Topic Summary

Banking works differently for free zone companies because banks assess your legal status, activity and documentation more closely at onboarding. This guide explains what banks are actually assessing, the core document checklist every UAE bank requires, the additional documents often requested, and which banks work best with free zone companies.

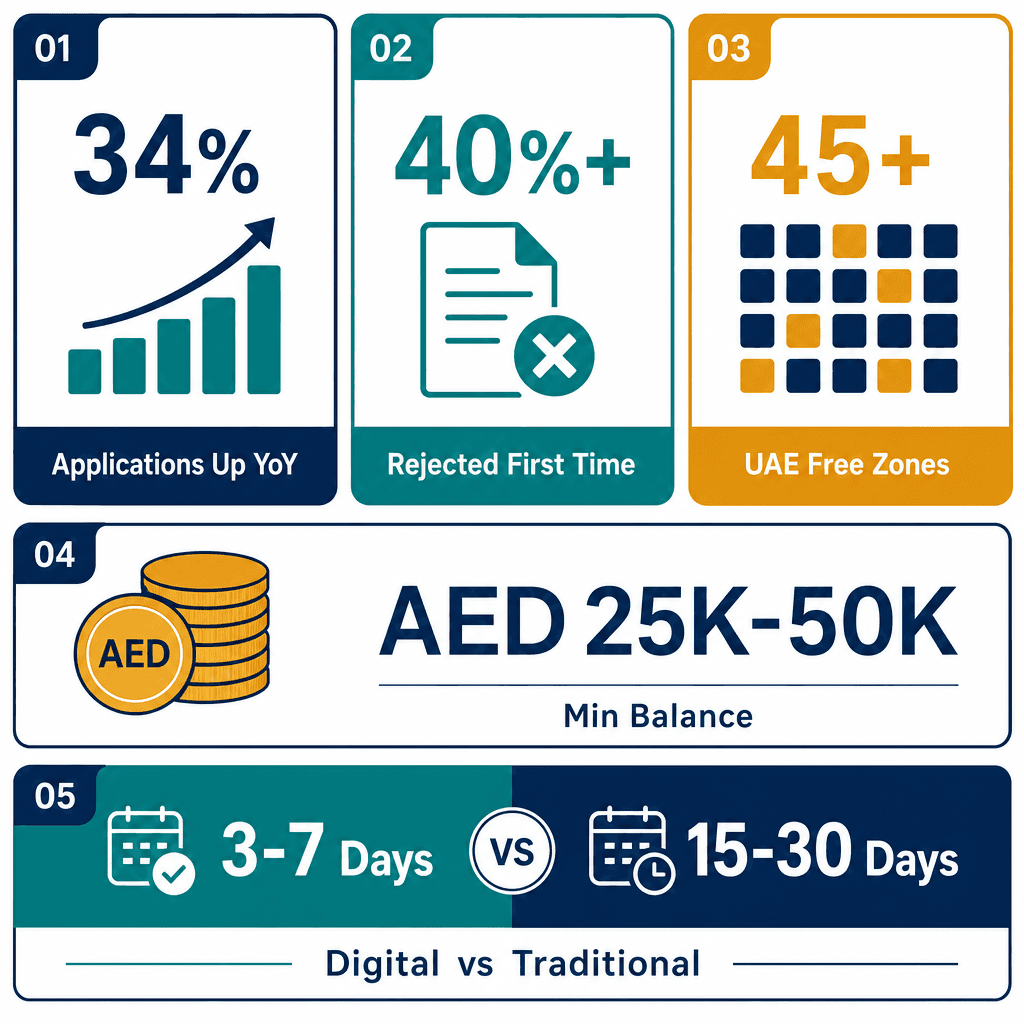

In 2026, corporate bank account applications from free zone companies increased by 34% year-on-year (UAE Central Bank, 2026). Over 40% of first-time applicants face rejection due to incomplete documentation (Dubai Chamber of Commerce, 2026). The UAE has 45+ free zones as of 2026 (UAE Ministry of Economy, 2026). Non-resident shareholders trigger enhanced KYC in 78% of applications (Dubai Chamber of Commerce, 2026). Traditional bank onboarding averages 15–30 business days, while digital banks process accounts in 3–7 days (UAE Central Bank, 2026).

The banking requirements for Dubai free zone companies centre on a verified trade license, certified Memorandum of Association, shareholder passports, and a credible business plan submitted to a UAE-licensed bank. Most corporate accounts require a minimum average balance of AED 25,000 to AED 50,000 depending on the institution. This guide covers every banking requirement for Dubai free zone companies, from mandatory documents and KYC steps to the best-fit banks, minimum balances in AED, rejection triggers, and how to open a corporate bank account Dubai with confidence in 2026.

