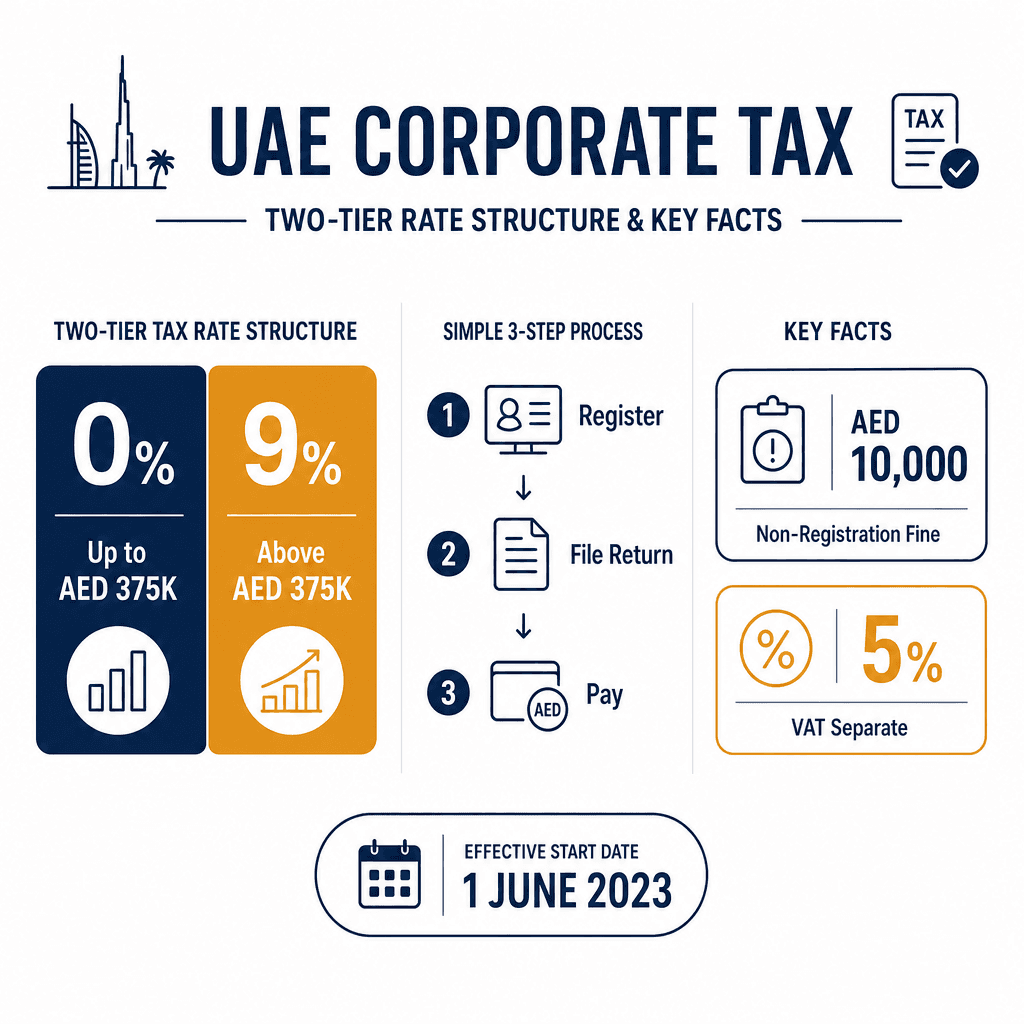

In 2026, every UAE-registered business, mainland or free zone, operates under a federal corporate tax regime that came into force on 1 June 2023, ending more than five decades of zero federal corporate tax for most commercial entities (UAE Ministry of Finance, 2023). The headline rate is 9%, but that single number doesn't tell the full story. The governing legislation, Federal Decree-Law No. 47 of 2022, introduced a two-tier structure: 0% on taxable income up to AED 375,000 [1] and 9% on profits above that threshold [2]. Free zone companies can still access a 0% rate on qualifying income, provided they meet substance and income conditions defined in Cabinet Decision No. 55 of 2023 [3]. Registration is mandatory for all UAE businesses, with a fixed AED 10,000 penalty for non-registration [4]. VAT at 5%, introduced in January 2018, runs as a completely separate obligation [5].

