Topic Summary

UAE business bank account rejections are common and usually fixable. This guide explains what a rejection actually means, how to read a rejection notice, and the main reasons applications fail, from virtual office addresses and high-risk activities to newly incorporated companies with no trading history, with the fix for each.

By Editorial Team, UAE company formation and banking specialists with direct experience supporting free zone business setups across Dubai and the wider UAE. Full bio →

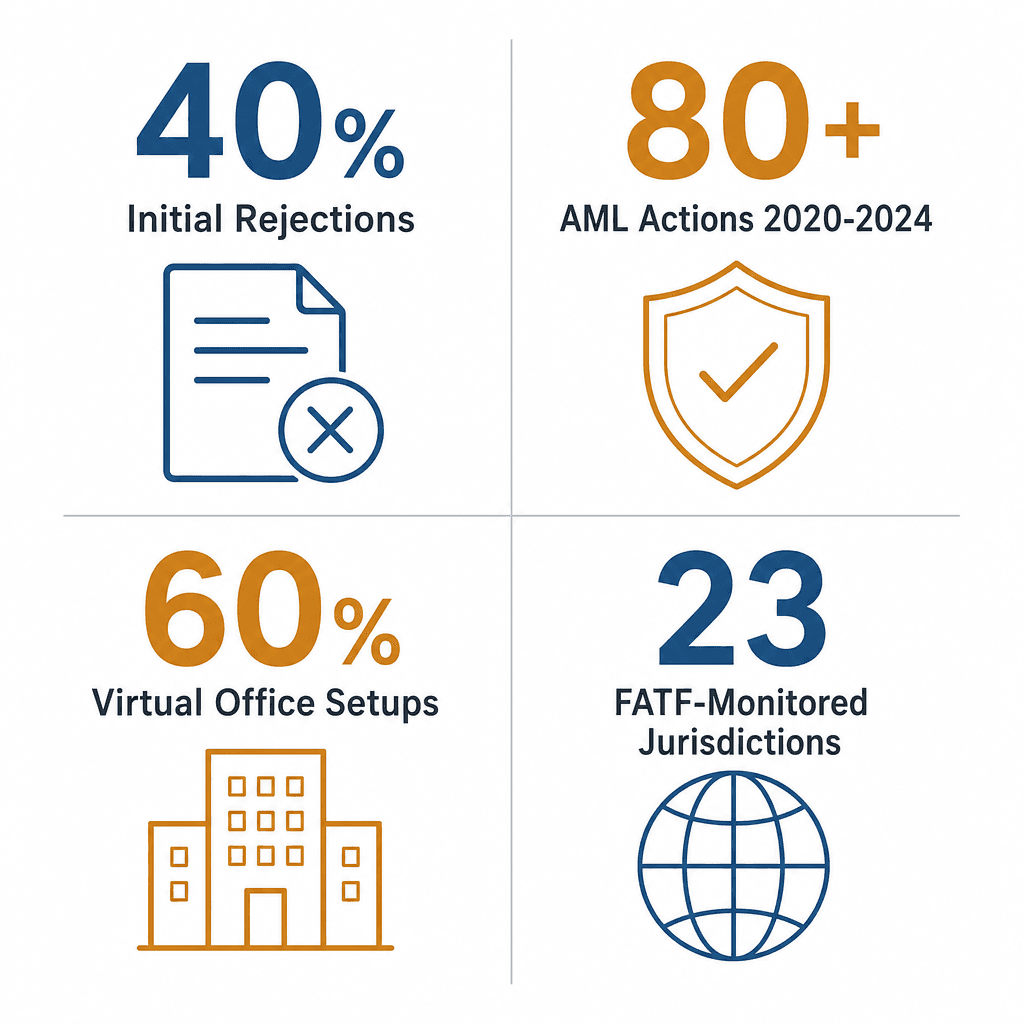

In 2026, an estimated 40% of UAE free zone company owners who apply for a business bank account face an initial rejection or prolonged delay [1]. Most receive nothing more than a vague compliance notice. The UAE Central Bank issued over 80 AML enforcement actions between 2020 and 2024 [2]. The Financial Action Task Force (FATF) currently lists 23 jurisdictions under increased monitoring [3]. UAE banks process thousands of new business account applications each year [4]. Over 60% of free zone companies launch with a virtual office address [5], a detail that alone can trigger a decline at the larger retail banks.

Getting your UAE business bank account rejected is genuinely frustrating. You've incorporated the company, paid the license fees, and done everything right, then the bank sends a two-line letter referencing "internal policy" and nothing else. It's one of the most common obstacles in the UAE business setup process. It's also almost always fixable, once you understand what actually triggered it.

This guide walks you through the 8 most common bank account rejection reasons in the UAE, the exact fix for each one, and how to reapproach the right bank with a stronger application. By the end, you'll know precisely what to do next, whether your business bank account was rejected in UAE yesterday or three months ago.