Why Banking is Different for Free Zone Companies

Free zone companies operate under a distinct legal framework outside UAE mainland jurisdiction, which means UAE banks apply additional due diligence. Banks must verify the free zone authority, assess the business model's credibility, and confirm the company has genuine commercial activity, making the banking requirements for Dubai free zone entities more rigorous than mainland applications.

Free Zone Legal Status and Its Impact on Bank Onboarding

Free zone companies are incorporated under individual free zone authorities, Dubai South, other UAE free zones, not the UAE mainland Department of Economic Development (DED). Banks must verify each authority's legitimacy separately, which adds a layer of review that mainland applicants simply don't face. The UAE has 45+ free zones as of 2026 (UAE Ministry of Economy, 2026), and not every bank has pre-approved every one of them.

UAE banks treat free zone entities as higher-risk for Anti-Money Laundering and Counter-Financing of Terrorism (AML/CFT) purposes. The reason is straightforward: free zone companies can trade internationally with minimal physical presence, which raises questions about substance. Outside the Dubai International Financial Centre (DIFC), where the Dubai Financial Services Authority (DFSA) governs financial services, the UAE Central Bank oversees all corporate bank account compliance (cbuae.gov.ae).

A logistics company licensed under Dubai South Business Hub Free Zone, for example, must provide its free zone trade license, not a DED license, and banks will cross-reference the license number directly with the free zone authority portal before proceeding. Banks typically require 2–4 weeks of additional review for free zone versus mainland applicants (Dubai Chamber of Commerce, 2026).

What Banks Are Actually Assessing When You Apply

Banks run three parallel assessments on every free zone banking application:

Substance: Banks verify the company has real economic activity, signed contracts, invoices, or client letters. A registered address alone won't satisfy this.

Source of funds: Shareholders must explain where the initial share capital originates, especially non-UAE-resident directors.

Business model clarity: Vague activity descriptions like "general trading" trigger enhanced due diligence and, frequently, rejection. Over 40% of rejections cite insufficient business substance evidence (Dubai Chamber of Commerce, 2026).

A technology consultancy applying to Emirates NBD was asked to provide two signed client contracts and a 12-month revenue projection alongside the standard document pack, a common enhanced due diligence request for free zone service companies. That's not unusual; it's the new baseline for free zone company banking in Dubai.

Documents Required for Free Zone Company Bank Account

To open a bank account for a free zone company in the UAE, you need: a valid free zone trade license, certified Memorandum of Association, passport copies of all shareholders and directors, Emirates ID or UAE visa for residents, proof of business address, and a written business plan with projected financials. Some banks add a source-of-funds declaration. The bank documents for a free zone UAE application split into two categories: non-negotiable core documents and commonly requested supplementary items.

Core Document Checklist for All UAE Banks

95% of UAE banks require a certified MoA as non-negotiable (UAE Central Bank, 2026). Here's the full core list:

Valid free zone trade license, must not be within 3 months of expiry at time of application.

Certified Memorandum of Association (MoA) and Articles of Association, Arabic translation required by some banks. Free zone MoAs are issued by the free zone authority, not a UAE notary, brief your bank on this distinction upfront.

Passport copies of all shareholders, directors, and Ultimate Beneficial Owners (UBOs), minimum 6 months validity required.

Emirates ID for UAE-resident shareholders; UAE entry visa copy for non-residents.

Proof of registered business address, a free zone tenancy agreement or flexi-desk certificate is accepted.

Business plan with 12-month financial projections, increasingly treated as a core requirement, not supplementary.

Dubai South Business Hub Free Zone issues a tenancy or flexi-desk certificate alongside the trade license. This single document satisfies the proof-of-address requirement accepted by Emirates NBD, Mashreq, and ADCB, no separate utility bill or lease is needed.

Additional Documents Banks Often Request

Beyond the core pack, expect these requests, particularly if any shareholder is a non-GCC national:

Source-of-funds declaration: A signed letter explaining the origin of shareholders' capital. Mashreq and FAB require this for non-resident shareholders.

Bank reference letters from shareholders' existing banks, standard practice for non-GCC nationals.

Signed client contracts or letters of intent to demonstrate a real business pipeline.

CV or professional profile of the company's General Manager or authorised signatory.

A German national setting up a consultancy at a Dubai free zone was asked by ADCB to provide a bank reference letter from their Deutsche Bank account alongside the standard pack. Non-resident shareholders trigger enhanced KYC in 78% of UAE bank applications (Dubai Chamber of Commerce, 2026), so prepare this early rather than scrambling after the bank requests it.

