Topic Summary

By Editorial Team , UAE business setup and tax compliance specialists with direct experience filing VAT refund claims through the FTA EmaraTax portal. Full bio →

Last updated: June 2026

By Editorial Team, UAE business setup and tax compliance specialists with direct experience filing VAT refund claims through the FTA EmaraTax portal. Full bio →

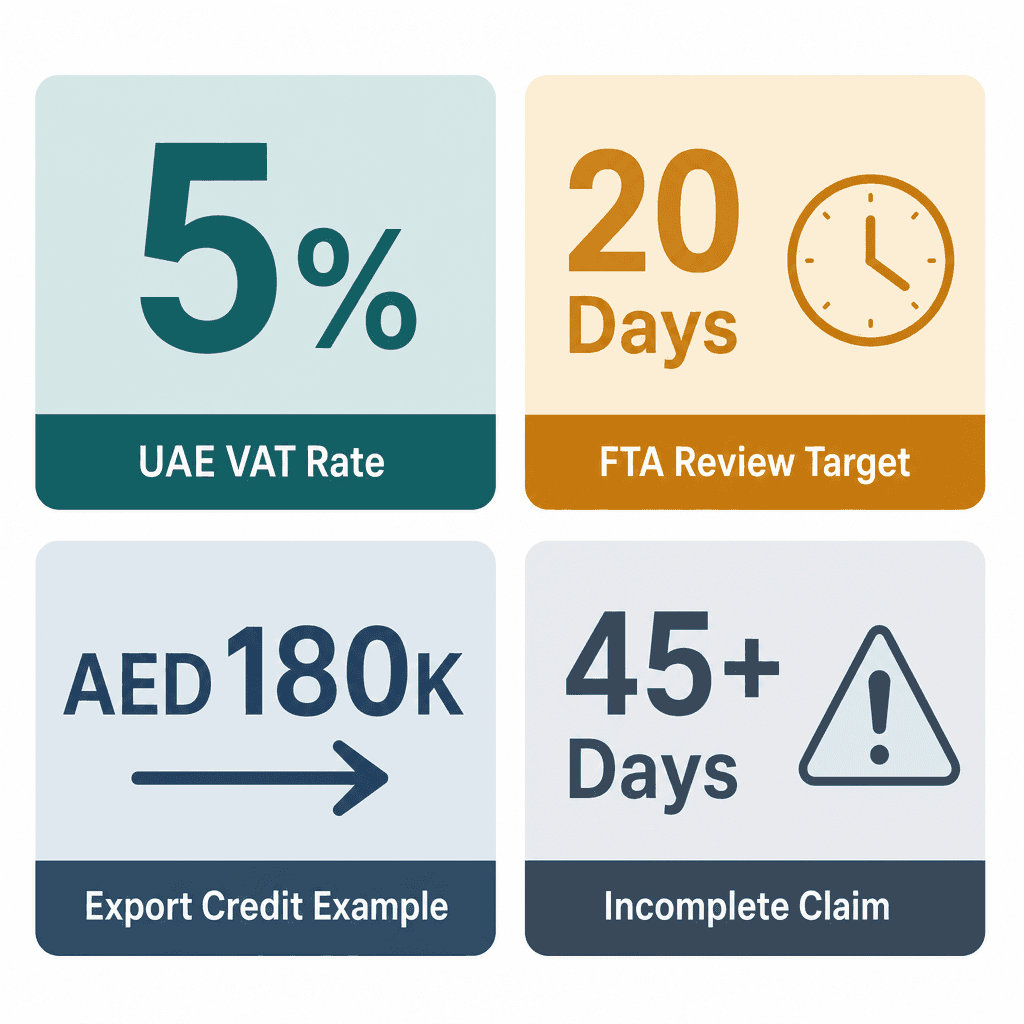

The UAE applies VAT at 5%, one of the lowest rates globally (Federal Tax Authority, 2017). Since VAT was introduced under Federal Decree-Law No. 8 of 2017, businesses have filed returns covering billions of dirhams in input and output tax each quarter. If your company paid more VAT on purchases than it charged on sales in any given period, you hold an excess VAT credit, and the FTA will refund it in cash. Yet many businesses either don't realise a refund is available, or they submit incomplete claims that get rejected outright. This guide is for any UAE-registered business owner or finance manager who wants to understand exactly when a VAT refund for companies in the UAE arises, which recovery route to choose, and how to file a clean application that clears the FTA's 20-working-day review window without triggering an audit.

What Is a VAT Refund for Companies in the UAE and When Does It Arise

A VAT refund for companies in the UAE arises when input tax paid on business purchases exceeds output tax charged on sales in a given tax period. The FTA recognises this as an excess VAT credit UAE situation and allows companies to either carry it forward or claim it back as a cash refund through EmaraTax. Understanding the mechanics is the first step to recovering money your business is genuinely owed.