This guide covers UAE corporate tax explained in full: the rates that apply, who qualifies for exemptions, how free zone businesses can preserve the 0% rate, what counts as taxable income, when and how to file, and the concrete compliance steps every business owner needs to take today.

What Is UAE Corporate Tax Explained: Rates, Scope, and Effective Date

UAE corporate tax is a federal tax on business profits introduced on 1 June 2023 under Federal Decree-Law No. 47 of 2022. The standard rate is 9% on taxable income above AED 375,000. Income up to that threshold is taxed at 0%, giving small businesses meaningful relief. Free zone entities are subject to the same law but may qualify for a 0% rate on qualifying income, covered in detail in the free zone section below.

The Effective Date and Why It Changed Everything

Corporate tax applies to financial years starting on or after 1 June 2023. That means the effective date depends on your fiscal year, not a single calendar date. A company with a 1 January fiscal year became liable from 1 January 2024 and filed its first return in 2025. A company with a 1 June fiscal year became liable immediately from 1 June 2023.

The UAE had no federal corporate income tax for over 50 years. This marks a structural shift aligned with the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS), which the UAE joined as a committed member. The change signals the country's transition from a purely tax-free jurisdiction to one with a competitive but internationally credible tax framework (OECD, 2023).

To use a concrete example: a Dubai mainland trading company with a fiscal year running January to December became a corporate taxpayer from 1 January 2024, filing its first UAE corporate tax return in September 2025.

The Two-Tier Rate Structure: 0% and 9%

Here's how the rate structure actually works, and it's more favourable than most people initially assume:

0% rate: applies to taxable income from AED 0 to AED 375,000

9% rate: applies only to taxable income above AED 375,000, not to total income

15% rate: applies to large multinationals with consolidated global revenues above EUR 750 million, in line with Pillar Two of the OECD framework (OECD Pillar Two, 2023)

A consultancy earning AED 600,000 in taxable profit pays 0% on the first AED 375,000 and 9% on the remaining AED 225,000. Total tax: AED 20,250, not AED 54,000. That distinction matters enormously for small and mid-sized businesses planning their cash flow. For DSBH banking and taxation services, this rate structure is one of the first things we walk clients through, because the misconception that "9% applies to everything" causes unnecessary alarm.

Who Is Exempt from UAE Corporate Tax: Government, Extractors, and Public Benefit Entities

UAE corporate tax exemptions cover government entities and government-controlled entities, businesses extracting UAE natural resources (taxed separately at emirate level), qualifying public benefit entities, qualifying investment funds, and pension or social security funds. These entities must still register with the FTA unless a specific exclusion applies. Worth flagging: free zone entities are not in this exemption category, their 0% rate is a preferential rate, not an exemption from the law itself.

Government Entities and Natural Resource Extractors

Federal and emirate government bodies are automatically exempt under Federal Decree-Law No. 47 of 2022. This covers wholly government-owned entities engaged in sovereign functions. But government-controlled entities that conduct commercial activities, think government-linked companies operating in retail or hospitality, may still be subject to corporate tax unless they obtain a specific exemption decision from the Cabinet.

Businesses extracting UAE natural resources (oil, gas, minerals) remain subject to existing emirate-level taxation and are carved out of the federal corporate tax net entirely. Abu Dhabi National Oil Company (ADNOC) subsidiaries engaged in upstream extraction, for instance, fall under emirate-level fiscal arrangements, not the 9% federal rate. This carve-out preserves the existing fiscal framework that has governed the hydrocarbon sector for decades.

Qualifying Public Benefit Entities and Investment Funds

Charities and non-profits: exemption is not automatic. The entity must be listed in a Cabinet Decision to qualify. A UAE-registered charitable foundation providing educational grants, for example, must apply for public benefit entity status and be formally listed before its income is exempt.

Qualifying investment funds: REITs and other funds structured correctly can be exempt to prevent double taxation at both fund and investor level. The structure must meet conditions set by the FTA.