Which UAE Banks Work Best with Free Zone Companies

Emirates NBD, Mashreq Bank, ADCB, and First Abu Dhabi Bank (FAB) are the most accessible UAE banks for free zone companies in 2026. Each has a dedicated business banking team experienced with free zone structures. Mashreq Business Edge and ADCB BusinessEdge offer streamlined onboarding with relationship manager support from day one. For free zone company banking in Dubai, choosing the right institution from the start saves weeks.

Top Conventional Banks for Free Zone Business Accounts

Emirates NBD: Largest UAE bank by assets (AED 740 billion as of 2026, Emirates NBD Annual Report, 2026), strong free zone onboarding team, accepts most free zone authorities. Minimum balance: AED 50,000.

Mashreq Bank: Fastest onboarding among traditional banks, average 10–15 business days for free zone accounts (Mashreq Bank, 2026). Dedicated relationship managers from application day.

ADCB BusinessEdge: Competitive for SMEs, minimum balance AED 25,000, accepts flexi-desk addresses from approved free zones.

FAB (First Abu Dhabi Bank): Preferred for companies with high international transaction volumes. Strong SWIFT network for cross-border payments.

A Dubai South Business Hub Free Zone-licensed trading company opened a Mashreq Business Edge account in 12 business days by submitting a complete document pack upfront, including a business plan and two signed client contracts, avoiding the back-and-forth that routinely extends timelines at other institutions.

UAE Bank Minimum Balances and Account Opening Timelines for Free Zone Companies (2026)

Bank | Min Average Balance (AED) | Below-Balance Fee (AED/month) | Typical Approval Timeline | Free Zone Friendly |

|---|---|---|---|---|

Emirates NBD Business Account | 50,000 | 500 | 15–20 business days | High, accepts most UAE free zones |

Mashreq Business Edge | 25,000 | 250 | 10–15 business days | High, fastest traditional bank onboarding |

ADCB BusinessEdge | 25,000 | 300 | 15–25 business days | High, accepts flexi-desk addresses |

FAB Business Account | 50,000 | 500 | 20–30 business days | High, preferred for international payments |

RAKBANK Business Current Account | 25,000 | 300 | 15–20 business days | Medium-High, strong SME focus |

Wio Business (Digital) | Zero | Zero | 3–5 business days | High, fully digital, no branch visit |

Islamic Banking Options for Free Zone Companies

Dubai Islamic Bank (DIB) offers Sharia-compliant current accounts for free zone companies with a minimum balance of AED 25,000. It's particularly strong for GCC-based shareholders and companies in the halal trade or food sectors. Abu Dhabi Islamic Bank (ADIB) is competitive for manufacturing and trading free zone companies and accepts most UAE free zone licenses. Both institutions offer profit-sharing deposit accounts as an alternative to interest-bearing savings, Islamic banking assets in the UAE reached AED 895 billion in 2025 (UAE Central Bank, 2026), reflecting the scale of this option.

A Halal food trading company licensed at a Dubai free zone chose Dubai Islamic Bank for its Sharia-compliant current account structure, which aligned with its shareholders' preferences and the nature of its import/export business. Worth noting: not all UAE banks accept every free zone. Confirm your free zone appears on the bank's approved list before submitting an application. Explore your options through Dubai South Beyond Hub banking for pre-vetted introductions.

Minimum Balances in AED

UAE corporate bank account minimum balances for free zone companies range from AED 25,000 to AED 50,000 as an average monthly balance in 2026. Falling below the threshold triggers monthly fees of AED 250 to AED 500. Digital banks like Wio Business require no minimum balance, making them a viable alternative for early-stage free zone companies managing tight cash flow.

How to Maintain Minimum Balance Without Straining Cash Flow

Negotiate a waiver period: Most banks offer a 3-month minimum balance waiver for new accounts. Mashreq routinely grants this to new free zone clients on request through a relationship manager, it's not advertised, but it's available. Always ask.

Use a digital bank as a secondary account: Keep day-to-day transactions on a zero-balance digital account while the traditional bank balance stays intact above the threshold.

Set an internal alert at 110% of the minimum threshold: This gives you a buffer before fees kick in and time to transfer funds without panic.

A startup e-commerce company at a Dubai free zone chose Wio Business as its primary account for the first 12 months, zero minimum balance removed cash flow pressure while the business scaled, then migrated to Emirates NBD once monthly revenues exceeded AED 100,000. Wio Bank processed over 50,000 SME account applications in 2025 (Wio Bank, 2026), confirming its credibility as a primary banking option.

KYC Process for Free Zone Companies

The KYC process for free zone companies in the UAE involves five steps: submitting the document pack, identity verification of all UBOs, business activity assessment, source-of-funds review, and final compliance approval. The UAE Central Bank mandates this process under AML/CFT Federal Decree-Law No. 20 of 2018. The full process takes 10–30 business days depending on the bank. Knowing how to open a bank account for a free zone in Dubai starts with understanding exactly what happens after you submit.