Input Tax vs Output Tax: The Core Mechanics

Input tax is the 5% VAT your business pays on purchases, imports, and operating overheads. Output tax is the 5% VAT you charge customers on your taxable sales. When input exceeds output in a single tax period, the difference sits as a credit on your FTA account. That credit doesn't expire. You can carry it forward indefinitely or request a cash refund, the choice is yours.

Zero-rated exports under Article 45 of UAE Federal Decree-Law No. 8 of 2017 are the most common driver of structural credits. A Dubai South-based electronics exporter paying AED 180,000 in input VAT on components but charging AED 0 output VAT on zero-rated exports ends the quarter with an AED 180,000 refundable credit. That's not a rounding error, it's real cash sitting with the FTA. For foundational context on how UAE VAT works, see VAT in the UAE everything you need to know.

Three Business Profiles Most Likely to Have a Refundable VAT Credit

Exporters: Sales are zero-rated (0% output VAT) but inputs carry standard 5% VAT, creating a structural surplus every single period.

Startups and capital-expenditure-heavy businesses: Large upfront equipment and fit-out purchases generate significant input VAT long before revenue is substantial. A logistics company setting up a warehouse at Dubai South spending AED 2 million on fit-out in Q1 generates AED 100,000 in input VAT against minimal revenue, a textbook refund scenario. Capital expenditure VAT recovery is explicitly permitted under UAE VAT Executive Regulations, Article 75.

Project-based or seasonal businesses: Where invoices are delayed past the tax period, output tax recognition lags behind input tax spending, creating temporary but real credit positions.

Free zone companies making zero-rated supplies to non-UAE counterparties face this situation routinely. If you're a Dubai South tenant in logistics or e-commerce, you should be reviewing your VAT position every single return period, not just when a large credit accumulates. You can also check your registration status through our UAE VAT registration guide.

Carry Forward vs Cash Refund: Choosing the Right Route for Your VAT Credit

UAE businesses with an excess VAT credit UAE have two options: carry the credit forward to offset future output tax with no application required, or submit a standalone refund request to the FTA for a direct cash payment. Exporters and capital-intensive businesses almost always benefit more from requesting cash rather than waiting for offsetting sales that may never fully absorb the credit.

Carrying the Credit Forward: When It Makes Sense

Carrying forward requires no separate action. The credit appears automatically on your next VAT return and reduces the output tax you owe. There's no statutory time limit, credits can sit on your account indefinitely under UAE VAT law.

It's the right call if you're expecting strong taxable sales in the next one or two periods that will naturally absorb the balance. A UAE retailer with a AED 15,000 credit in Q1 and a confirmed Q2 sales pipeline may rationally skip the standalone application. But here's the thing: the FTA pays no interest on carried-forward credits. If the credit is large and future sales are uncertain, you're effectively giving the government an interest-free loan.

Requesting a Cash Refund: The Standalone Application Route

Any VAT-registered business can request a cash refund at any time when an excess credit exists. The request goes through the FTA EmaraTax portal (eservices.tax.gov.ae), it's entirely separate from your periodic VAT return. Once approved, funds transfer directly to your registered UAE bank account. No cheques are issued.

A Dubai-based engineering consultancy with AED 300,000 in quarterly input VAT on equipment imports and zero-rated project exports applies for a VAT refund for companies in the UAE each quarter to protect cash flow. That's the right strategy. The FTA targets 20 working days for complete applications (FTA, 2026). For ongoing compliance support, see accounting and tax compliance at Dubai South.

Carry Forward vs Cash Refund: Which Route Suits Your Business?

Feature | Carry Forward | Cash Refund Application |

|---|---|---|

Application Required | ✅ None, automatic | ❌ Standalone EmaraTax submission |

Processing Time | Immediate (next return) | 20 working days (FTA target) |

Cash Flow Impact | ❌ Capital remains tied up | ✅ Cash returned to business |

Interest on Credit | ❌ None paid by FTA | N/A, credit recovered |

Best For | Small credits, strong near-term sales | Exporters, startups, large credits |

Documentation Required | ✅ None additional | ❌ Full supporting file needed |

5 stepsh2>

To claim a VAT refund in the UAE, log in to the FTA EmaraTax portal, navigate to the VAT refund section, confirm your excess credit balance, complete the refund request form, upload supporting documents, and submit. The FTA typically processes complete applications within 20 working days and deposits funds directly to your registered bank account. Here's how each step works in practice.

Step 1: Confirm Your Excess Credit Balance Before Applying

Log in to EmaraTax at eservices.tax.gov.ae and open your VAT account dashboard. The excess credit figure shown must match your internal VAT ledger exactly. Any discrepancy needs to be resolved before you file, a mismatch is a direct audit flag.

Critically, ensure all prior VAT returns are filed with no outstanding penalties or liabilities. The FTA automatically offsets all outstanding debts before issuing any refund (UAE VAT Executive Regulations). A company that filed a late Q3 return and accrued a AED 1,000 penalty will see that amount deducted from its refund before the net balance transfers.