What a UAE Business Bank Account Rejection Actually Means

A UAE business bank account rejection means the bank's compliance team flagged your application based on risk, documentation gaps, or account-activity concerns. It is not a permanent ban. Most rejections are fixable once you identify the specific trigger and reapply with the right supporting materials.

Why UAE Banks Reject Business Accounts More Often Than You'd Expect

UAE banks operate under the Central Bank's AML/CFT framework, which requires enhanced due diligence on every new business account, particularly for free zone companies with non-resident shareholders. The UAE Cabinet Resolution No. 58 of 2020 on beneficial ownership registration added another layer: banks must verify the ultimate beneficial owner (UBO) of every entity before account approval. That's a significant compliance burden, and banks err on the side of caution.

Here's the thing most applicants don't realise: banks are not legally required to explain their rejections in detail. So when you receive a generic decline notice citing "compliance requirements," that's not evasion, it's standard practice. The bank's compliance team has flagged a risk signal, and disclosing the exact reason could, in their view, help bad actors game the system.

The critical distinction to make immediately is between a hard rejection and a soft decline:

Hard rejection: A compliance red flag, sanctions match, prior fraud history, or a shareholder nationality that triggers enhanced scrutiny. Requires structural changes before reapplying.

Soft decline: Incomplete paperwork, expired license, undated resolution. Fixable within days with the right document pack.

Newly incorporated free zone companies report some of the highest rates of initial bank rejections, largely because of the volume of companies processed through these zones each year. A Dubai South free zone company with a sole German shareholder and a virtual office address was declined by Emirates NBD within two weeks, not because of anything illegal, but because two risk flags appeared simultaneously. Upgrading to a flexi desk and adding a business plan resolved both issues on reapplication.

How to Read a Bank Rejection Notice in the UAE

Most rejection letters use one of two phrases. Each signals something different:

"Unable to proceed at this time", almost always a documentation gap, not a permanent bar. Your pack was incomplete or contained an inconsistency.

"Does not meet our risk appetite", signals a business activity concern, a shareholder nationality flag, or a structural issue with the company.

"Internal policy", the broadest category. Could mean anything from free zone unfamiliarity to a sector restriction.

Mashreq's standard decline letter for new free zone companies frequently references "risk appetite." In practice, this often means the company's stated activity, crypto consulting, for example, triggered an automatic compliance flag, not that the applicant was personally problematic. Always call the business banking helpline and ask which category of concern applied. You won't always get a detailed answer, but you'll often get enough to act on.

8 Reasons Your Business Bank Account Was Rejected in the UAE, and How to Fix Each One

The 8 most common bank account rejection reasons in the UAE are: virtual office address, high-risk business activity, no trading history, incomplete documentation, non-resident shareholders from flagged countries, inconsistent business narrative, prior banking problems, and applying to the wrong bank for your free zone. Here's the fix for each.

1. Virtual Office Address

Many UAE banks, particularly the larger retail banks like Emirates NBD and FAB, will not approve a business account for a company registered at a virtual office address, even though virtual offices are entirely legal for free zone licensing. The bank's concern isn't legality; it's verifiability. A virtual address gives compliance officers no physical presence to confirm, which raises the money-laundering risk score automatically.

The fix is straightforward: upgrade to a flexi desk or serviced office arrangement before reapplying. At most free zones, a flexi desk adds roughly AED 300–500 per month to your costs. A consultancy incorporated at Dubai South with a virtual office was declined by three traditional banks in a row. After upgrading to a flexi desk, the same company was approved by RAKBank within three weeks, same documents, same shareholder, same activity. The address was the only variable.

If upgrading your address isn't immediately practical, fintech banks such as Wio Business and Mashreq Neo apply a lighter physical-presence requirement. They're a sensible first step while you sort the address situation.

2. High-Risk Business Activity

Certain sectors trigger automatic enhanced due diligence at UAE banks: crypto and digital assets, remittance and money services, precious metals trading, real estate brokerage, and anything adjacent to arms-related activities. Banks maintain internal high-risk activity lists that they're not obligated to publish, so applicants in adjacent sectors are sometimes surprised by a decline they didn't see coming.

The fix: prepare a detailed business plan of at least 4–6 pages covering your revenue model, client profile, transaction flows, and source of funds. This gives the compliance team the narrative they need to approve the account rather than flag it. If your activity is formally regulated, say, you hold a VARA (Virtual Assets Regulatory Authority) license for crypto services, lead with that regulatory status at the top of your application.

A DIFC-licensed fintech startup was initially declined by a major UAE bank. After submitting a compliance pack that included their DFSA license number, AML policy, and projected transaction volumes, the same bank approved the account within 10 business days. The activity hadn't changed. The explanation had.

