Topic Summary

VAT in the UAE applies to most goods and services, with supplies falling into standard-rated, zero-rated and exempt categories. This guide explains how value added tax works in practice, why the UAE introduced it, what falls under each supply type, and what businesses must do to stay compliant.

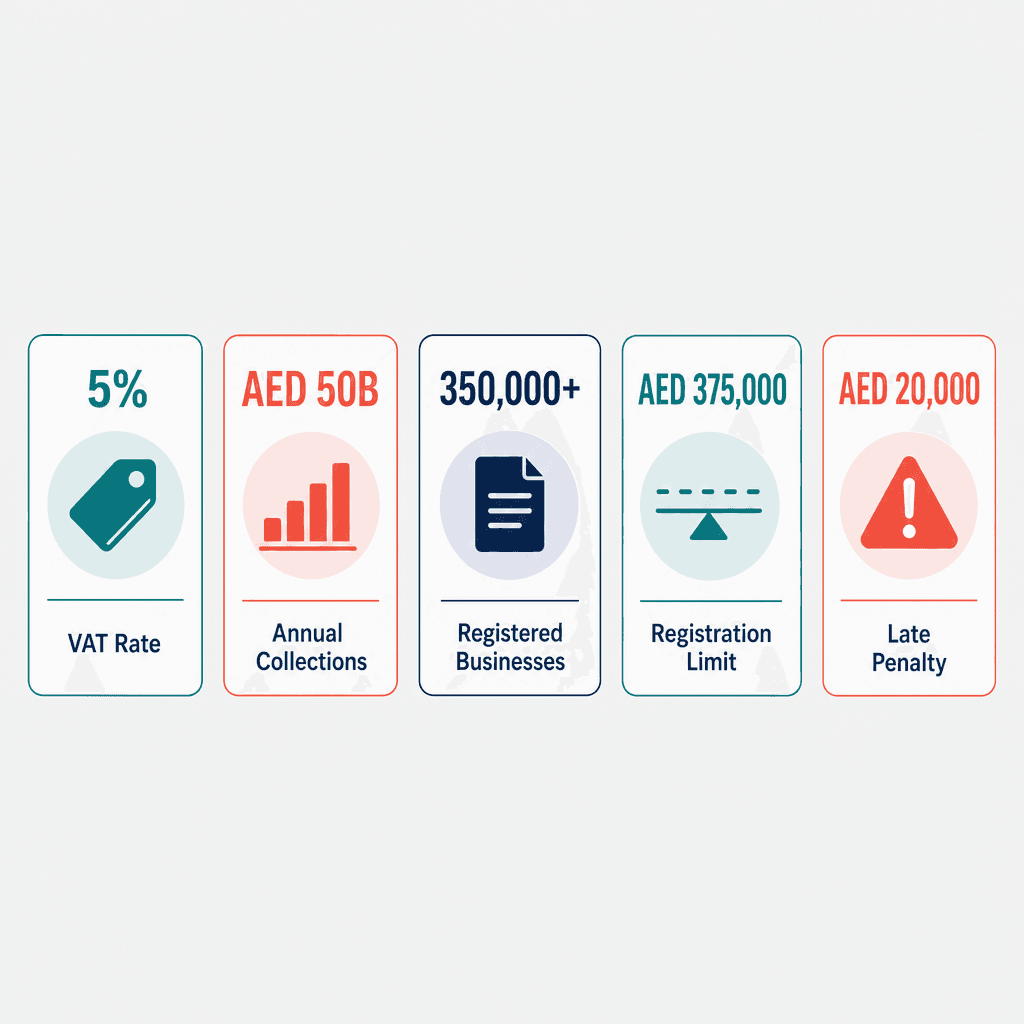

In 2026, the UAE collects over AED 50 billion annually through its VAT system (Federal Tax Authority, 2026). More than 350,000 businesses hold an active Tax Registration Number (TRN) (Federal Tax Authority, 2026). The Federal Tax Authority levied over AED 1.2 billion in administrative penalties in 2025 alone for non-compliance (UAE Ministry of Finance, 2025). The mandatory registration threshold sits at AED 375,000 in taxable turnover. Late registration penalties start at AED 20,000 (Federal Tax Authority, 2026).

VAT in UAE is a 5% consumption tax on most goods and services, introduced on 1 January 2018 under Federal Decree-Law No. 8 of 2017. This guide covers registration thresholds, zero-rated versus exempt supplies, the EmaraTax filing process, and free zone VAT rules, so you can stay compliant and protect your margins from day one. For a detailed walkthrough of the registration process alone, see our UAE VAT registration guide.