Pension and social security funds: funds established for the benefit of employees are exempt, provided they meet the definitional requirements under the law.

The practical takeaway from this section of the non-compliance risks and fines in UAE landscape: assuming your entity is exempt without formal confirmation is one of the most common and costly mistakes we see. Verify your status with the FTA before skipping registration (UAE Ministry of Finance, 2023).

Free Zone Businesses and the 0% Corporate Tax Rate: What the Conditions Actually Require

Free zone companies can retain a 0% corporate tax rate on qualifying income if they meet three conditions: they earn qualifying income as defined by Cabinet Decision, they maintain adequate substance in their free zone, and they pass the de minimis test on non-qualifying revenue. Failure on any single condition triggers the standard 9% rate, not just on the non-qualifying portion, but potentially across the entity's entire taxable income for that year.

What Counts as Qualifying Income for Free Zone Entities

Qualifying income is defined specifically in Ministerial Decision No. 139 of 2023. It's not a catch-all for any income earned by a free zone company. The categories that qualify include:

Income from transactions with other Qualifying Free Zone Persons

Income from qualifying intellectual property assets

Income from qualifying activities, manufacturing, fund management, ship operations, reinsurance, and holding company functions are included; the list is bounded and specific

Income from transactions with non-free zone persons that relate to qualifying activities (subject to conditions)

Income from mainland UAE customers is generally non-qualifying and taxed at 9%. A Dubai South logistics company earning freight income from non-free zone UAE clients cannot treat that revenue as qualifying income. Non-qualifying revenue must also stay below the de minimis threshold, the lower of AED 5 million or 5% of total revenue. Exceed that, and the entire entity loses Qualifying Free Zone Person status for that tax period.

For a detailed breakdown of income categories, see our dedicated article on understanding qualifying income for UAE corporate tax.

Substance Requirements and the Nexus Test

Adequate substance is the condition most businesses underestimate. A Qualifying Free Zone Person must conduct core income-generating activities inside the free zone, not merely hold a license while operating from a mainland office. The FTA assesses substance per financial year, and documentation is essential if you're ever audited.

A DMCC-licensed trading company that warehouses goods in a mainland facility and conducts all sales negotiations from a mainland office risks failing the substance test entirely, exposing its income to the 9% rate. The nexus test for IP income adds another layer: the IP must have been developed, at least partly, through qualifying R&D expenditure by the entity itself.

In practice, not all free zones are equal, and a business's operational profile directly affects how readily it can satisfy substance requirements. Dubai South's integrated logistics infrastructure, combining free zone licensing, warehousing, and physical operations in one location, makes it structurally easier to demonstrate genuine operational substance than setups where core activities are dispersed across multiple sites. For compliance support, accounting and tax compliance at Dubai South is worth exploring (Cabinet Decision No. 55 of 2023).

What Counts as Taxable Income Under UAE Corporate Tax

Taxable income under UAE corporate tax is the accounting net profit of a business, adjusted for specific items under the Corporate Tax Law. Adjustments include adding back non-deductible expenses, applying transfer pricing rules for related-party transactions, and excluding exempt income such as dividends from qualifying shareholdings. Understanding how does corporate tax work UAE means understanding these adjustments, the starting point is your audited accounts, not a separate tax calculation from scratch.

Starting Point: Accounting Profit and the Key Adjustments

Starting figure: net profit per financial statements prepared under IFRS or IFRS for SMEs

Non-deductible items to add back: regulatory fines and penalties, personal expenditure, 50% of entertainment expenses, and interest above the general interest deduction limitation rule

Exempt income to remove: dividends from UAE resident companies and capital gains from qualifying shareholdings (5%+ stake held for at least 12 months) are excluded under the participation exemption

A Dubai mainland company that paid AED 80,000 in regulatory fines during the year must add that full amount back to its accounting profit before calculating taxable income. That's a direct, unavoidable uplift to the tax base, and a reason why compliance with regulatory requirements has a direct financial cost beyond the fines themselves.