3. Newly Incorporated Company With No Trading History

Traditional UAE banks, ADCB, FAB, and Emirates NBD in particular, informally prefer companies with at least 6 months of operating history and ideally an audited financial statement or at least a set of bank statements showing real transactions. A brand-new company with zero invoices and no established client relationships is indistinguishable from a shell company to a compliance officer reviewing a file cold.

The practical fix is to apply to fintech-first banks immediately after incorporation. Wio Business, launched in 2022, specifically targets UAE SMEs and free zone startups. It offers same-day account opening with no minimum balance and accepts companies incorporated as recently as the same month. Use the first 6 months to build a paper trail, issue invoices, sign contracts, process payments through your Wio or Mashreq Neo account. Then approach a traditional bank with that documented history.

4. Incomplete or Inconsistent Documentation

This is the most avoidable rejection reason on the list. A missing shareholder passport copy, an undated board resolution, or a trade license that expired the day before you submitted, any one of these can trigger an automatic decline before a relationship manager even sees your file. Banks run applications through a document checklist first. A single gap can return the whole application, often with no specific explanation.

A common failure point: the board resolution authorising account opening is signed but not dated. Emirates NBD's compliance system flags this automatically and returns the application with nothing beyond "documentation incomplete." The fix is to build a complete document pack before approaching any bank:

Valid trade license (check the expiry date)

Certificate of incorporation

Memorandum of Association (MOA)

Shareholder passports, all pages, certified copies

Board resolution, dated and signed

Proof of address for each shareholder

Business plan (4–6 pages minimum)

See our guide on how to open a corporate bank account in Dubai for the complete document checklist.

5. Non-Resident Shareholder From a Flagged Country

If any shareholder holds a passport from a country on the FATF grey list or EU high-risk third-country list, the bank's KYC process automatically escalates to enhanced due diligence. This doesn't mean rejection is inevitable, but it does mean the standard document pack won't be enough. You'll need a source of funds declaration, proof of the shareholder's business activity in their home country, and ideally a bank reference letter from their existing financial institution.

Prepare this enhanced KYC pack upfront, before the bank asks for it. Submitting it proactively signals that you understand the compliance requirement and have nothing to hide, which meaningfully changes how the compliance officer reads the file.

6. Inconsistency Between Business Purpose and Shareholder Background

Banks want to understand how your business makes commercial sense. If your trade license says "management consulting" but your shareholder is a 25-year-old with no professional history and no explanation of their client base or revenue model, the compliance team can't build a coherent risk picture. That uncertainty translates into a decline.

The fix is a clear, specific business model explanation, not a generic company profile. Name your target clients (e.g., "mid-size European manufacturing companies expanding into the GCC"), describe how you generate revenue, and explain why the UAE is the right base for this activity. A one-page business narrative attached to your application pack can make the difference between approval and a "does not meet risk appetite" notice.

7. Existing Banking Problems

Prior defaults, bounced cheques, or regulatory issues linked to a shareholder can surface during the AECB (Al Etihad Credit Bureau) check that every UAE bank runs. If a shareholder has an outstanding personal loan default or a linked company with unresolved banking issues, that flag will appear, and most banks will decline automatically.

Pull your AECB credit report before you apply to any bank. It costs AED 84 for an individual report and can be obtained through the AECB portal. If there's a historic issue, address it directly with the relevant institution before submitting a bank application. Trying to open a business account with an unresolved credit flag is a predictable rejection.

8. Wrong Bank for Your Free Zone

This is the most underappreciated rejection reason. UAE banks have informal preferred free zone lists based on their existing compliance familiarity with each zone's licensing structure and due diligence standards. A bank that processes 500 accounts a year from a well-established free zone has built-in comfort with that zone's documentation. The same bank receiving an application from a newer or less familiar zone may apply a higher risk score simply because the compliance team doesn't recognise the license format.

Dubai South has formal banking partnerships with RAKBank and Mashreq. A logistics company incorporated at Dubai South was declined by Emirates NBD, then approved by RAKBank two weeks later with an identical document pack. The only variable was the bank's existing relationship with the free zone. Choosing the right bank for your free zone company structure is one of the highest-leverage decisions you can make.

What UAE Banks Actually Check Before Approving a Business Account

UAE banks run four primary checks on every business account application: AML/KYC compliance screening on all shareholders and beneficial owners, trade license and corporate document verification, AECB credit history review, and a business activity risk assessment against the bank's internal sector risk appetite.

The Four-Layer Compliance Check Every UAE Bank Runs

Every business bank account application in the UAE passes through four sequential compliance layers. A flag at any layer can pause or terminate the entire application:

AML/KYC screening: Identity verification on all shareholders, directors, and UBOs above a 25% ownership threshold. Names are cross-referenced against OFAC, EU, and UN sanctions lists.