Step-by-Step KYC Process for Free Zone Bank Account Opening

Submit your complete document pack to the bank's business banking team. Incomplete packs are the single most common cause of delays, banks pause the clock and wait for missing items.

Identity verification of all shareholders, directors, and UBOs against international sanctions lists: OFAC, UN consolidated list, and EU restrictive measures.

Business activity review: Compliance assesses whether the stated activity matches the trade license category and the business plan. Mismatches here trigger requests for clarification or additional documents.

Source-of-funds verification: Shareholders submit 6-month bank statements or a signed declaration explaining the origin of share capital.

Final approval by the bank's compliance committee: You receive account details and a UAE IBAN within 2–5 business days of approval.

An IT services company at Dubai South Business Hub Free Zone cleared KYC with Emirates NBD in 14 business days by submitting all five document categories in one go, including a detailed business plan with named clients and a 12-month P&L projection. UAE Federal Decree-Law No. 20 of 2018 mandates UBO disclosure for all corporate bank accounts (UAE Ministry of Economy, 2026), this is not optional.

UBO Disclosure Rules Every Free Zone Owner Must Know

Any individual owning 25% or more of the company's shares is classified as a UBO and must be disclosed to the bank.

Banks must file UBO data with the UAE goAML platform (goaml.ae), non-disclosure is a criminal offence under UAE AML law.

If a corporate shareholder owns shares, the bank traces ownership back to the natural person. Have a corporate structure chart ready before submission.

A free zone holding company with a Cayman Islands parent was required to provide a full ownership structure chart tracing back to the individual shareholder, Emirates NBD required this before proceeding to KYC step 3. The UAE ranked 5th globally for AML compliance frameworks in 2025 (FATF, 2025), so expect the process to be thorough. Free zone companies with foreign shareholders trigger enhanced KYC at all UAE banks. That's standard, not a red flag, open a corporate bank account Dubai with a complete pack and the process moves predictably.

What is the minimum balance for a UAE corporate bank account?

The minimum average monthly balance for a UAE corporate bank account ranges from AED 25,000 at Mashreq Business Edge and ADCB BusinessEdge to AED 50,000 at Emirates NBD and FAB. Digital banks like Wio Business require zero minimum balance. Falling below the threshold at traditional banks triggers monthly fees of AED 250 to AED 500.

Common Reasons for Bank Account Rejection

UAE banks reject free zone company bank applications most often for five reasons: incomplete or expired documents, vague business activity descriptions, high-risk nationality combinations triggering enhanced due diligence, no evidence of genuine business substance, and shareholders appearing on international sanctions lists. Addressing these before submission cuts rejection rates significantly. The banking requirements for Dubai free zone applicants are strict, but the rejection triggers are entirely avoidable.

The Five Most Common Rejection Triggers

Expired or near-expiry trade license: Banks reject any license expiring within 3 months of the application date. Renew first, apply second.

Vague activity description: "General trading" without specifying goods, target markets, or suppliers triggers automatic enhanced review and, often, rejection. Vague activity descriptions account for 28% of rejections (Dubai Chamber of Commerce, 2026).

No business substance: A free zone address with no staff, no contracts, and no client pipeline signals a shell company to compliance teams.

Shareholders from FATF high-risk jurisdictions: Iran, Myanmar, and North Korea result in automatic rejection at most UAE banks.

Mismatched information: Spelling differences in a shareholder's name across passport, MoA, and trade license cause compliance flags that halt applications entirely.

A trading company was rejected by two banks because its MoA listed the shareholder as "Mohammed Al Rashid" while the passport read "Mohammad Al Rasheed", a minor variation that required a notarised correction before reapplication. Over 40% of first-time free zone bank applications face rejection (Dubai Chamber of Commerce, 2026). That statistic drops sharply when applicants address all five triggers before submitting.

How to Reapply After a Rejection

Request a written explanation: Banks aren't legally obligated to provide one, but many will if asked directly through a relationship manager. Get specifics before rebuilding your pack.

Address every identified gap: Resubmitting the same incomplete pack is the most common reapplication mistake. Fix everything, not just the flagged item.

Apply to a different bank simultaneously: Rejection from one institution has no bearing on your eligibility at another. Run parallel applications to save time.

After rejection from FAB for insufficient business substance, a Dubai free zone consultancy added two signed client letters, a revised business plan, and the GM's LinkedIn profile to its reapplication pack, approved by Mashreq within 11 business days. For structured support with your application,

References

cbuae.gov.ae (cbuae.gov.ae)

Wio Bank, 2026 (wio.io)

FAQ