Transfer Pricing and Related-Party Transactions

Transactions between related parties must be priced at arm's length, the same price an independent party would charge in comparable circumstances. UAE transfer pricing rules follow OECD guidelines, and businesses with related-party transactions above thresholds set by Ministerial Decision must maintain both a master file and a local file.

A UAE holding company charging its subsidiary a AED 2 million annual management fee must be able to demonstrate that fee reflects genuine services at market rates. If it can't, the FTA can adjust taxable income upward, potentially triggering additional tax and penalties. Intra-group service charges, management fees, and intercompany loans are all subject to this scrutiny.

For free zone entities, this is especially critical. An intercompany transaction between a free zone entity and a related mainland entity can reclassify income as non-qualifying, triggering the 9% rate on what was previously treated as a 0% income stream. The DSBH banking and taxation services team regularly reviews these structures for clients before year-end (OECD Transfer Pricing Guidelines, 2022).

UAE Corporate Tax vs VAT: Understanding the Relationship Between the Two

UAE corporate tax and VAT are separate obligations with different triggers. VAT at 5% applies to taxable supplies of goods and services above AED 375,000 in annual turnover. Corporate tax applies to business profits. A business can owe both, either, or neither, registration thresholds, filing cycles, and compliance rules are entirely independent. UAE CT explained simply: corporate tax is on what you earn; VAT is on what you sell.

Key Differences Every Business Owner Must Know

UAE Corporate Tax vs VAT: Key Differences Every Business Owner Must Know

Feature | Corporate Tax | VAT |

|---|---|---|

Tax type | Direct tax on business profits | Indirect consumption tax on sales |

Rate | 0% (up to AED 375,000) / 9% (above) | 5% flat rate on taxable supplies |

What it applies to | Net taxable profit of the business | Value of goods and services supplied |

Registration threshold | Mandatory for ALL UAE businesses, no revenue minimum | AED 375,000 in annual taxable supplies |

Who bears the cost | The business, reduces net earnings directly | The end consumer, business collects and remits |

Filing frequency | Annual, 9 months after financial year end | Quarterly or monthly (FTA-assigned) |

Governing body | Federal Tax Authority (FTA) | Federal Tax Authority (FTA) |

Here's a scenario that catches many founders off guard: a startup generating AED 200,000 in revenue in its first year is below the mandatory VAT registration threshold. But it must still register for corporate tax and file a return, even if its taxable income is zero. Registration is not optional, and the AED 10,000 penalty for missing it applies regardless of profitability.

VAT is a pass-through cost if you're claiming input tax credits correctly. Corporate tax is a real cost to your bottom line. Both are administered by the Federal Tax Authority (FTA) through the EmaraTax portal, but the compliance calendars don't align, you need separate tracking systems for each. See our UAE VAT registration guide for the full VAT setup process (Federal Tax Authority UAE, 2024).

Does corporate tax apply if my business made a loss?

Yes, you must still register and file a corporate tax return even if your business recorded a loss. There's no tax to pay on a loss, but the filing obligation exists. The loss can be carried forward to offset future taxable income, subject to conditions under the Corporate Tax Law (Federal Decree-Law No. 47 of 2022).

Who Must Register for UAE Corporate Tax, and the Penalties If You Don't

Every UAE business, mainland and free zone, must register for corporate tax with the FTA, even if exempt or loss-making. Registration deadlines vary by license issuance date. Failure to register carries an AED 10,000 penalty. Late filing and late payment attract additional fines that compound over time. Corporate tax for businesses in Dubai and across the UAE is not a voluntary system, the obligation is universal.

Registration Deadlines and How They Are Calculated

Existing businesses (licensed before 1 March 2024): deadlines were staggered by license issuance month across 2023–2024 under an FTA schedule

New incorporations (after 1 March 2024): must register within three months of incorporation date

Natural persons (sole proprietors): must register if annual business turnover exceeds AED 1 million

Registration platform: FTA's EmaraTax portal, no fee for registration itself

A free zone company licensed in May 2023 had a registration deadline of 31 May 2024 under the FTA's staggered schedule. Missing that date triggered an immediate AED 10,000 penalty, fixed, with no standard waiver mechanism. You'll need your trade license, Emirates ID of the authorised signatory, and financial year details to complete registration on EmaraTax (Federal Tax Authority UAE, 2024).

