Topic Summary

Banking for startups in the UAE is more demanding than most founders expect, with stricter compliance checks than Western markets. This guide explains why, compares traditional and digital-first banks for startups, and covers the accounts your startup actually needs, from the operational current account to multi-currency options.

By Editorial Team, Business setup specialists covering UAE free zone incorporation, corporate banking, and regulatory compliance. Full bio →

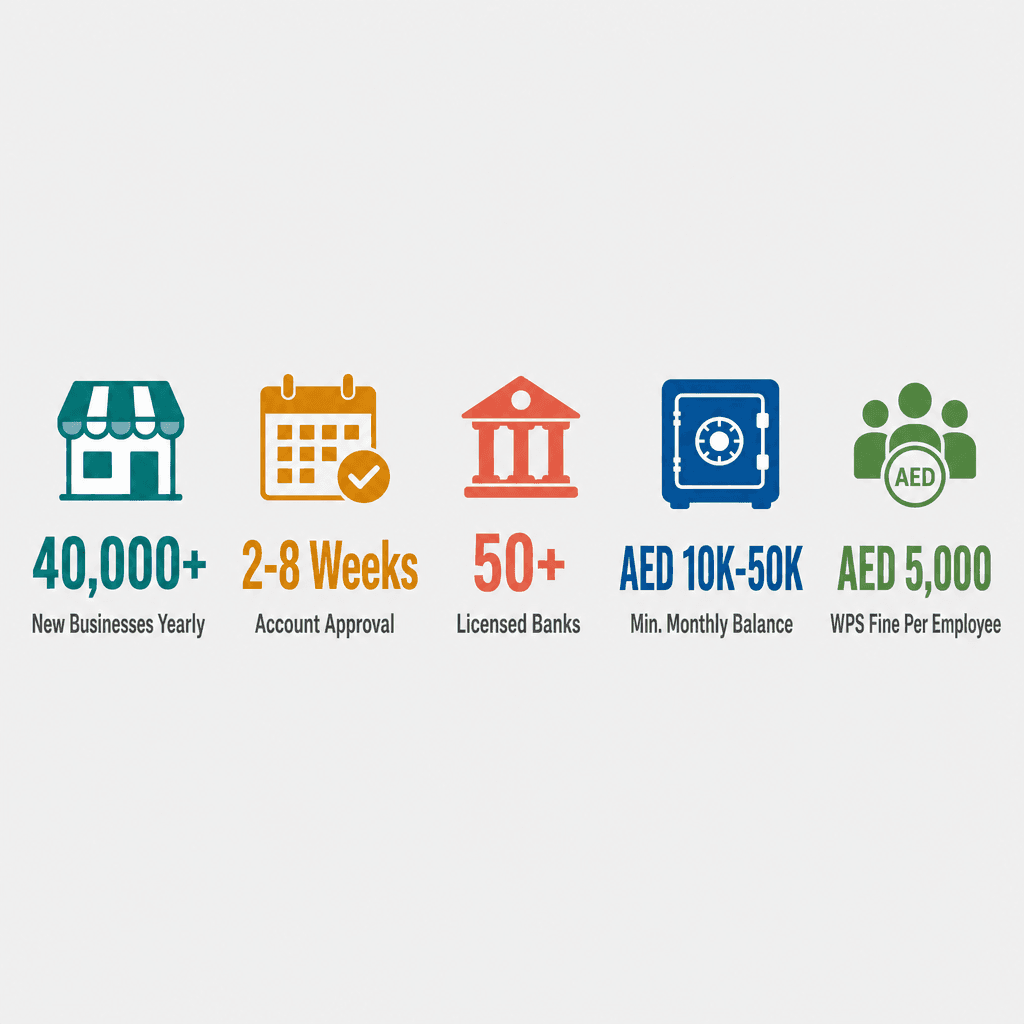

Over 40,000 new businesses register in the UAE every year, yet a significant share stall at the banking stage rather than incorporation (UAE Government Portal, 2025). Corporate account approval timelines run 2–8 weeks on average. The Central Bank of the UAE (CBUAE) supervises more than 50 licensed banks, each applying its own KYC threshold. Minimum monthly balances range from AED 10,000 to AED 50,000 depending on the institution. WPS non-compliance fines start at AED 5,000 per employee (MoHRE, 2024). Payment gateway fees typically run 2.5–3.5% per transaction. For first-time founders, banking for startups in the UAE is frequently the steepest part of the entire setup process.