What Is VAT in UAE

VAT in UAE is a 5% consumption tax applied to most goods and services at each stage of the supply chain. Introduced on 1 January 2018 under Federal Decree-Law No. 8 of 2017, it is administered by the Federal Tax Authority. Businesses collect VAT from customers and remit the net amount to the government quarterly.

How Value Added Tax Works in Practice

The value added tax UAE system works on a chain principle. Every business in the supply chain, manufacturer, wholesaler, retailer, charges VAT on its sales and reclaims VAT on its purchases. Only the net difference goes to the Federal Tax Authority. The final consumer, who can't reclaim anything, bears the full cost.

Here's a concrete example. A Dubai-based electronics retailer sells a laptop for AED 5,000. They charge the customer AED 250 in VAT (5%). Their supplier had charged them AED 100 in VAT on the wholesale purchase. The retailer remits only AED 150 to the Federal Tax Authority, the difference between what they collected and what they paid. That's the core mechanic of vat uae in action.

Why the UAE Introduced VAT

The UAE introduced value added tax UAE as part of a deliberate strategy to reduce dependence on oil revenues. The government targeted AED 12 billion in first-year receipts when VAT launched in 2018. By 2026, annual VAT collections have grown to over AED 50 billion (Federal Tax Authority, 2026), a clear sign the system has matured.

The move also reflects the UAE's commitments under the Unified GCC VAT Agreement, which coordinates VAT policy across Gulf Cooperation Council member states. Saudi Arabia, Bahrain, and the UAE were the first to implement; the framework ensures cross-border trade within the GCC follows consistent rules. Businesses that understand vat uae mechanics can price competitively and avoid cash flow surprises at quarterly filing time.

UAE VAT Supply Type Comparison - Standard, Zero-Rated, and Exempt

Supply Type | VAT Rate | Input VAT Reclaimable? | Examples |

|---|---|---|---|

Standard-Rated | 5% | Yes | Retail goods, professional services, commercial rent, hospitality |

Zero-Rated | 0% | Yes | Exports outside GCC, international transport, healthcare, education, first residential supply |

Exempt | 0% | No | Bare land, residential rent (not first supply), local passenger transport, implicit financial services |

Out of Scope | N/A | N/A | Salary payments, inter-group dividends, activities outside UAE territory |

Registration Threshold (Mandatory) | AED 375,000 taxable turnover, apply within 30 days of crossing | All businesses supplying taxable goods or services in the UAE | |

Registration Threshold (Voluntary) | AED 187,500 taxable turnover, optional; enables input VAT recovery | Startups and SMEs wanting to reclaim input VAT before hitting mandatory threshold |

UAE VAT Rate and What It Applies To

The standard VAT rate in UAE is 5%, one of the lowest globally. It applies to most commercial goods, services, imports, and real estate transactions. Certain supplies are zero-rated at 0%, meaning VAT is charged but at a nil rate, and some categories are fully exempt from VAT entirely.

Goods and Services Subject to the 5% Standard Rate

Most of what businesses sell day-to-day falls under the standard 5% rate. Retail goods, professional services, hospitality, entertainment, and commercial real estate leases all attract VAT at 5%. A UAE management consultancy billing AED 100,000 to a mainland client charges AED 5,000 in VAT, no exceptions, no workarounds.

Imports of goods into the UAE mainland are subject to VAT at the point of customs clearance via dubai.customs.gov.ae. Worth flagging: B2B services supplied within the UAE are taxable regardless of where the recipient is based. Operating in a free zone doesn't shield you from VAT on services unless your zone is specifically designated under Cabinet Decision No. 59 of 2017.

Comparing Standard Rate, Zero Rate, and Exempt Supplies

The zero-rated versus exempt distinction is, in practice, the most misunderstood area of vat uae (Federal Tax Authority guidance, 2026). Both categories show 0% on the invoice, but the similarity ends there.

Zero-rated means you charge 0% VAT but can still reclaim all input VAT on your purchases. That's a genuine cash flow advantage. Exempt means you charge nothing and you can't reclaim input VAT either. For businesses with mixed supply types, exempt supplies create a hidden cost that erodes margins if not managed carefully.

Take a healthcare clinic as a real example. Patient consultations are VAT-exempt, the clinic charges no VAT and can't recover the VAT it paid on medical equipment purchases. But if that same clinic exports medical equipment to a GCC partner, that supply is zero-rated, meaning full input VAT recovery applies. Same business, two very different VAT outcomes depending on the supply type.