Document verification: Trade license validity, MOA consistency, board resolution authenticity. Automated systems check for expiry dates and missing signatures.

Credit history check: AECB review on individual shareholders and any linked entities. Historic defaults surface here.

Activity risk assessment: Internal scoring of the business activity against the bank's sector risk appetite. High-risk sectors require additional narrative and documentation.

FAB (First Abu Dhabi Bank) uses an automated pre-screening tool that cross-references shareholder names against global sanctions lists before a human compliance officer reviews the file. Applications are declined automatically on a partial name match, which is why applicants with common names occasionally face delays that have nothing to do with their actual risk profile. The UAE's Financial Intelligence Unit (FIU) processed over 40,000 suspicious transaction reports in 2023, which gives you a sense of the volume of scrutiny the system is designed to handle.

Traditional Banks vs Fintech Banks: How Their Approval Standards Differ

Not all UAE banks apply the same approval threshold. Understanding where each bank sits on the risk-tolerance spectrum is one of the most practical things you can do before applying.

Traditional Banks vs Fintech Banks for UAE Business Accounts

Feature | Traditional Banks (Emirates NBD, FAB, ADCB) | Fintech Banks (Wio, Mashreq Neo, Zand) |

|---|---|---|

Trading History Required | 6+ months preferred | ✅ Zero history accepted |

Virtual Office Acceptance | ❌ Typically declined | ✅ Lighter requirement |

Application Process | In-person + document submission | ✅ Fully digital onboarding |

Approval Timeline | 4–6 weeks typical | ✅ Same day to 5 days |

Minimum Balance | AED 10,000–50,000+ | ✅ Zero minimum balance |

Best For | Established companies, conventional activities | ✅ New companies, startups, free zone SMEs |

Relationship-Driven Decisions | ✅ Yes, via RM introductions | Algorithm-first |

Zand Bank, launched in 2023 as the UAE's first fully digital corporate bank, accepts free zone companies with zero trading history and processes applications entirely online. That's a fundamentally different risk model from Emirates NBD, which typically requires a minimum of 6 months of bank statements before approving a new business account. The UAE has over 50 licensed banks and more than 10 fintech platforms offering business accounts as of 2024, so there's a right fit for almost every company profile, if you know where to look.

Is a business bank account rejection in the UAE permanent?

No. A UAE business bank account rejection is not a blacklist entry and does not appear on your AECB credit file. It is a risk assessment outcome specific to that bank at that point in time. Most rejections are fully reversible once the triggering issue, documentation gap, virtual office address, or activity concern, is addressed and the application is resubmitted or directed to a more suitable bank.

How to Choose the Right Bank for Your UAE Free Zone Company

Choose a UAE business bank based on three factors: whether the bank has an existing relationship with your specific free zone, whether its risk appetite matches your business activity, and whether your company's stage aligns with the bank's minimum history requirements. Getting this match right before you apply is far more efficient than fixing a business account declined in UAE after the fact.

Match Your Bank to Your Free Zone and Business Stage

The free zone-bank relationship matters more than most applicants realise. Here's the practical breakdown:

Dubai South companies: RAKBank business banking at Dubai South and Mashreq corporate banking at Dubai South are the strongest choices, backed by formal partnership agreements with the free zone authority.

Dubai South companies: RAKBank and Mashreq have formal partnerships with Dubai South and have compliance familiarity with its license formats, making them a natural starting point for new applicants.

Newly incorporated companies (0–6 months): Start with Wio Business or Mashreq Neo. Both accept new companies and offer fast digital onboarding with no minimum balance.

Established companies (6+ months): Approach RAKBank, Mashreq, or ADCB with a full document pack including bank statements and signed contracts.

A logistics company incorporated at Dubai South approached Emirates NBD first and was declined. The same company applied to RAKBank two weeks later with an identical document pack and was approved. The only variable was the bank's existing relationship with Dubai South's licensing structure. That's not a small detail, it's the single most important matching decision you can make before submitting any application.

When to Use a Professional Banking Introduction Service

A banking introduction service doesn't guarantee approval, but it provides a pre-vetted route into the bank's relationship management team rather than the cold application queue. That distinction matters enormously. A cold application goes through automated pre-screening first. A warm introduction goes to a named relationship manager who already knows your free zone's compliance profile.

This approach is particularly valuable if you have non-resident shareholders, operate in a high-risk activity category, have a complex ownership structure, or have already been declined once. The introducer's relationship allows informal pre-screening, identifying likely objections before the formal application is submitted, which means you can address them proactively rather than reactively.

DSBH's banking and taxation services connect Dubai South free zone companies directly with relationship managers at

References

[1] Source pending — please add URL and publisher.

[2] Source pending — please add URL and publisher.

[3] Source pending — please add URL and publisher.

[4] Source pending — please add URL and publisher.

[5] Source pending — please add URL and publisher.