This guide gives you the foundational context you need: how the UAE banking landscape works, which accounts to open, what banks look for, how to build a lasting relationship with your bank, and when to bring in payment gateways and a second account.

What Is Banking for Startups in the UAE and Why It Differs From the West

Banking for startups in the UAE involves opening a corporate account with a licensed UAE bank or a digital-first alternative. Unlike Europe or the US, the process is stricter, approval timelines are longer, KYC requirements are more extensive, and the choices you make in your first six months directly shape your long-term banking relationships.

Why UAE Banking Is More Demanding Than Most Founders Expect

UAE banks operate under CBUAE anti-money laundering (AML) and Know Your Customer (KYC) frameworks that go well beyond standard Western requirements. A bank can decline your application without a formal explanation, and there's no universal appeals process. That opacity catches a lot of founders off guard.

The compliance footprint you build in your first six months follows your company. Which bank you choose, which account type you open, and how you transact all feed into a risk profile that shapes every future banking interaction. There's no equivalent of a UK or US business current account you can open online in minutes.

No online-only instant approval for corporate accounts

Enhanced due diligence for cross-border ownership structures

Business activity risk classification affects approval speed

Shareholder nationality and residency history are evaluated

A US-founded SaaS startup incorporated in a Dubai free zone was declined by two major UAE banks before succeeding with a third. The difference was a structured business plan and a shareholder with a clean UAE residency history, a small detail that carries significant weight in the onboarding process.

Traditional Banks vs Digital-First Banks in the UAE

Traditional banks (Emirates NBD, ADCB, RAKBank, Mashreq, FAB) offer full corporate services including trade finance, credit facilities, and WPS payroll processing. The trade-off is longer onboarding timelines. Digital-first options like Wio Bank (launched 2022 as the UAE's first purpose-built digital business bank), Liv Business, and YAP for Business offer faster account opening and lower minimum balances, but may not cover everything a scaling startup needs.

RAKBank business banking at Dubai South is worth an early conversation if you're based in that free zone. The bank has an active partnership with Dubai South Business Hub and dedicated relationship managers who understand the free zone's licensing structure from day one.

Traditional Banks vs Digital-First Banks for UAE Startups

Feature | Traditional Banks (RAKBank, Emirates NBD, ADCB) | Digital-First Banks (Wio, Liv Business, YAP) |

|---|---|---|

Account Opening Timeline | 2–8 weeks; in-person meetings typically required | 3–10 business days; largely digital process |

Minimum Balance Requirement | AED 10,000–AED 50,000 average monthly balance | AED 0–AED 5,000; lower or zero thresholds common |

WPS Support | ✅ Fully registered WPS agents; dedicated payroll teams | Limited; check WPS registration status before committing |

Multi-Currency Accounts | ✅ USD, EUR, GBP and more; full FX desk access | Wio supports multiple currencies; others vary |

Trade Finance / Credit Facilities | ✅ Letters of credit, overdrafts, SME loans available | ❌ Limited or unavailable at early stage |

Onboarding Process | Relationship manager-led; more documentation required | App-based; lighter document set; faster decisions |

Best For | Startups needing WPS, trade finance, or high-volume B2B transactions | Early-stage startups needing a fast operational account with low overheads |

Which Bank Accounts Your UAE Startup Actually Needs

Most UAE startups need a dirham current account for daily operations as a minimum. If you trade internationally, a multi-currency account prevents costly conversion fees. Companies using e-commerce or subscription billing also need a payment gateway integration. You don't need all three on day one, prioritise based on your revenue model.

The AED Current Account: Your Operational Foundation

Every startup needs an AED current account. It's your operational hub: paying suppliers, receiving client payments in dirhams, and running payroll through the UAE's Wage Protection System (WPS). Without it, you can't function legally as an employer or transact with most UAE-based counterparties.

Minimum monthly balance requirements range from AED 10,000 to AED 50,000 across major UAE banks. Monthly maintenance fees run AED 0–AED 500 depending on whether you maintain that balance. Make sure your account includes online banking access and a corporate debit card from day one, it sounds basic, but these are frequently overlooked in the onboarding rush.

A logistics startup at Dubai South used their RAKBank current account to process WPS payroll for 12 employees and receive AED-denominated client payments within their first 30 days of trading. Getting the account right early meant zero payroll disruption from the start.