Who Must Register for VAT in UAE

Any UAE business with taxable supplies or imports exceeding AED 375,000 in the previous 12 months, or expected to exceed that threshold in the next 30 days, must register for VAT with the Federal Tax Authority. Voluntary registration is available for businesses with taxable supplies above AED 187,500.

Mandatory vs Voluntary VAT Registration Thresholds

The mandatory threshold is AED 375,000 in taxable turnover. Cross it, and you have 30 days to submit your vat registration uae application on EmaraTax. Miss that window and the Federal Tax Authority can back-date your TRN to the date you first crossed the threshold, triggering retrospective VAT liability on every sale you made without charging VAT.

The voluntary threshold is AED 187,500. Registering voluntarily makes sense if your suppliers are VAT-registered and you're paying significant input VAT on purchases. A Dubai South-based logistics startup hitting AED 200,000 in year one, for instance, could voluntarily register and reclaim AED 10,000 in input VAT paid on warehouse fit-out costs. Businesses below AED 187,500 can't register at all, factor that into your pricing model from the start.

Who Is Exempt from VAT Registration

Businesses that exclusively supply VAT-exempt goods or services, bare residential property rentals, local passenger transport, aren't required to register. Government entities and certain charities may also qualify for special VAT treatment under Federal Tax Authority directives.

One important exception: non-resident businesses supplying taxable goods or services in the UAE must register regardless of turnover. There's no threshold exemption for overseas entities. For example, a UK-based software firm selling subscriptions to UAE businesses must register from the first dirham of UAE revenue, while a small local business earning AED 150,000 annually sits below both thresholds and has no registration obligation unless they choose voluntary registration. You can start the registration process at eservices.tax.gov.ae. For TRN verification once registered, see our TRN verification Dubai guide.

Zero-Rated vs VAT-Exempt Supplies

Zero-rated supplies are taxed at 0% but allow the supplier to reclaim input VAT, exports, international transport, and healthcare are key examples. Exempt supplies carry no VAT charge but deny the supplier any input VAT recovery. The distinction directly affects your cash flow and pricing strategy in UAE.

Categories of Zero-Rated Supplies in UAE

Zero-rated categories are defined in Cabinet Decision No. 52 of 2017. If your business falls into any of these, you charge 0% VAT but retain full input VAT recovery rights:

Exports of goods outside the GCC, critical for UAE trading and re-export businesses

International passenger and freight transport services

Healthcare services and related goods (medicines, medical equipment) supplied by licensed providers

Educational services provided by accredited institutions

First supply of newly completed residential buildings within 3 years of completion

A Dubai South free zone re-exporter shipping electronics to Europe charges 0% VAT on the export invoice and reclaims all input VAT on local procurement, turning zero-rating into a genuine competitive advantage on international pricing.

Categories of VAT-Exempt Supplies in UAE

Exempt supplies generate no VAT revenue for the government, and no input VAT recovery for you. The main categories are bare land sales, residential property rentals (excluding the first supply), local passenger transport (taxis, buses, metro), and implicit financial services such as interest on loans.

A UAE bank is a useful illustration. It charges no VAT on mortgage interest, that's exempt. But it charges 5% VAT on advisory fees, that's standard-rated. Because the bank makes both exempt and taxable supplies, it must apply a partial exemption calculation under Federal Tax Authority Public Clarification VAT 001 to determine how much of its input VAT it can actually recover. Mixed supply businesses should take this seriously, it's not a minor administrative detail; it directly affects profitability.

Is my healthcare business zero-rated or exempt for UAE VAT?

Licensed healthcare providers supplying medical services and qualifying goods are zero-rated under Cabinet Decision No. 52 of 2017, meaning they charge 0% VAT and can reclaim input VAT in full. Non-licensed health-related activities may fall under the standard 5% rate. Always confirm your specific activity with a Federal Tax Authority-approved tax agent.

How to Register for VAT - Step by Step

To register for VAT in UAE, create an EmaraTax account at eservices.tax.gov.ae, complete the VAT registration form with trade license and financial details, upload supporting documents, and submit. The Federal Tax Authority issues your Tax Registration Number within 20 business days. Late registration penalties start at AED 20,000.