Filing Deadlines, Late Payment Penalties, and What Happens Next

Filing deadline: nine months after the end of the financial year, a 31 December year-end means a 30 September deadline

Payment deadline: same date as filing, there's no separate payment window

Late filing penalty: AED 1,000 per month for the first 12 months, AED 2,000 per month thereafter

Late payment penalty: 14% per annum on unpaid tax, charged monthly

A company with a 31 December 2024 year-end that files its return on 1 December 2025, just one month late, immediately incurs a AED 1,000 penalty, plus monthly charges if tax remains unpaid. These penalties compound. A business that's both late filing and late paying can accumulate significant liabilities in a short period. For a full picture of the penalty framework, see our guide to non-compliance risks and fines in UAE (FTA Administrative Penalties, 2023).

Step-by-Step: What Your Business Needs to Do Right Now to Stay Compliant with UAE Corporate Tax

UAE corporate tax compliance requires six core actions: confirm your tax period, register on EmaraTax, assess your free zone qualifying income status, set up IFRS-compliant accounting, review related-party transactions for transfer pricing, and file your return with payment by the nine-month deadline. Start with registration, penalties begin there. Here's how to work through it systematically.

Step 1: Confirm Your Tax Period and Register on EmaraTax

Identify your financial year start date. This determines when your first corporate tax period began and when your first return is due. A 1 January start means your first return covers January–December 2024, due by 30 September 2025.

Log in to EmaraTax. The FTA's single digital portal handles all tax registrations. You'll need your trade license, Emirates ID of the authorised signatory, and your financial year details.

If you've missed your deadline, act immediately. The AED 10,000 penalty is fixed in most cases, but further delay compounds your exposure. Engage a tax adviser and register the same day.

A UK-based founder who set up a Dubai South free zone company in late 2023 and assumed registration could wait until the first return was due missed the staggered deadline and incurred the AED 10,000 penalty before filing a single return. The registration step is separate from the filing step, and it comes first. EmaraTax registration is free; the penalty for skipping it is not (Federal Tax Authority UAE, 2024).

Step 2: Assess Free Zone Status, Set Up Accounting, and File on Time

Free zone businesses: document your qualifying income streams and substance position before year-end. Retroactive documentation is significantly weaker in an FTA audit than contemporaneous records.

Set up IFRS-compliant accounting. Financial statements must be prepared under IFRS or IFRS for SMEs. Cash-basis accounting is not acceptable for corporate tax purposes under Federal Decree-Law No. 47 of 2022.

Review related-party transactions. Confirm arm's length pricing is documented for all intra-group charges, loans, and service fees before closing your books.

File and pay by the nine-month deadline. Calendar year businesses: 30 September is your annual deadline. Don't treat it as a soft date.

A Dubai South free zone logistics company should document its qualifying activities, substance headcount, and revenue split between free zone and non-free zone clients before closing its books, not after receiving an FTA query. Dubai South's integrated infrastructure makes genuine substance demonstrably easier to evidence than a letterbox operation elsewhere. For hands-on support, accounting and tax compliance at Dubai South and DSBH banking and taxation services can help you build the compliance infrastructure before your next filing deadline.

UAE Corporate Tax Compliance Timeline: From Registration to Filing

A visual process map showing the six compliance steps every UAE business must complete, with deadlines and penalty triggers at each stage.

Step 1: Identify financial year start date (determines first tax period)

Step 2: Register on EmaraTax, deadline tied to license month; AED 10,000 penalty for non-registration

Step 3: Assess qualifying income and substance (free zone businesses only)

Step 4: Prepare IFRS-compliant financial statements

Step 5: Review and document all related-party transactions at arm's length

Step 6: File return and pay tax

References

[1] Source pending — please add URL and publisher.

[2] Source pending — please add URL and publisher.

[3] Source pending — please add URL and publisher.

[4] Source pending — please add URL and publisher.

[5] Source pending — please add URL and publisher.