A quick checklist of features to confirm at account opening:

Online banking portal with corporate access levels

Corporate debit card (ideally Visa or Mastercard)

WPS payroll processing enabled

Cheque book facility (still required for some UAE transactions)

SWIFT/IBAN details for international receipts

Multi-Currency Accounts for Internationally Trading Startups

If you invoice in USD, EUR, or GBP, a multi-currency account is worth the extra setup effort. UAE banks typically charge a 1–3% FX margin on currency conversions, and those costs compound fast for an active international business. The AED is pegged to the USD at 3.6725, so USD conversion risk is minimal, but EUR and GBP conversions carry the full margin.

Emirates NBD, Mashreq, and ADCB all offer multi-currency business accounts. Wio Bank also supports multiple currencies on the digital side. A consultancy billing European clients in EUR used a Mashreq multi-currency account to hold EUR balances and convert only when the rate was favourable, saving an estimated 2.1% per transaction. That's meaningful margin at scale.

For a deeper walkthrough of the account opening process, see this guide on how to open a corporate bank account in Dubai.

5 Steps to Get Your UAE Startup Bank Account Approved

To get a UAE startup bank account approved, prepare a detailed business plan, ensure all shareholder documents are current, choose a bank aligned with your business activity, submit a complete KYC package, and follow up proactively. Most applications take 2–8 weeks. Incomplete documentation is the most common reason for delays.

What Banks Actually Evaluate During Onboarding

Here's what banks are actually looking at when they review your application:

Business activity risk level. Banks classify activities as low, medium, or high risk. Crypto, forex trading, and cash-intensive businesses face the most scrutiny. A standard consultancy or logistics company sits in a much more comfortable risk band.

Shareholder profiles. Nationality, residency status, existing UAE banking history, and PEP (politically exposed person) status all affect your approval odds. A clean UAE residency record helps significantly.

Trading history. New companies with zero transaction history are considered higher risk. A detailed business plan with projected cash flows partially compensates for the absence of a track record.

Business plan quality. Banks want to understand your revenue model, customer base, and expected transaction volumes. Vague plans are a red flag. Specificity signals legitimacy.

Documentation completeness. Trade license, Memorandum of Association (MOA), passport copies, proof of address, and shareholder certificates must all be current and certified where required. Incomplete KYC packages account for the majority of application delays (CBUAE guidance, 2024).

A fintech startup with a Cayman Islands shareholder was asked for additional source-of-funds documentation by two UAE banks before approval. That's standard practice for cross-border ownership structures, not a red flag about the business itself.

Is it worth using a free zone's banking introduction service?

Yes, in most cases. Free zone banking introduction services connect you with bank relationship managers already familiar with your license type and jurisdiction. Founders using structured introductions typically report fewer documentation requests and faster decisions than those approaching banks cold. The difference is context: the bank already understands your business category before the first meeting.

Minimum Balance Requirements and Account Charges to Budget For

Most UAE banks require a minimum average monthly balance (AMB). Falling below it triggers a monthly fee, typically AED 100–AED 500. AMB requirements run from AED 10,000 at RAKBank's SME tier to AED 50,000 at some ADCB tiers. Budget for these from day one.

Additional charges to factor in:

Outward international transfer fees: AED 25–AED 100 per transaction

Cheque book issuance fees

Annual corporate debit card fees

Statement fees for paper records

An e-commerce startup processing 200+ monthly international transfers found that negotiating a flat monthly fee with their relationship manager was more cost-effective than paying per-transaction rates. That conversation is worth having early. For support navigating these decisions, DSBH banking and taxation services can connect you with the right contacts.

Building a Strong Banking Relationship in the UAE From Day One

UAE banks value consistency and transparency. Regular deposits, clear documentation of fund sources, proactive communication with your relationship manager, and prompt responses to compliance queries all build the trust that leads to better services, credit facilities, higher transaction limits, and faster approvals for future requests.

Practical Habits That Strengthen Your Bank's Confidence in Your Business

Your bank's compliance systems are monitoring your account continuously. Consistent, explainable activity builds a positive profile. Irregular or unexplained transactions do the opposite.

Make regular deposits. Even modest, consistent inflows signal an active, legitimate business.

Document every significant transaction. Keep invoices, contracts, and payment confirmations organised and accessible.

Notify your bank before large or unusual transactions arrive. Surprises trigger compliance flags.

Respond quickly to any bank queries. Delays are interpreted as evasiveness under AML monitoring frameworks.