Documents You Need Before You Start

Gather these before logging into EmaraTax. Missing even one document is the most common cause of delayed TRN issuance:

Valid trade license, mainland DED license or free zone license

Emirates ID and passport copy of the authorised signatory

Proof of taxable turnover: audited financials, bank statements, or signed sales contracts for the past 12 months

Business bank account details in AED

Customs registration number from dubai.customs.gov.ae if you import goods

A new Dubai South Business Hub Free Zone company can typically assemble this full document pack in under two hours using the Federal Tax Authority's pre-registration checklist at tax.gov.ae.

Step-by-Step VAT Registration on EmaraTax

Step 1: Go to eservices.tax.gov.ae and create an EmaraTax account using your Emirates ID or UAE Pass.

Step 2: Select "Register for VAT" and complete all form sections, business details, activity type, turnover figures, and AED bank account information.

Step 3: Upload all required documents in PDF or JPEG format (maximum 5MB per file).

Step 4: Review the declaration and submit. You receive an acknowledgement reference number immediately on screen.

Step 5: The Federal Tax Authority reviews your application within 20 business days and issues your 15-digit TRN by email.

In practice, a trading company at Dubai South Business Hub Free Zone completed EmaraTax registration in 45 minutes and received its TRN within 14 business days, six days ahead of the statutory maximum. Don't wait until you're close to the AED 375,000 threshold. The AED 20,000 penalty for late registration makes early action the only sensible approach (Federal Tax Authority, 2026).

How to File VAT Returns in UAE

UAE VAT returns are filed quarterly through EmaraTax at eservices.tax.gov.ae. You report total output VAT collected, deduct eligible input VAT, and pay the net amount, or claim a refund if input VAT exceeds output. Returns are due within 28 days of the end of each tax period. Late filing attracts an AED 1,000 penalty.

Understanding Output VAT, Input VAT, and Net Payable

Output VAT is the 5% you charge customers on taxable sales, you're collecting it on behalf of the Federal Tax Authority, not keeping it. Input VAT is the 5% your suppliers charge you on business purchases, this is reclaimable. Net VAT payable is simply output minus input.

Here's a real Q1 calculation: a Dubai-based IT firm collects AED 25,000 in output VAT on client invoices and pays AED 8,000 in input VAT on software licenses and office rent. Net payable to the Federal Tax Authority: AED 17,000. If input exceeds output, you apply for a refund or carry the credit forward to the next period.

Keep every valid tax invoice. Under Article 59 of the UAE VAT Executive Regulations, a valid tax invoice must show the supplier's TRN, supply date, taxable amount, and VAT amount separately. Missing documentation is the most common reason input VAT claims are rejected during a Federal Tax Authority audit.

VAT Return Filing Deadlines and Penalties

Most businesses file quarterly. Businesses with annual turnover above AED 150 million may be assigned a monthly tax period by the Federal Tax Authority. Returns and payments are due by the 28th day after the period ends, so Q1 (January to March) is due 28 April.

The penalty structure is worth knowing in detail:

Late filing: AED 1,000 for the first offence; AED 2,000 for a repeat within 24 months

Late payment: 2% of unpaid tax immediately on day one

Late payment: additional 4% after 7 days

Late payment: 1% per day after one month, capped at 300% of the unpaid amount (Federal Tax Authority, 2026)

A retailer missing the 28 April deadline by 10 days on AED 50,000 VAT payable incurs AED 1,000 in filing penalties plus roughly AED 3,000 in late payment surcharges. That's AED 4,000 lost to avoidable non-compliance. For a broader view of how VAT interacts with the UAE's 9% corporate tax rate, see our UAE corporate tax explained guide.

What happens if my input VAT exceeds output VAT in a quarter?

If your input VAT exceeds output VAT, you have a VAT credit. You can apply for a cash refund via EmaraTax or carry the credit forward to offset future VAT liabilities. Export-heavy businesses and new businesses with high setup costs commonly find themselves in a net credit position in early quarters.

VAT in Free Zones - Special Rules

Not all UAE free zones are equal for VAT. Designated Zones are treated as outside the UAE for VAT purposes, meaning goods moving between them are generally not subject to VAT. Non-designated free zones follow standard UAE VAT rules. Most free zones, including Dubai South Business Hub Free Zone, are non-designated unless specifically listed by the Federal Tax Authority.

Designated Zones vs Non-Designated Free Zones

Designated Zones are defined by Cabinet Decision No. 59 of 2017 and treated as outside UAE territory for VAT on goods. Jebel Ali Free Zone (JAFZA)

References

Federal Tax Authority (tax.gov.ae)

eservices.tax.gov.ae (eservices.tax.gov.ae)