Step 2–4: Complete the Refund Form and Upload Documents

In EmaraTax, select "VAT Refund Request." You can claim a partial or full credit, you're not locked into claiming everything at once. Upload your supporting documents in PDF, JPEG, or PNG format (FTA portal guidance). Blurry scans are a surprisingly common rejection trigger.

Confirm your IBAN and bank name. The account holder name must match your registered trade name exactly, even a minor variation causes delays. A free zone trading company at Dubai South uploading export documentation should ensure customs exit certificates and commercial invoices are clearly legible and correctly named before hitting submit. Bank account verification can take 3–5 additional business days if the details haven't been previously confirmed.

Step 5: Submit and Track Your Application Status

Once submitted, you'll receive an FTA reference number. Track your application status in EmaraTax, statuses include "Under Review," "Additional Information Required," "Approved," and "Rejected." If the FTA requests additional information, respond within the specified window (typically 5 business days). Miss that window and the claim may be closed entirely.

A company that submitted a refund on 1 March 2025 and received an "Additional Information Required" notice on day 10 had its timeline reset. Final payment arrived on day 31 after supplementary documents were accepted. Clean, complete submissions avoid this entirely. The FTA target is 20 working days; incomplete applications can stretch to 45+ working days. If your claim is flagged for review, see our guide on tax audit in the UAE how to prepare.

Documents Required to Support a VAT Refund Claim in the UAE

To claim back VAT in Dubai, companies typically need FTA-compliant tax invoices for all input purchases, export documentation for zero-rated supplies, bank statements confirming payments, contracts for large-value transactions, and a VAT audit file reconciling the claim to filed returns. Getting this file right before submission is the single highest-leverage thing you can do.

Core Documents Every Applicant Must Provide

FTA-compliant tax invoices: Must include supplier TRN, date, description, unit price, VAT rate, and VAT amount stated separately, per UAE VAT Executive Regulations, Article 59.

Bank statements or payment proof: Confirming input VAT was actually paid, not just invoiced.

Filed VAT return copies: For every period to which the refund relates.

Trade license and TRN certificate: Confirming the entity is VAT-registered and active.

An FTA review of a AED 500,000 refund claim found that 20% of supporting invoices lacked the supplier's TRN. Those line items were disallowed outright, reducing the approved refund to AED 400,000. Verifying every supplier TRN against the FTA's public verification tool before submission takes minutes and saves thousands.

Additional Documents for Exporters and Capital Expenditure Claims

Goods exporters: UAE customs export declarations via Mirsal 2, airway bills, bills of lading, or courier receipts confirming physical export from UAE territory (UAE VAT Law, Article 45).

Service exporters: Contracts confirming the customer is outside the UAE and the service benefit was received abroad (UAE VAT Executive Regulations).

Capital expenditure claims: Purchase contracts, delivery notes, and asset registers confirming the asset is actively used for taxable business activities.

A manufacturer at Dubai South exporting goods to Saudi Arabia must provide both the UAE customs export declaration and the Saudi import clearance document to fully substantiate zero-rating on each shipment. For document management support, accounting and tax compliance at Dubai South covers this in detail.

How the FTA Processes VAT Refund Claims and What Triggers an Audit

The FTA reviews VAT refund applications from UAE companies within 20 working days for complete submissions (FTA, 2026). Large claim amounts, first-time applicants, high refund-to-revenue ratios, and inconsistencies between filed returns and supporting documents are the primary triggers for a deeper FTA audit. Knowing these triggers lets you prepare proactively.

The FTA's 20-Working-Day Review Timeline

The FTA's 20-working-day clock starts from the date a complete application is received. If the FTA issues an information request, the clock resets. Responding quickly, ideally within 48 hours rather than the full 5-day window, keeps your timeline on track. Once approved, funds transfer to your registered UAE bank account within approximately 3–5 additional business days.

A consultancy submitted a AED 120,000 refund claim on 3 February 2025 with complete documentation and received funds in its account by 4 March 2025, exactly 20 working days. That's achievable for any business with a clean, well-prepared file. Monitor your status daily through EmaraTax once you pass the 15-day mark.

Six Factors That Flag a Refund Claim for FTA Audit

Claim amount is disproportionately large relative to the company's revenue or filing history.

First-time refund applicant, the FTA applies heightened scrutiny to initial claims from any business.

Significant increase in claimed input VAT compared to prior periods without a clear documented reason.

Mismatch between customs export records and zero-rated sales figures on the VAT return.

Suppliers listed on invoices who are not VAT-registered or whose TRNs are invalid, one of the most common disallowance grounds in FTA reviews.

Outstanding tax liabilities or unfiled returns on the applicant's account at the time of submission.

A trading company claiming AED 2 million in input VAT in its first filing period with only AED 50,000 in declared sales was flagged for a full desk audit. The FTA requested 12 months of bank statements and full supplier verification. The

References

Editorial sources available on request. Full citation list is being compiled.