A media production startup proactively sent their relationship manager a project contract before receiving a large USD payment from a US client. The payment cleared without any compliance hold. A peer company in a similar situation didn't give advance notice and triggered a 10-day review. UAE banks are required to file Suspicious Transaction Reports (STRs) with the Financial Intelligence Unit for unexplained large transfers (CBUAE, 2024), so the more context you provide upfront, the smoother your banking experience.

When to Add a Second Bank Account to Your UAE Setup

A second account makes sense when your primary bank can't support a specific need: multi-currency holding, trade finance, or payment gateway integration. It also provides operational resilience. If one account is frozen during a compliance review, your business keeps running.

That said, avoid spreading activity too thin across multiple banks in your first year. Banks prefer concentrated, transparent transaction histories in the early months. Typical trigger points for adding a second account:

Annual revenue exceeding AED 500,000

International expansion requiring a separate currency account

Hiring beyond 10 employees (payroll complexity increases)

Adding an e-commerce channel needing gateway settlement separation

A retail startup opened a secondary account with a digital bank specifically for Shopify payment gateway receipts, keeping their primary traditional bank account clean for B2B invoicing and payroll. That separation made reconciliation simpler and kept both accounts' compliance profiles clean. See also: how to open a corporate bank account in Dubai for a step-by-step walkthrough.

The Role of Payment Gateways as a Complement to Your UAE Bank Account

Payment gateways like Telr, Stripe UAE, PayTabs, and Noon Pay sit between your customers and your bank account, processing card and digital payments. They are not a replacement for a corporate bank account, they complement it by enabling online revenue collection that then settles into your UAE business account.

Telr, Stripe UAE, PayTabs, and Noon Pay: Choosing the Right Gateway

Each gateway has a distinct profile. Picking the right one saves you integration headaches later:

Telr: Strong local UAE focus, Arabic-language checkout, works well with free zone companies. Telr is an official partner of Dubai South Business Hub, making it a natural first choice for DSBH-licensed businesses. See: Telr payment gateway for UAE businesses.

Stripe UAE: Fully launched in the UAE in 2023. Familiar interface for US or European founders, strong developer API, easy integration with SaaS billing platforms.

PayTabs: Well-suited for B2B payments and recurring billing, with strong GCC regional coverage.

Noon Pay: Backed by Noon's regional e-commerce infrastructure. Best suited for consumer-facing businesses.

All gateways require a UAE trade license and a corporate bank account for settlement, a personal account won't work. Gateway fees typically run 2.5–3.5% per transaction. A SaaS startup with US-based founders chose Stripe UAE for its familiar dashboard, while their physical retail brand used Telr for Arabic-language POS support. Two gateways, two distinct use cases.

How Payment Gateway Settlements Connect to Your Bank Account

Most UAE gateways settle funds to your bank account within 3–7 business days. Confirm your settlement currency before going live: some gateways default to USD even if your transactions are in AED. An online education platform discovered their gateway settled in USD by default, switching to AED settlement and aligning it with their RAKBank current account eliminated a recurring FX conversion cost entirely.

Settlement checklist before you go live:

Confirm settlement currency matches your bank account currency

Understand the chargeback and dispute resolution timeline

Check whether your bank requires a gateway integration letter

Note: chargeback rates above 1% can trigger gateway account reviews

WPS Requirements for UAE Startups With Employees

The UAE Wage Protection System (WPS) requires all companies with employees to pay salaries through an approved WPS channel, typically your corporate bank account or an approved payroll agent. Companies with one or more employees must comply. Non-compliance results in fines and can affect your trade license renewal.

How WPS Works and What Your Bank Needs to Enable It

WPS is administered by the UAE Ministry of Human Resources and Emiratisation (MoHRE). It electronically verifies that salaries are paid on time and in full to every registered employee. Your bank must be a registered WPS agent to process payroll, RAKBank, Emirates NBD, ADCB, and FAB are all registered.

Steps to activate WPS through your bank:

Confirm your bank is a registered WPS agent (check the CBUAE approved agents list)

Register your company on the MoHRE WPS portal

Submit employee Emirates IDs and salary details to your bank's WPS team

Process the first payroll cycle through the WPS-enabled account

Salaries must be paid within 10 days of the agreed payment date. Delays trigger automatic MoHRE notifications. Fines for non-compliance start at AED 5,000 per unpaid employee and can escalate to license suspension (MoHRE, 2024).

A 5-person startup at Dubai South activated W

References

Editorial sources available on request. Full citation list is being compiled.